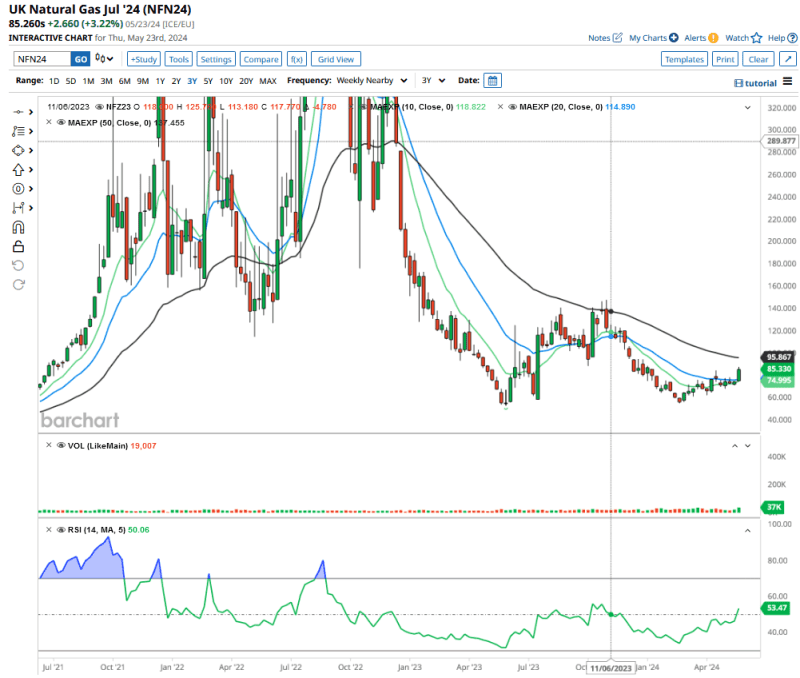

UK Natural Gas (NFN24), up +17.1%, is now at the highest levels since the middle of January 2024, fueled by a decrease of Norwegian exports to only 323 mcm a day as it competes with European demand. Imports from Norway are around 40%, and as the threat of outages continues, it has sustained prices.

During 2024, the average price has been 68.50, below the average price at the same time last year. The forward curve grows sharply upwards until the end of 2025 with December contract quoting above 109. Austria's OMV AG might stop payments to Gazprom soon, and that would cut 80% of supplies to the country.

Furthermore, Slovakia and Hungary are also dependent on Russian gas, despite the move to replace it as a result of the war in Ukraine, which was the main transit zone. Most gas into Europe from Russia is now provided via Turkey, and has not been affected by sanctions so far.

So, the geopolitical situation seems to be the main factor driving prices, as storage is still at good levels.

The contract has finally broken the key level of 74.90, and this week, it has surprised the market with a bullish breakout, placing prices well above the 10- and 20-unit exponential moving averages (EMAs). From here, the next strong dynamic resistance will be the 50 EMA (currently marking 95.80), and we would need to go as far back as December 2022 for the most recent breakout from that level.

The weekly RSI at 53.47 is still in the "neutral" area; however, it is trending up and following the direction of prices. For now, all signs are pointing upwards.

Best European Commodity Performers This Week

Robusta Coffee 10-T (RMN24), +11.67%: In the last four sessions, we see a confident bullish rebound, breaking all the 10, 20 and 50 averages. Mind the 4,000 level, which so far has acted as good resistance. Breaking it upwards will set the next target to 4,300.

This week's announcement that Vietnam 2024/2025 robusta coffee crop will be the lowest in 13 years (24 million bags) is fueling the last rebound. There are projections of yet another robusta global deficit for 2024/2025 of 4.6 million.

Brazil production in contrast has been revised up from Conab (Brazil's National Supply Company) to up to 58.8 bags. Given the dryness reports in Mina Gerais that might bit too optimistic, and the supply might be tight for this season.

Rapeseed (XRQ24), +4.54%: European Rapeseed is in a solid uptrend that started on Feb. 26 and has used the 10 and 20 EMA as effective support. The daily RSI at 62.77 is still validating the trend.

