The stock market, as we've been reminded just recently, can be volatile. Dividend stocks allow investors seeking passive income to protect their portfolios from market volatility. Dividend-paying companies offer investors a consistent stream of income. The best dividend stocks often belong to stable, mature companies that generate consistent profits and have an established history of paying dividends to shareholders.

While higher dividend yields are always appealing to passive income investors, there are more factors to consider - such as a history of paying dividends, strong fundamentals, and a sustainable business model. Let’s take a look at three such dividend stocks to grab now.

Dividend Stock #1: Clearway Energy

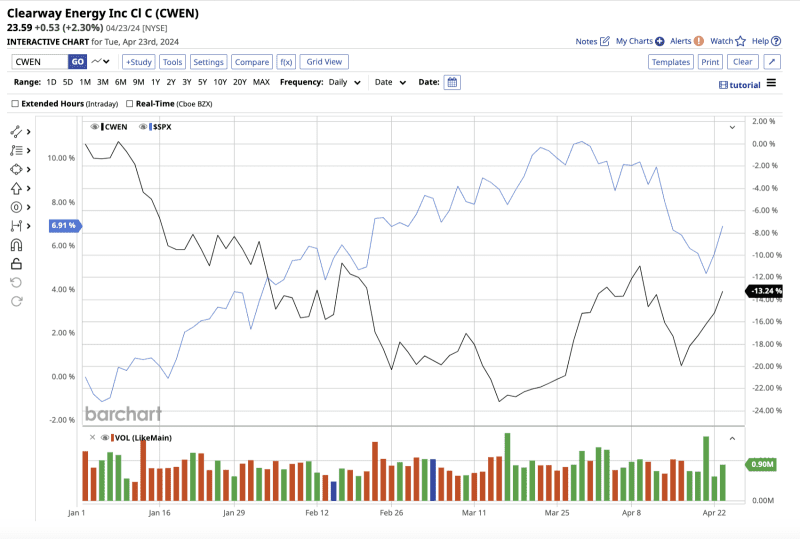

Clearway Energy (CWEN) is a leading renewable energy company focused on clean energy projects in the U.S. Founded in 2018, the company has a diverse portfolio that includes solar, energy, and wind storage assets.

Valued at $4.7 billion, CWEN stock has dipped 14.6% YTD, compared to the S&P 500 Index’s ($SPX) gain of 6.3%.

Clearway pays an annual dividend yield of 7.3%, which is significantly higher than the utility sector average of 3.6%. While the yield appears to be attractive, the payout ratio (which measures the amount of earnings to be paid out as dividends) is 228%.

This may raise questions about the company's ability to sustain dividend payments in the future. However, the company appears confident in meeting the upper end of its dividend growth target of 5% to 8% by 2026, without the need for additional capital. In Q1, the company increased its quarterly dividend by 1.7%, to $0.4033 per share.

Furthermore, CEO Christopher Sotos emphasized that the company's $215 million in new long-term corporate capital investments and "new Resource Adequacy contracts at Marsh Landing and El Segundo" will boost long-term growth.

While the company reported a loss in 2023, analysts expect that earnings will increase by 50% in 2024 to $1.01, dipping slightly by 1.5% in 2025.

Overall, Wall Street rates CWEN stock as a “moderate buy.” Five of the eight analysts who cover the stock rate it a "strong buy," while the other three rate it a "hold." The average target price assigned to the stock is $28.89, which is 23.7% higher than current levels. Furthermore, its Street-high target price of $37 implies a potential 58.4% gain over the next 12 months.

