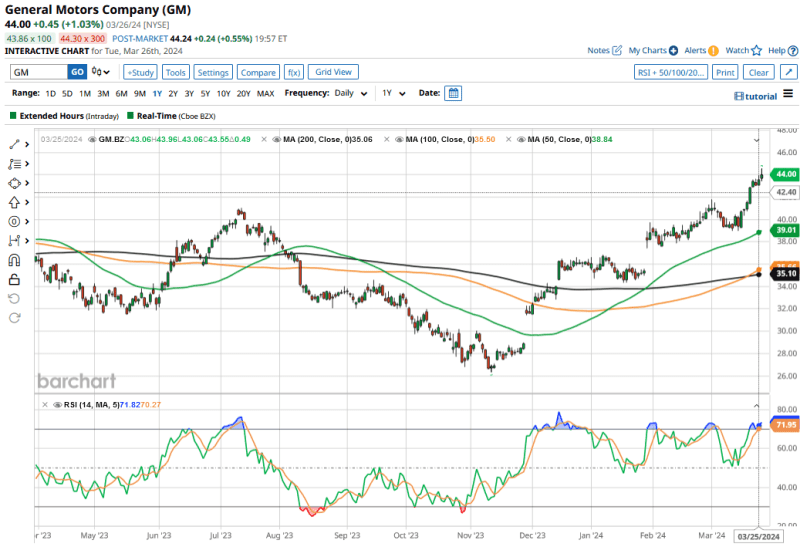

General Motors (GM) stock hit new 52-week highs yesterday, and is now up 22.5% for the year to comfortably outperform the S&P 500 Index ($SPX). Ironically, Tesla (TSLA) is the worst-performing S&P 500 constituent this year, while some other electric vehicle (EV) names are trading near their record lows.

We have seen a clear divergence in the fortunes of legacy automakers and pure-play EV companies over the last few months. While legacy automakers are upbeat on the earnings and demand outlook, EV companies across the board have flagged sluggish demand.

This includes Tesla, which warned that this year's delivery growth “may be notably lower than the growth rate achieved in 2023.” EV bankruptcies also look set to accelerate, and Fisker (FSR) could be next on the list after it said that talks with a major unnamed automaker have failed, prompting the NYSE to delist the stock.

Meanwhile, even as GM stock hit its 52-week highs yesterday, the stock still looks cheap and could potentially double from here. Here’s why.

General Motors Believes Its Own Stock Is Cheap

Yesterday, General Motors presented at the Bank of America 2024 Global Auto Summit. While the company’s CFO Paul Jacobson talked about multiple topics during the event, he particularly stressed the company’s low valuation multiple, featuring it three times during the conversation.

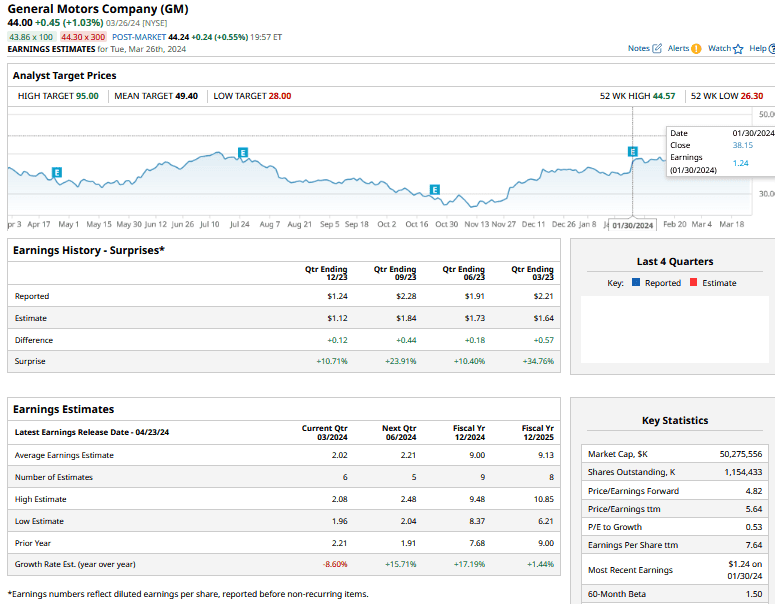

To gauge whether GM stock is really cheap, let’s dive into the company’s 2024 guidance that it provided during the Q4 earnings call. General Motors expects to post net income between $9.8 billion and $11.2 billion this year, versus the $10.1 billion that it posted last year. However, management expects the adjusted earnings per share (EPS) to range between $8.50-$9.50, which is significantly higher than the $7.68 that it posted last year.

