By Kyiv School of Economics

Russia’s oil export revenues remain high as energy sanctions fail to offset rising global prices. Improved external dynamics are helping to stabilise the ruble and support the budget. Although there is a risk that Russia will face economic vulnerabilities in the future due to reduced macroeconomic buffers, more action is needed now to stop Russia’s brutal war in Ukraine, according to the May edition of the KSE Institute’s chart book.

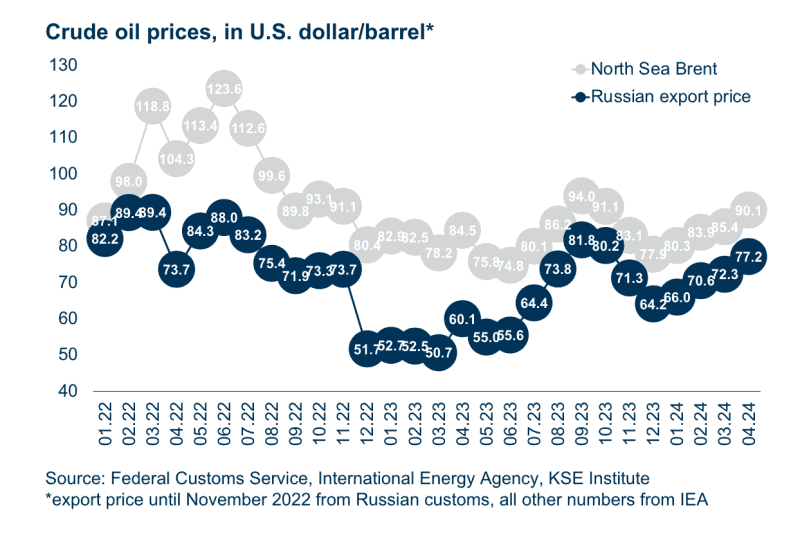

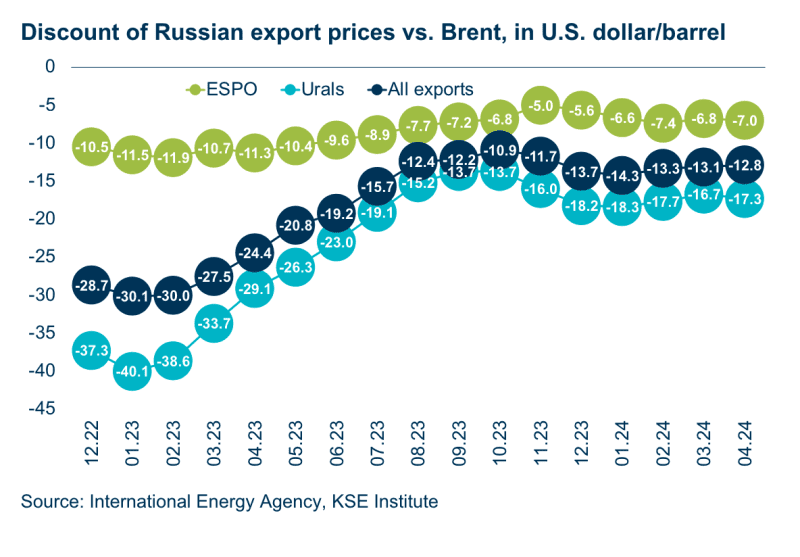

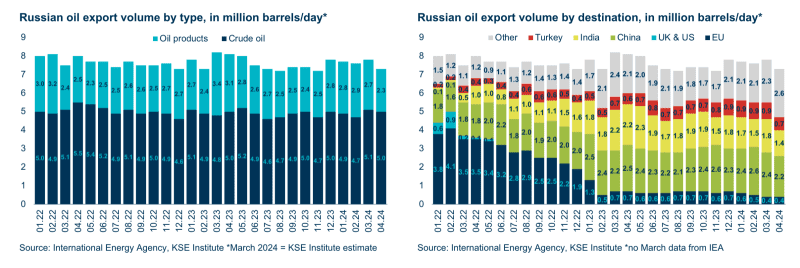

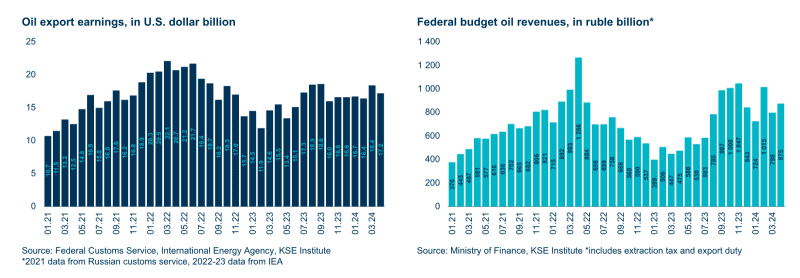

Higher oil prices have supported Russia’s export earnings, with oil revenues reaching $17.2bn in April. Global oil prices continued to rise, with Brent reaching an average of $90/barrel. Meanwhile, the Russian crude export price was $77.2/barrel. As the US Treasury’s vessel designation campaign remained on hold (with 41 tankers sanctioned), the discount on export prices was essentially unchanged. Altogether, Russia has been generating substantial extra earnings due to these price dynamics. From January to April 2024, crude oil and oil product exports averaged $570mn per day—a 22% increase over the same period in 2023. At this rate, oil and gas revenues will fully cover the military budget this year.

Russia’s trade surplus dropped by half in April compared to March due to weaker exports, especially non-oil ones. Despite monthly fluctuations, the external environment is much more supportive than a year ago. The trade surplus grew by 14%, from $37.2bn in January-April 2023 to $43.7bn in the same period of 2024. The current account surplus more than doubled from $15.6bn to $31.7bn between March and April as deficits in services, income, and transfers declined. Along with actions taken by the CBR, improved foreign currency inflows have stabilized the ruble.

