Investing in growth stocks is often considered advantageous for several reasons, particularly for investors seeking long-term capital appreciation. Most growth stocks in emerging industries have the potential to provide significant returns if held for an extended period.

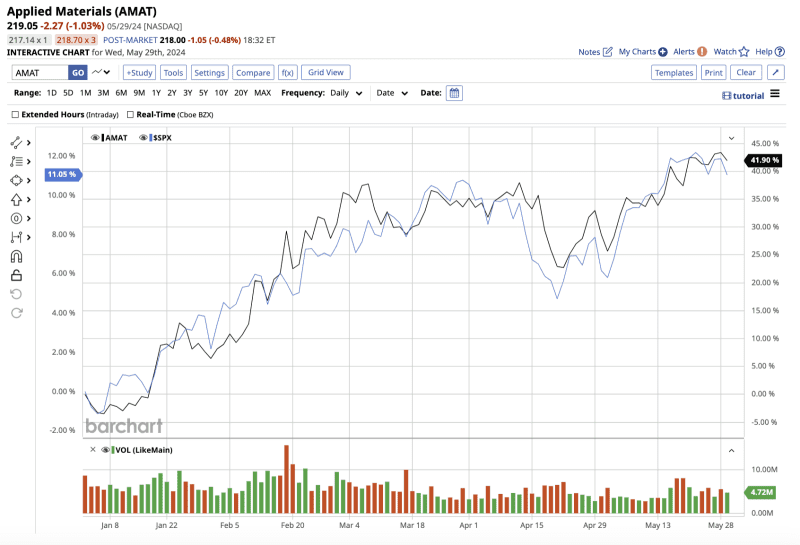

As the artificial intelligence (AI) frenzy continues to boost the semiconductor industry, companies involved in this space have benefited from the explosive growth. One such emerging growth stock is semiconductor fabrication equipment supplier Applied Materials (AMAT), which has gained 34.6% year-to-date, outpacing the S&P 500 Index’s ($SPX) gain of 10%.

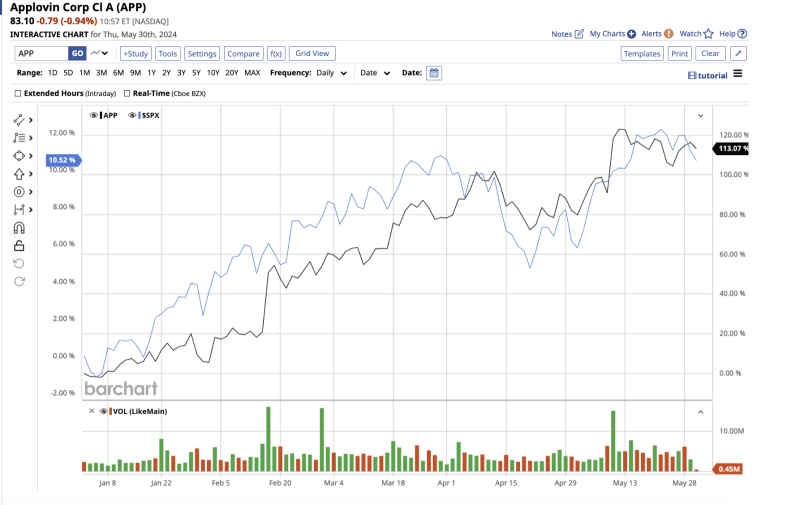

Meanwhile, California-based tech company AppLovin’s (APP) stock has gained a whopping 110% YTD, crushing the broader market in comparison. Wall Street analysts have rated both stocks a “moderate buy,” expecting a double-digit upside based on the high price estimate. Let’s find out why.

Growth Stock No. 1: AppLovin

AppLovin (APP) is a leading platform that helps mobile developers grow, market, and monetize their apps. The company's business model is divided into two main segments: software platforms and apps. The software platform includes AppLovin's robust ad network and app discovery tools, while the apps segment includes a collection of owned and operated mobile games.

AppLovin has reported significant revenue growth, thanks to rising demand for mobile advertising and the success of its apps. The company's revenue model is based on both advertising fees and in-app purchases within its gaming portfolio. Over the past five years, its revenue has increased at a compounded annual growth rate (CAGR) of 27%.

In its most recent first quarter, total revenue of $1.06 billion grew a massive 48% year-over-year. The software platform, which contributes to a chunk of total revenue, grew 91% to $678 million due to improvements in AXON technology. In addition, Apps revenue increased 5% year over year.

While AppLovin has experienced strong revenue growth, profitability has been mixed due to high operational costs and investments in growth initiatives. However, the company reported a net profit of $236 million in the first quarter, up from a net loss of $4.5 million in the year-ago quarter.

AppLovin's cash and cash equivalents totaled $436 million at the end of the quarter, with $35.5 million in short-term debt. The company generated $388 million in free cash flow (FCF).

