The global media and streaming industry is growing rapidly, with many new entrants fighting to make a mark. However, few names can match the weight and legacy of the Walt Disney Company (DIS). It has remained popular among viewers for over a century, thanks to timeless animated classics and blockbuster franchises like Marvel and Star Wars.

Disney is often compared to Netflix (NFLX), due to their stiff competition in the streaming content space. However, I believe Disney's legacy portfolio gives it an advantage over new entrants in the industry. Despite rising rivalry in the entertainment industry, Wall Street remains optimistic about this legacy player, rating it a "strong buy."

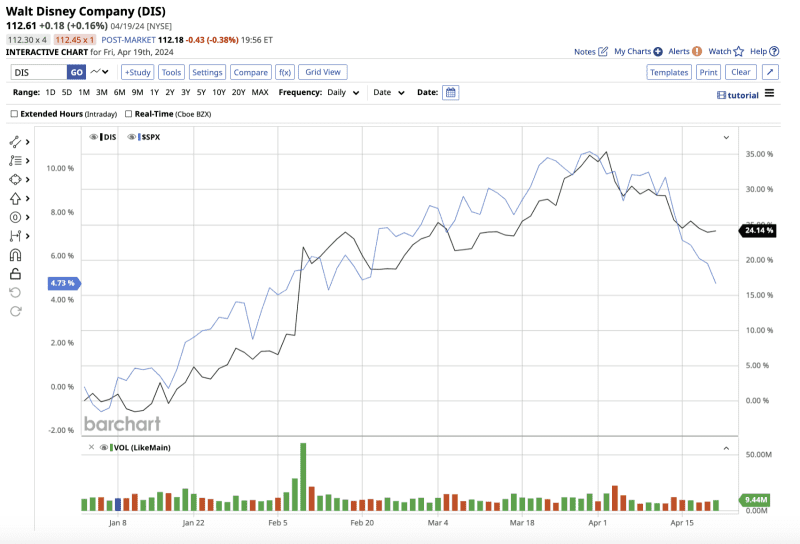

Valued at $206.5 billion, Disney stock is up 25% year-to-date, outperforming the S&P 500 Index’s ($SPX) gain of 4.7%.

The Bull Case For Disney

Disney's story is about adaptation and evolution. Over the years, the company has undergone numerous transformations, expanding its reach into various segments of the entertainment industry.

Besides its unparalleled portfolio of intellectual property (IP) - which includes Pixar, Marvel, and Star Wars - the company's businesses also include Disney Experiences, such as theme parks, resorts, cruises, and more. This diversified portfolio has allowed it to generate recurring and stable income over the years.

In the most recent first quarter of fiscal 2024, diluted earnings per share (EPS) jumped by an impressive 49% year on year to $1.04 per share. Total revenue was in line with the year-ago quarter at $23.5 billion.

Disney+, launched in 2019, is the company's attempt to establish its presence in the highly competitive streaming market. While Disney+ Core subscriptions fell by 1.3 million in Q1, the company expects to add 5.5 million to 6 million subscribers in Q2.

Management hopes to achieve profitability in its combined streaming business by the fourth quarter of fiscal 2024 through cost-cutting measures. The company expects to meet or exceed its annualized cost savings target of $7.5 billion by the end of fiscal 2024.

Furthermore, while reducing costs and focusing on profitability, the company is also committed to returning money to shareholders. Disney ended the quarter with $886 million in free cash flow, allowing it to pay dividends.

Notably, Disney increased its quarterly dividend by 50% to $0.45 per share in Q1. It pays a forward dividend yield of 1.6% with a payout ratio of 32%, leaving enough room for a dividend increase in the future. Plus, it is targeting $3 billion in share repurchases in fiscal 2024.

Looking ahead, in fiscal 2024, management expects earnings growth of 20% to $4.60, compared to the consensus estimate of $4.69. Analysts predict a modest 3.3% increase in revenue to $91.8 billion in fiscal 2024. Revenue and earnings could rise by 5.4% and 17.5% in fiscal 2025, respectively.

Comparatively, analysts predict that Netflix's revenue and earnings will rise by 14.4% and 51.5%, respectively, in 2024.

Is Disney Stock a Buy Now, According to Analysts?

Following Disney's strong first-quarter results, analysts are optimistic about the stock. Raymond James analyst Ric Prentiss reiterated his "buy" rating with a price target of $112. Prentiss is impressed with Disney's first-quarter results, which he believes demonstrate the company's ability to transition from a traditional TV business to a streaming powerhouse.

Additionally, Tigress Financial analyst Ivan Feinseth also sees a positive future for Disney. The analyst's favorable outlook is supported by Disney's ongoing financial strength, the diversity of its business segments, its strong balance sheet, and accelerating cash flow.

More recently,J.P. Morgan analyst David Karnovsky reiterated his “buy” rating on DIS, with a price target of $140, citing the company's “unparalleled content, promising streaming service financials, and the robust operations of their theme parks.”

The analyst believes that, based on its diverse business segments, the stock is now attractively valued "with a defensive cushion against downside risks."

Similarly, Argus Research also maintained a “buy” rating with a $140 price target.

Overall, Wall Street analysts rate Disney stock as a "strong buy.” Of the 27 analysts following DIS, 18 recommend it as a "strong buy," four suggest a "moderate buy," four rate it a "hold," and one recommends a "strong sell."

Analysts have set a mean price target for Disney stock of $125.65, which is 11.6% higher than current levels. Its high target price of $145 indicates an upside potential of nearly 29% over the next 12 months.

Disney is also the cheaper stock to invest in now. DIS's forward price-to-earnings (P/E) multiple of 24x is lower than Netflix’s forward P/E of 30x.

The Bottom Line on Disney Stock

No doubt, Netflix has quickly and firmly established itself in the entertainment industry. Analysts expect Netflix's earnings to skyrocket over the next two years. However, I believe that Disney's legacy global franchises, beloved brands, and diverse revenue streams will allow the company to survive and thrive in the long run. This makes Disney a resilient stock, providing investors with both growth and stability.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.