EU Commission grain trade data shows that rapeseed imports are below last year's volume. 2023-24 imports are at 4.9 Mt, which is 1.9Mt less than previous season.

Australia has exported 60% less to the EU as a result of dryness in a context of strong demand from EU crushers that are hitting record volumes. Fundamentals are clearly supporting this trend for now.

Worst European Commodity Performers This Week

Crude Oil Brent (CBQ24), -3.12%: Brent contracts are trading below the 10, 20, and 50 EMAs with a clear bearish bias in the last 5 sessions. The 79.5-80 area should provide a first support it the trend continues.

Demand is low currently at the start of the driving season, and with no close prospect of interest rate cuts to stimulate it. All attention is now focused on the next OPEC meeting on June 1.

VSTOXX Futures (DVM24), -25%: With lows hitting the 13 level, we are approaching extremely low volatility in the equity sector, down to levels not seen since January 2024. Previous to that, volatility had remained

higher since January 2020.

The 50 EMA indicates 19, so this could be a good time for those looking to pick up cheap options on equities.

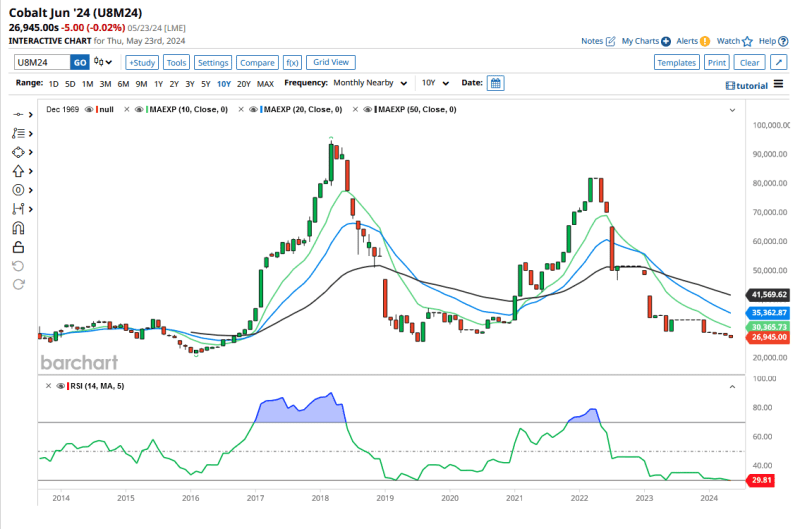

Cobalt (U8M24), -2,44%: Cobalt has its production concentrated in two countries. It had its last boom in May 2022 (high at 81,940), and a subsequent crash at the current 26,945.

The metal is near its cheapest in the last 5 years, and China has taken notice. Cobalt is a byproduct of copper and nickel production, and it's in demand among the defense, electric vehicle (EV), and communication industries.

There is a massive surplus in the market in 2024, which has produced the current crash, with overproduction reported in the Republic of Congo and Indonesia. Congo supplies 77% of the global market, with around 170,000 tons just last year, and the current surplus in the market for 2024 is estimated at 35,000 tons.

The crash in prices has not stopped Chinese miners in Congo, as they benefit from state support. China's state stockpiler is ramping up demand, as it plans to acquire 15,000 tons at around USD$12.50-$13.80 per pound for stockpiling, and presumably for military use.

At the current levels, and with expected EV demand picking up, we could be close to a turnaround in this bear market.

How to Trade Cobalt

Futures contracts on this metal have very low liquidity, and the only realistic options for retail traders are on the ETF sector - though there is nothing specifically on cobalt 100%, either miners or on futures.

That said, two ETF options are the Amplify Lithium & Battery Technology ETF (BATT) and the ProShares S&P Global Core Battery Metals ETF (ION).

Markets on cobalt are ripe with opportunity at these levels; however, be sure to mind the liquidity if you are going to jump in.

On the date of publication, Cesar Marconetti did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.