The divergence between the net income and EPS guidance is because of the massive $10 billion share buyback that GM announced last year, which it expects will push up the 2024 EPS by $1.45.

Looking at other metrics, GM expects to generate adjusted automotive free cash flows between $8 billion to $10 billion in 2024, which is lower than the $11.7 billion it posted last year.

GM Stock Valuation Looks Cheap by Historical Standards

Here’s how GM stock measures up right now, based on a few different valuation metrics:

- GM stock trades at a next 12-month (NTM) price-to-sales multiple of 0.29x, as compared to an average multiple of 0.39x over the last three years.

- GM stock trades at an NTM price-to-earnings (PE) multiple of 4.9x, which is a significant discount to the long-term averages. Its multiples are also below those of hometown rival Ford (F), which trades at an NTM PE multiple of 6.65x.

- GM’s NTM market cap to free cash flows is a mere 6.16x.

There has been a disconnect between the share prices of legacy automakers and their resilient earnings. If anything, GM’s earnings might be better than its guidance this year, as it said that pricing so far has held up much better than what it had expected.

Interestingly, one of the reasons that valuations of legacy automakers are languishing near record lows is because markets believe that they have hit peak profitability, and margins and profits will fall in coming years as they sell more electric cars.

Ford CEO Jim Farley has emphasized multiple times that the company is nowhere near peak profitability, as some believe. GM is also working on EV profitability, and sees the business churning out a variable profit in the back half of this year before becoming profitable next year.

GM is also building flexibility in its plants, so that it can pivot production between EVs and internal combustion engine (ICE) vehicles based on the demand environment. Plus, General Motors is bringing hybrid cars to North America, as the demand for hybrid cars has been strong even as the EV adoption rate has slowed down.

General Motors Stock Forecast

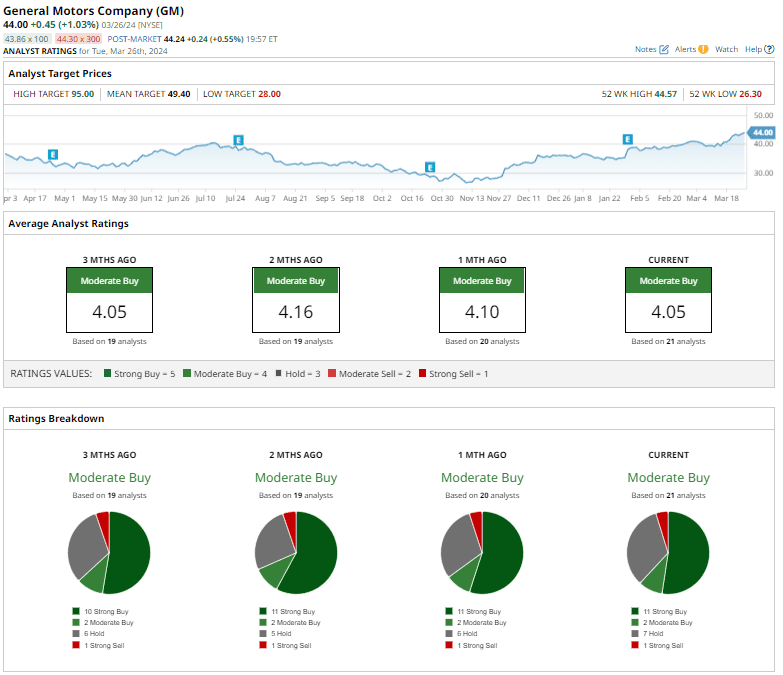

GM has an overall rating of “Moderate Buy” from analysts. Of the 21 analysts covering GM stock, 11 have a “Strong Buy” rating while 2 have rated it as a “Moderate Buy.” Seven analysts rate GM as a “Hold,” and 1 as a “Strong Sell.”

GM’s mean target price of $49.40 is 12.2% above yesterday’s closing prices. Its Street-high target price of $95 (via Citi) implies the stock could more than double from these levels.

To be sure, the path ahead is not that easy for GM. It has faced production issues in its EV ramp-up, and the Cruise self-driving business has failed to live up to expectations, and last year the company had to pause its operations. As for valuation, legendary value investor Warren Buffett's exit of GM stock was hardly the upvote that it needed.

However, I believe GM is a good stock to buy at these levels, as the company benefits from a strong pricing and demand environment for ICE cars. It has also tweaked its capital allocation, making it more skewed towards increasing shareholder returns - which could mean more buybacks or even special dividends for investors.

While GM stock might not double over the next year, as the Street-high target price suggests, I would put my two cents on GM doubling over the next two to three years as its valuations revert to more normalized levels.

On the date of publication, Mohit Oberoi had a position in: F , GM , TSLA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.