Palantir Inc. (PLTR) made strong free cash flow (FCF) margins over the last year, and FCF could hit $900 million. As a result, PLTR stock could be worth 27% more at $26.92 per share. One way to play this is to short out-of-the-money (OTM) puts.

I discussed this in my last Barchart article on May 7, “Palantir Stock Is Down on Results, But Value Investors Can Take Advantage of This Dip.” This was after the company released its Q1 earnings on May 6.

Strong FCF Margins Over the Last Year

That report showed that its Q1 FCF margin fell from 50% in Q4 2023 to 23.4% in Q1. As I pointed out, this could account for some of the stock's recent “treading water,” as it may have been disappointed in the lower margins.

But this does not consider seasonal effects with this software intelligence company's orders. For example, most of its customers are government agencies and they tend to renew once a year. I pointed this out in a recent GuruFocus article.

So, looking back over the trailing 12 months (TTM), Palantir's FCF margins were 27.5%. This was down a bit from the 33% TTM FCF margin in Q4, but not as much as the 50% FCF margin it made in Q4.

So, going forward, we can project that the company may be able to make a 30% FCF margin. Analysts estimate sales will average about $3 billion over this year and next. That implies that free cash flow could reach $900 million (i.e., 30% x $3 billion).

That is 23% higher than the $730.5 million in FCF it generated in 2023. In other words, PLTR stock could be worth substantially more based on this estimate.

Price Targets

For example, take the $900 FCF estimate and apply a 1.5% FCF yield metric. That results in a $60 billion market cap estimate (i.e., $900m/0.015).

That means that if the company were to pay out 100% of its FCF the market would likely give it a 1.5% dividend yield.

This is 27% more than its existing $47.2 billion market cap. In other words, PLTR stock could be worth $26.92 per share (i.e., 1.27 x $21.20 per share today).

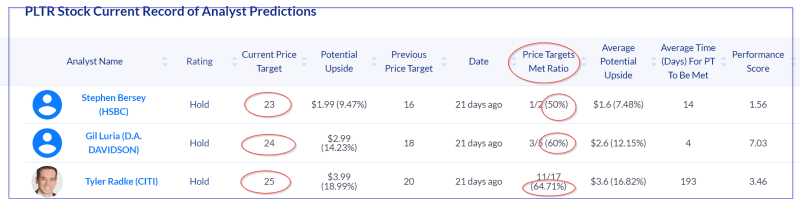

Other analysts agree. For example, the table below from AnaChart.com, a new sell-side analyst tracking service, shows that three of the top-performing analysts on the stock have higher price targets:

It shows that the DA Davidson analyst has a $24 price target and the Citi analyst has a $25 price target. Both of these analysts have high-performance ratios. Their price targets have been hit 60% and 64.71% of the time, respectively.

The bottom line is that PLTR stock could be worth more than its price today. This may come to the fore when it produces Q2 earnings. Until then the stock may continue treading water.

Shorting OTM Puts

One way to play this is to sell short out-of-the-money put options in nearby expiration periods. I discussed this in my last article, as mentioned above, on May 7.

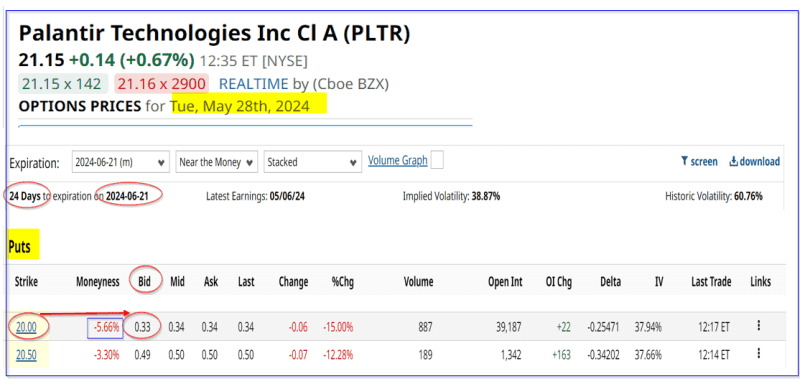

I suggested shorting the $20.00 strike price puts expiring on May 31, which was 3 weeks away. At the time PLTR stock was at $21.73 and the puts were trading for 37 cents on the bid side. That provided an immediate yield of 1.85% (i.e., $0.37/$20.00).

Today those puts are almost worthless, trading for 3 cents. So, it makes sense to roll this trade over. This involves setting two new trades: “Buy to close” this put option play and do another “Sell to Open” trade for a strike price and expiry period 3 weeks away.

For example, look at the June 21 expiration period and the $20 strike price put option. It trades again for 33 cents. That represents a 1.65% (i.e., $0.33/$20.00) for a strike price that is 5.66% out-of-the-money.

Here is what that means. The investor first secures $2,000 in cash and/or margin with their brokerage firm. Then they can enter an order to “Sell to Open” 1 put contract at $20.00. The account will receive $33.00. That represents an immediate yield of 1.65%.

So, if this can be repeated every 3 weeks over a quarter, the investor can make $132, or 6.6% of the $2,000 invested each time. That is a very good expected return.

In other words, existing shareholders can make extra income. For those that have not yet bought PLTR stock, it provides a way to buy in at a cheaper price (i.e., with extra income) in case the stock falls.

The bottom line is that PLTR stock looks cheap here and shorting OTM puts is a good way to play this.

More Stock Market News from Barchart

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.