These strong revenues are helping to keep the fiscal situation stable. In the first four months of the year, Russia’s federal budget deficit reached RUB1.5 trillion– 92% of the full-year target, but less than half the deficit in the same period in 2023.

Revenues rose sharply (50%) – with oil and gas revenues up 82% and non-oil revenues up 37% – more than offsetting higher expenditures (22%) due to increased war spending. Although the budget showed a deficit of around RUB900mn in April, Russia is on track to meet its 2024 target. At current oil export prices, Russia is unlikely to face significant external imbalances or fiscal constraints.

Looking ahead, however, Russia is likely to encounter economic vulnerabilities due to reduced macroeconomic buffers. If increased economic sanctions succeed in reducing energy revenues in the coming months, Russia’s underlying vulnerabilities could quickly resurface. After spending almost $54bn of the NWF’s liquid assets since the start of the full-scale invasion, only gold and yuan remain, which cannot easily be used at scale to finance the budget. This would force the regime to rely on higher domestic debt issuance, driving up borrowing costs. At the same time, the immobilization of nearly $300bn in CBR reserves seriously constrains the authorities’ policy space to manage the economy.

To erode Russian macroeconomic stability and curb its ability to wage war, stronger and more decisive actions from Ukraine’s allies are needed.

Read the full report here.

The price per barrel of oil has been rising

Russia oil export volumes by type and destination

Russian oil export earnings in USD and RUB

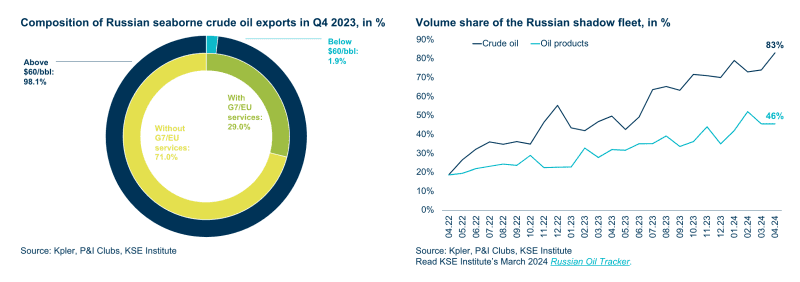

Composition of seaborne exports by shadow fleet share and oil price cap avoidance

**

The Kyiv School of Economics (KSE) is a bne IntelliNews media partner and a leading source of economic analysis and information on Ukraine. This content originally appeared on the KSE website.