As with any evolving company, AppLovin’s focus on scaling its platform and optimizing its ad network is expected to improve profit margins over time. For investors looking to capitalize on the growth of mobile advertising and gaming, AppLovin stock offers a compelling opportunity.

Here's what analysts covering the stock predict for the next two years:

- Revenue and earnings are expected to increase by 33.2% and 198.5%, respectively, in 2024.

- Revenue and earnings are expected to increase by 11.6% and 27.3%, respectively, in 2025.

Overall, Wall Street rates APP stock a “moderate buy.” Of the 16 analysts covering APP stock, 10 have rated it a “strong buy,” one has a “moderate buy” recommendation, four suggest a "hold,” and one rates it a “strong sell.”

Closing at $83.89 yesterday, APP stock has surpassed its mean price target of $83.48. However, its high target price of $105 suggests the stock could rise 25.4% over the next 12 months.

Growth Stock No. 2: Applied Materials

Applied Materials (AMAT) offers equipment, services, and software for manufacturing advanced semiconductor chips. Applied Materials has demonstrated strong financial health over the years, with consistent revenue growth, strong margins, and a solid balance sheet. The company has capitalized on the growing demand for semiconductors, driven by trends such as 5G, AI, cloud computing, and the Internet of Things (IoT). Revenue increased from $14.6 billion in 2019 to $26.5 billion in 2023.

In the most recent second quarter of 2024, net revenue remained flat at $6.65 billion. However, it exceeded the consensus estimate by $111.3 million. Adjusted earnings per share rose 5% year on year to $2.09, exceeding expectations by $0.10.

The company generated $1.13 billion in adjusted FCF, which it used to pay $1.09 billion in dividends and share repurchases. The forward dividend yield of 0.73% is lower than the sector average of 1.37%, making it less appealing. Nonetheless, a forward payout ratio of 16% suggests that dividends may increase as earnings rise.

Management expects third-quarter revenue of $6.65 billion, plus or minus $400 million. Additionally, adjusted earnings per share could range from $1.83 to $2.19. Analysts' Q3 estimates are within the same range.

While management didn't specify their expectations for the year, analysts covering the stock predict that revenue and earnings will rise by 1.47% and 3.6%, respectively.

As semiconductor demand grows, with AI and the tech sector progressing rapidly, Applied Materials is poised to take advantage of this growing demand for advanced chips. Analysts predict 2025 could be a better year, with revenue and earnings increasing by 11.5% and 15.3%, respectively.

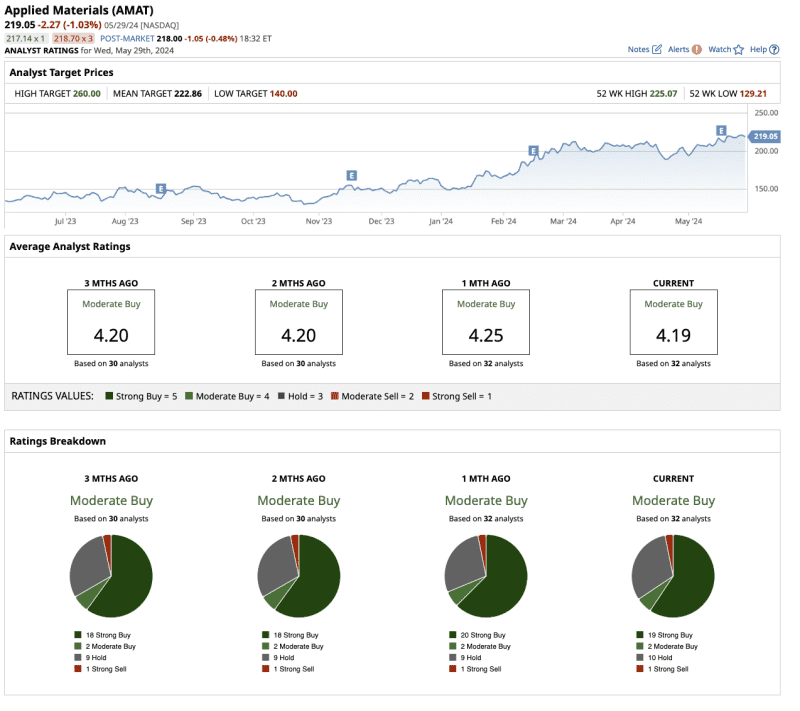

Overall, Wall Street rates AMAT stock a “moderate buy.” Of the 32 analysts covering AMAT, 19 have rated it a “strong buy,” two have a “moderate buy” recommendation, 10 suggest a "hold,” and one rates it a “strong sell.”

AMAT stock is hovering around its mean price target of $222.86, implying a potential upside of around 2% from current levels. Plus, its high target price of $260 suggests the stock could go as high as 19.2% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.