Dividend Stock #2: Agree Realty

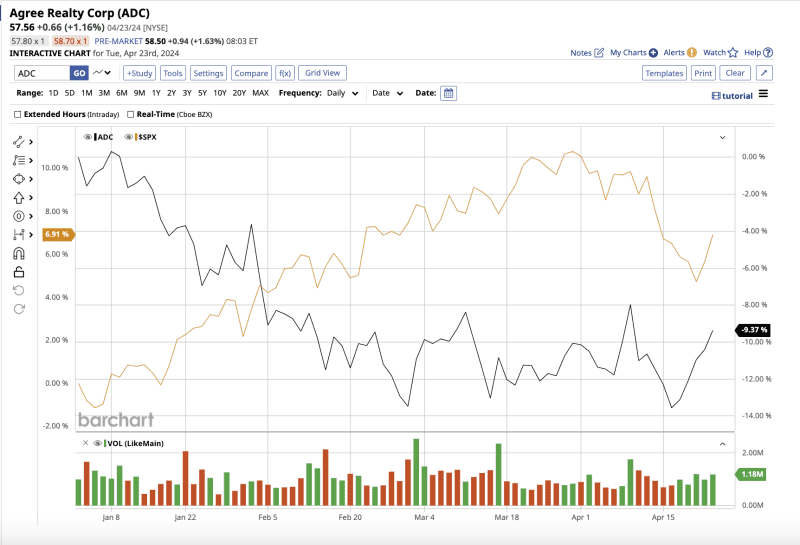

Agree Realty Corporation (ADC) is a real estate investment trust (REIT). Its operations are focused on acquiring, developing, and managing retail properties throughout the U.S.

Agree's portfolio includes 2,135 properties across 49 states. It is primarily made up of necessity-based retailers, like supermarkets, pharmacies, and convenience stores. These tenants have proven resilient for Agree's business. Furthermore, Agree Realty often has long-term leases with its tenants, resulting in recurring revenue.

Valued at $5.8 billion, ADC stock is down 7.2%, lagging the broader market.

In the first quarter of 2024, Agree's adjusted funds from operations (AFFO) increased by 5% year over year. AFFO is similar to net income for non-REITs, and measures the amount of earnings that can be distributed as dividends.

Agree Realty has a dividend yield of 5.21%, which is higher than the real estate sector average of 4.46%. Its forward AFFO payout ratio is 74.3%, indicating that the current AFFO can support dividend payments. As a REIT, Agree Realty is legally required to distribute 90% of its taxable income to shareholders as dividends.

Prior to its earnings, the company announced a 1.2% increase in the monthly cash dividend to $0.25 per share. Looking ahead, analysts predict Agree’s funds from operations (FFO) will increase by 3.5% in 2024 and 3.6% in 2025.

Overall, Wall Street rates ADC stock as a “strong buy.” Out of the 15 analysts that cover the stock, 10 rate it a “strong buy,” two rate it a “moderate buy,” and three rate it a “hold.” The mean target price for the stock is $66.23, which is 13.5% above current levels. Additionally, its high target price of $71 implies a potential upside of 21.6% over the next 12 months.

Dividend Stock #3: Innovative Industrial Properties

While the cannabis industry is rapidly expanding, investors remain skeptical due to the relatively high risks, as the drug is not federally legal in the U.S. This is where Innovative Industrial Properties (IIPR) comes in. This company allows investors to profit from the cannabis industry's rapid growth while avoiding industry risks.

