By Elliot Gulliver-Needham

Today’s release of the UK’s GDP figures feels like a big deal. Proclamations that the Britain’s recession is over are everywhere, with what feels like the first bit of positive news for our economy in forever.

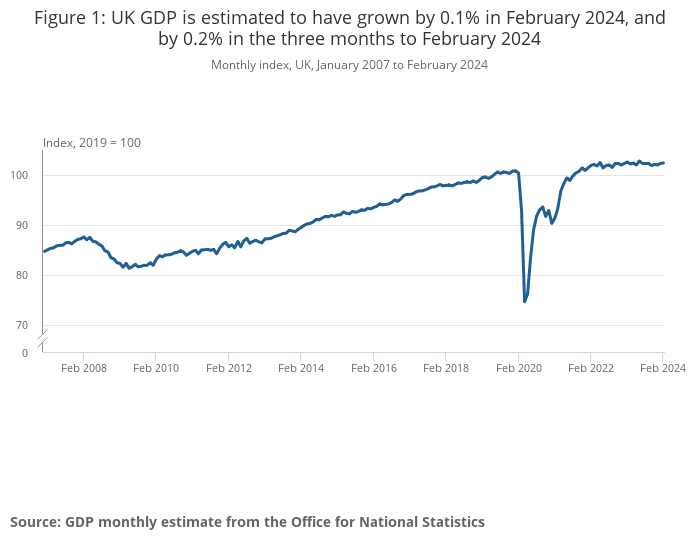

Growth over the last three months improved from -0.1 per cent to +0.2 per cent, thanks to February’s 0.1 per cent growth and a revision in January’s figures.

However, today’s numbers show something a bit murkier beneath the surface when looking closer, and many analysts are cautioning that the way out of recession might not be so easy.

Because of the terrible performance of the UK economy at the end of last year, where GDP fell 0.3 per cent in the last quarter, January and February’s numbers are just bringing us back to where we were in September 2023.

Based on today’s figures, economists are estimating that the first quarter of the year will see GDP growth of 0.4 per cent. While positive, these aren’t exactly the numbers we need to pull us out of the recession and into a new era of prosperity.

That figure would still be lower than most of the first quarters in the decade before the pandemic, when growth in the UK economy wasn’t exactly strong.

Today’s figures also don’t include GDP per head, so the economic gain we’ve seen could just be a result of more people coming into the country, rather than actual increases in productivity.

Meanwhile, though business services and manufacturing had a strong showing in today’s numbers, other areas of the economy were actually surprisingly weak.

The Resolution Foundation’s James Smith noted that “consumer-facing services continued to be in the doldrums with another weak month for hospitality”, while construction suffered due to poor weather throughout February.

Roger Barker, director of policy at the Institute of Directors, added that the economy is “still in a fragile state”, also noting the poor performance in consumer-facing parts of the economy, particularly accommodation and food services.

“Although the latest figures suggest that the UK is likely to generate positive economic growth in the first quarter, there are few signs of a strong economic rebound,” he said.

What matters now is whether the UK can maintain this growth, and especially if it can push it above the bare minimum 0.1 per cent per month.

Yael Selfin, chief economist at KPMG UK, said the UK economy outlook remained “foggy” due to the potential for business investment to be “dented by uncertainty related to the general election and growing speculation around a second fiscal event in the Autumn”.

“The big question is whether this is whether this is the start of more sustained growth, consistent with the Office for Budget Responsibility forecast, or whether headwinds from the cost of living and interest rates will mean growth close to zero growth in Q2, consistent with the Bank of England forecast,” said Smith.

A lot of this might come down to the Bank of England. The central bank’s Monetary Policy Committee is due to meet next on 9 May, where it could decide to cut interest rates, potentially pushing growth up.

“The weakness of February’s GDP figures will give them food for thought as they seek to determine the future course of UK interest rates,” added Barker.

“Based on today’s figures, the case for cutting base rate sooner rather than later is a relatively strong one.”