Pfizer (PFE) investors are bound to be disappointed with the stock’s returns. With a loss of 44%, it was among the worst-performing S&P 500 Index ($SPX) stocks last year. PFE stock peaked in December 2021, when its market cap surpassed $300 billion - and while the broader markets have since risen to new record highs, Pfizer’s market cap is only around half of what it once was at its peak. Though this might bring investors little comfort, sector peer Moderna (MRNA) – which also developed a COVID-19 vaccine – hasn’t fared any better, and its 2023 drawdown was similar to that of PFE.

Will Pfizer stock go up over the next couple of years, or will the pharma giant's shares remain dead money? Here’s the 2025 forecast for PFE, and the key catalysts that could drive a rally in the stock.

Why Has Pfizer Stock Fallen?

The key reason Pfizer stock has fallen over the last couple of years is due to dwindling sales of its COVID-19 products. That includes both the COVID-19 vaccine Comirnaty and the Paxlovid pill used to treat active infections.

A cursory look at Pfizer’s earnings helps explain why the stock has sagged. In 2023, Pfizer reported revenues of $58.5 billion, which were 42% lower than the previous year. While the company’s non-COVID sales rose 8%, that wasn't enough to offset the negative impact from falling sales of Paxlovid and Comirnaty.

Going forward, management expects Paxlovid and Comirnaty sales to hit $3 billion and $5 billion, respectively, in 2024. The combined sales forecast of $8 billion would be a shadow of comparable 2022 sales of $57 billion.

But Pfizer’s troubles go beyond its COVID-19 portfolio. In December, it halted the development of its twice-daily oral weight loss drug, danuglipron, after adverse side effects. Some also believe that Pfizer overpaid for its Seagen acquisition, and the transaction has left its balance sheet saddled with another $31 billion in debt.

Pfizer Stock 2025 Forecast: Seagen, New Products Could Be Key

There looks to be little hope of a revival in Pfizer’s COVID-19 portfolio, barring an unfortunate rise in infections. As such, Pfizer’s 2025 forecast will most likely depend on new product development and sales contributions from Seagen.

Pfizer expects Seagen revenues to come in at $3.1 billion in 2024, and gradually rise to at least $10 billion by 2030. During the Q4 earnings call, Pfizer’s CEO Albert Bourla said that, along with growing its key product franchises, Pfizer is “exploring further opportunities to advance a number of innovative combination regimens.”

He added, “We believe we are well-positioned to bring our global commercial manufacturing and supply capabilities to accelerate current and future marketed products. We believe all these components support our growth potential through 2024 and drive growth potential into 2025.”

For 2024, Pfizer forecast revenues between $58.5 billion to $61.5 billion. At the low end, that implies no YoY revenue growth for 2024. Analysts, however, expect the company’s growth to pick up, and consensus estimates call for 5.8% YoY revenue growth in 2025.

The company expects incremental net cost savings of $2 billion by the end of 2024. Along with the $2 billion that it realized in 2023, that would take the cumulative savings to $4 billion.

Pfizer is looking to deleverage its balance sheet over the next few quarters, and expects to lower its leverage ratios to more comfortable levels. It also expects operating margins to gradually rise into the “mid- to high 30s.”

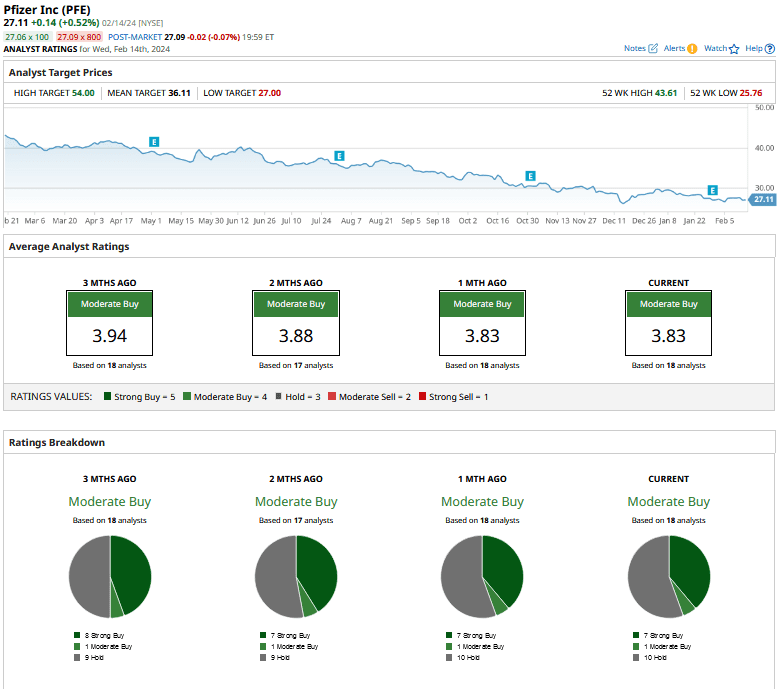

Analysts Expect Pfizer Stock to Go Higher

PFE has received a consensus rating of “Moderate Buy” from analysts, and its mean target price of $36.11 is 33% higher than Wednesday’s closing price. Of the 18 analysts covering the stock, only 7 rate it as a “Strong Buy,” and 1 as a “Moderate Buy.” The remaining 10 analysts rate the stock as a “Hold.”

Moreover, even the most bearish of analysts covering Pfizer don’t see it dropping any further, as the Street-low target price of $27 is roughly flat with current prices. However, the Street-high target price of $54 implies the stock nearly doubling from these levels.

Amid the recent pullback, Pfizer stock has not only given up its COVID-era gains, but has retreated to levels last seen in 2016. While the decline in sales of its COVID-19 products has weighed on the shares, the stock’s risk-reward looks quite favorable at current levels - even as a rerating might take time, and could predominantly depend on how its product pipeline shapes up, especially after the obesity drug disappointment.

Overall, I believe that stabilizing sales of COVID-19 products (albeit at a much lower base), decent revenue growth in the non-COVID portfolio, focus on cost cuts, and deleveraging efforts make Pfizer stock worth a look.

Also, with its next 12-month price-to-earnings multiple of 12.2x significantly below long-term averages, and a dividend yield above 6%, Pfizer stock could fit well into most value investors’ portfolios.

On the date of publication, Mohit Oberoi had a position in: PFE . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.