By Nicholas Earl

Wood Group has posted robust revenues and gross profits, as it bids to bolster its share price and win back the approval of investors following the failed takeover attempt from private equity firm Apollo.

The Scottish engineering giant generated £2.2bn ($2.9bn) in revenue over its first six months of trading in 2023, up around 15 per cent year-on-year.

This lead to adjusted earnings before interest, tax, deductions and amortisation (EBITDA) of £149m ($195m), which is a six per cent boost over the same trading period 12 months ago.

Its bumper figures were powered by a fattening order book which has stretched to £4.6bn ($6bn), up three per cent excluding the sale of its Gulf of Mexico business earlier this year.

This was supported by multiple contract wins, including a hefty £191m ($250m) deal to extend a life sciences engineering contract in South East Asia for brownfield services, a new £38m ($50m) agreement with Glaxosmithkline in the US, and an engineering services contract with Euro Manganese for sustainable mineral processing.

Its projects arm experienced chunky revenue growth of around 26 per cent, taking revenues up to £920m ($1.2bn), while Wood’s consulting division saw strong revenue growth of around nine per cent to £230m ($300m), with continued growth in its solutions across both energy security and energy transition.

In a sign of the emerging shift to green projects as companies scramble to align themselves with net zero targets, over a third of Wood’s bidding pipeline was from sustainable solutions, up from 30 per cent at year end.

However, it warns that outflows of around £103m ($135m) on its expenses, which it attributes to the seasonality of its business, and the remaining tax paid on the sale of the its environment consulting division – totalling around $60m.

This contributed to a spike in its net debt position, which worsened from £301m ($393m) at the end of 2022 to £498m ($650m) – roughly 2.2 times its EBITDA.

Nevertheless, the company is bullish about its future prospects, and now expects to generate positive free cash flow in the second half of 2023.

It has also made no change to its optimistic full-year expectations of extra liquidity through the entirety of 2024.

Ken Gilmartin, chief executive, said: “Trading shows continued good growth and margins in line with our expectations. We have won a number of significant contracts in energy, minerals and life sciences during the period, all testament to the exciting position Wood holds in its key growth markets.

“As we look ahead, we are confident of our delivery both for the full year and medium term, including a return to generating positive free cash flow.”

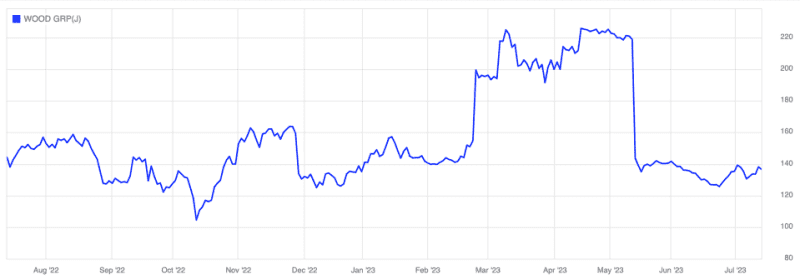

Wood did not reference Apollo’s attempted takeover of the company earlier this year – after the company knocked back five bids from the private equity firm.

In May earlier this year, Apollo ruled out making a sixth bid for the company, after several months of pursuing a takeover of the business – including a final offer of 240p per share on April 4 – a 20 per cent premium on its trading price that day.

Since then, Wood’s shares have plummeted on the FTSE 250 since then – dropping to 135p per share in the two weeks following the aborted sale.

Following today’s results, shares are down 1.3 per cent at 136.4p per share on the London Stock Exchange this morning.