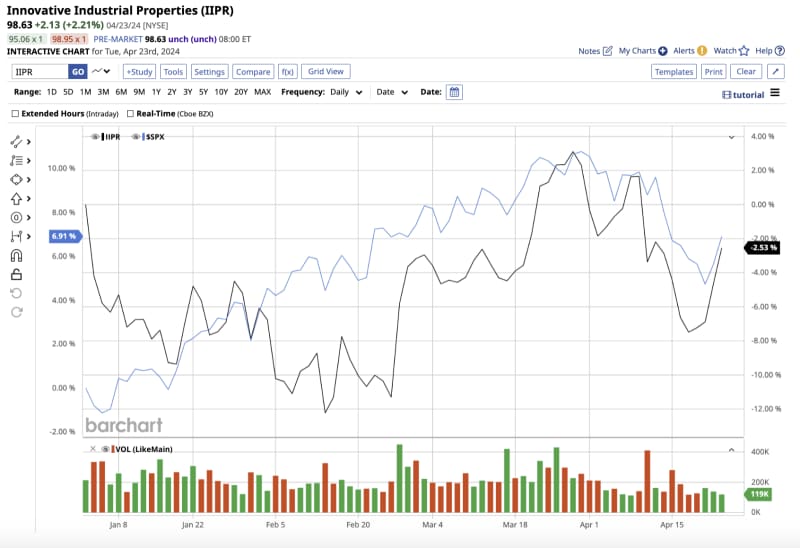

IIPR is a REIT that assists cannabis operators in the U.S. with the acquisition and leasing of properties for cannabis cultivation and processing. Its ability to generate consistent, recurring income through long-term triple-net lease agreements lasting 14.6 years with top cannabis companies has enabled it to pay dividends regularly. Its portfolio consists of 108 properties across 19 states, which are 95.8% leased.

Most of its tenants are leading cannabis companies, like Trulieve Cannabis (TCNNF), Green Thumb Industries (GTBIF), and Cresco Labs (CRLBF).

Valued at $2.8 billion, IIPR stock is down 2.5% on a YTD basis.

Like Agree Realty, IIPR is also required to pay out 90% of its earnings as dividends. In 2023, Innovative's AFFO increased 7% year-over-year to $9.08 per share.

It offers an attractive yield of 7.4%, which is significantly higher than the real estate sector average. Furthermore, its AFFO payout ratio of 79.8% implies that current dividend payments are sustainable, leaving room for growth.

Analysts predict a modest growth of 1.2% in Innovative’s FFO in 2024 and 0.57% in 2025, respectively.

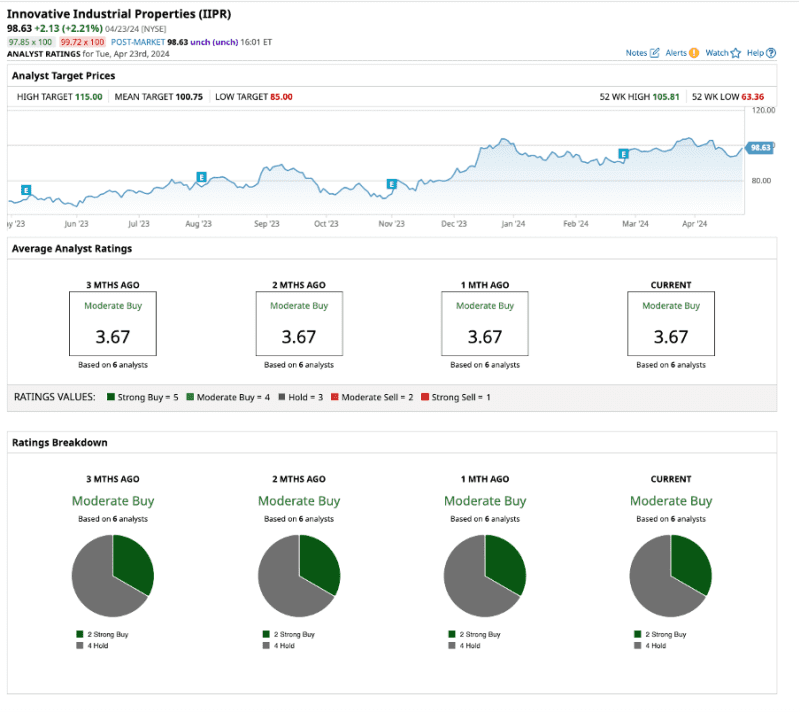

Overall, Wall Street rates IIPR stock as a “moderate buy.” Out of the six analysts who cover the stock, two rate it a "strong buy," and four rate it a "hold."

The average target price for the stock is $100.75, which is 2.1% higher than current levels. Furthermore, its high target price of $71 implies a potential 16.5% gain over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.