Copper (HGK24) has outperformed the S&P 500 Index ($SPX) this year, up 10% due to rising demand from Chinese manufacturers and global supply constraints. Its indispensability in construction, infrastructure, and renewable energy, driven by urbanization and industrialization, has helped fuel demand for the red metal.

Earlier this month, Bank of America (BAC) raised its price forecast for copper in anticipation of tightening supply and accelerating demand. It projects copper prices to surge to $10,250 per ton by Q4 of 2024, marking an 8% increase from their previous view. Prices are anticipated to rise further to an average of $12,000 per ton by 2026.

Amid BofA's optimistic outlook for copper, Freeport-McMoRan Inc (FCX) is catching attention as a top dividend-paying copper stock. On April 9, alongside its broader bullish note on the underlying commodity, BofA upgraded FCX from "Neutral" to "Buy," noting Freeport-McMoRan's “high quality copper leverage, robust and rising free cash flow, and material gold revenue” as factors.

Given this backdrop, is the dividend stock a buy? Let's find out.

About Freeport-McMoRan Stock

Headquartered in Phoenix, Arizona, Freeport-McMoRan (FCX) mines mineral properties in North America, South America, and Indonesia, focusing on copper, gold (GCM24), molybdenum, and other metals. Its assets include the Grasberg district in Indonesia; several mines in Arizona, New Mexico, and Colorado; and operations in Peru and Chile. Its market cap currently stands at $71.7 billion.

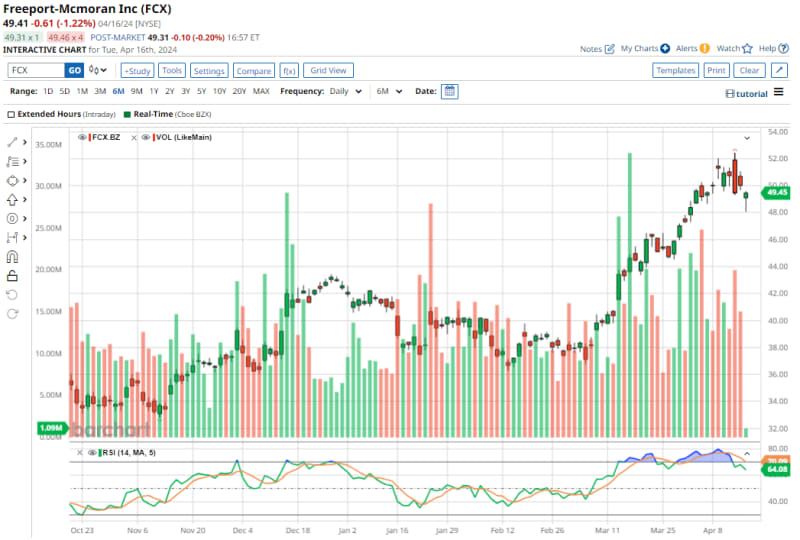

Freeport-McMoRan stock has surged by 16% on a YTD basis, outperforming the SPX's 6% gain over the same time frame.

The copper company pays shareholders a base quarterly dividend of $0.075 per share, along with variable payments based on performance. The trailing 12-month annualized dividend is $0.60 per share, which translates to a dividend yield of 1.20%.

Freeport-McMoRan stock trades at 30.84x forward earnings, in line with peers like Southern Copper (SCCO), at 29.65x. The current earnings multiple is lower than FCX’s own five-year average of 69.91x, too.

Freeport’s Q4 Earnings Beat Wall Street Projections

On Jan. 24, Freeport-McMoRan reported Q4 earnings of $388 million, or 27 cents per share, surpassing Wall Street expectations by 28.6%. Freeport-McMoRan’s revenue of $5.9 billion also beat the Street's forecast. The company’s forecast-beating report was credited to increased demand for copper and higher gold prices.

In its Q4 earnings presentation, management outlined its EBITDA and operating cash flow sensitivity to movements in copper prices. Management forecasts that a $0.10 change in copper price per pound equates to a $430 million increase in EBITDA and a $340 million increase in operating cash flow. The company's leaching technology and growth projects position it well to capitalize on rising copper prices.

Freeport-McMoRan is also actively pursuing growth opportunities, with several expansion projects across the U.S. The company is expanding its Lone Star Mine in Safford, Arizona, to increase copper production and extend the facility's operational life. It is also seeking permits for a pit addition at its Tyrone, New Mexico copper mine, underscoring its dedication to long-term sustainability and expansion.

Looking ahead, the company is, expecting to sell 4.1 billion pounds of copper, 2 million ounces of gold, and 85 million pounds of molybdenum in 2024. Analysts tracking Freeport-McMoRan expect the company's profit to reach $1.60 per share in fiscal 2024, up 3.9% year over year, and grow another 41.9% to $2.27 per share in fiscal 2025.

FCX will report Q1 earnings on Tuesday, April 23.

What Do Analysts Expect for Freeport-McMoRan Stock?

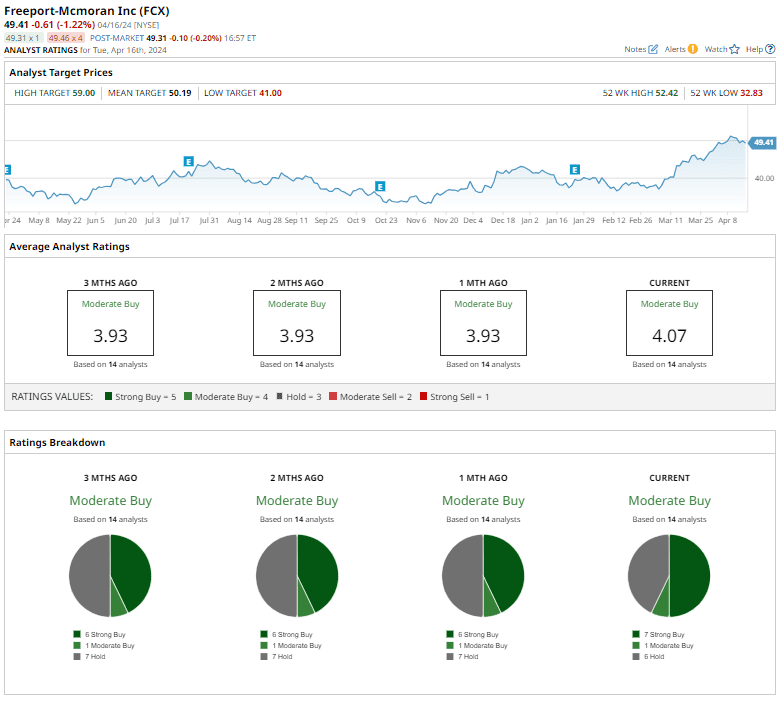

Freeport-McMoRan stock has a consensus “Moderate Buy” rating. Out of 14 analysts covering FCX stock, seven rate it as a "Strong Buy," one suggests a "Moderate Buy," and six say "Hold."

Scotiabank's Orest Wowkodaw recently maintained a “Sector Outperform” rating on FCX, but hiked the stock’s price target to $55 - more than 11% above the stock’s current price.

FCX stock is currently trading almost flat with the average analyst price target of $50.19. The Street-high price target of $59, assigned by BofA, indicates that the stock could rally as much as 19.4% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.