Every great stock began its journey when it was undervalued and overlooked. Nonetheless, a few savvy investors recognized their growth potential and invested in them when they were cheap. As a result, when these businesses reached their full potential, those early investors earned enormous profits.

Here are two examples of stocks under $100 that do not appear to be particularly valuable at the moment, but could generate significant returns in the future.

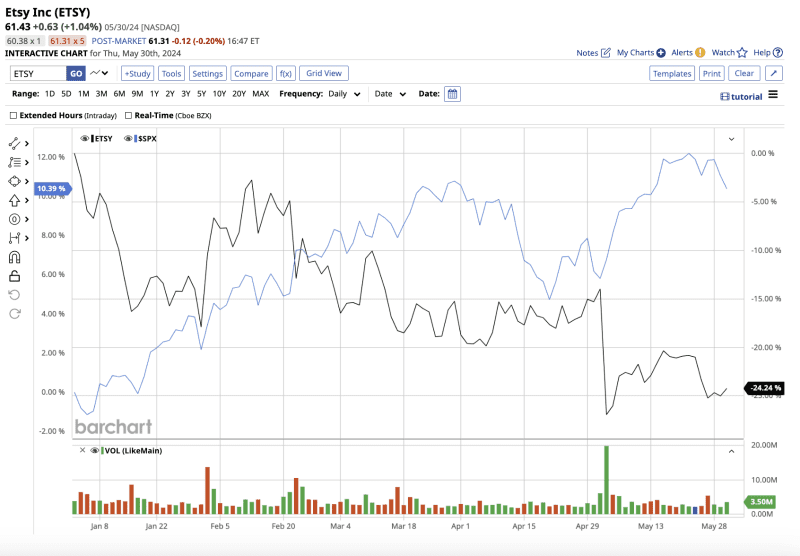

Etsy Stock

The first on my list is Etsy (ETSY), a unique two-sided online marketplace that connects buyers and sellers. With its platform, the company promotes creativity and small business growth by providing unique, handcrafted goods. Etsy operates in the United States, the United Kingdom, Germany, Canada, France, Australia, India, Italy, Spain, and a few other countries. In fact, Statista reports that between 2015 and 2023, Etsy's buyer app was downloaded 53 million times in the U.S. alone.

Valued at $7.18 billion, ETSY stock has dipped 23.6% year-to-date, compared to the S&P 500 Index's ($SPX) gain of 8.9% \- presenting an opportunity to buy it on the dip.

Etsy's financial performance has been volatile, influenced by market trends, consumer behavior, and general macroeconomic conditions. The pandemic market boosted Etsy, as online sales peaked during the lockdown. Although the post-pandemic market has slowed Etsy's sales, the company overall continues to grow steadily.

In 2023, Etsy reported revenue of $2.7 billion, reflecting a 7.1% increase from the previous year. An increase in active buyers and sellers, as well as higher gross merchandise sales (GMS), drove this growth.

The company's net income has also improved, reaching $307.5 million in 2023, up from a loss of $694 million in 2022.

In the most recent first quarter, Etsy demonstrated resilience by adding 5.7 million new buyers to its platform. The company also reactivated 6.3 million buyers, a 5.9% increase over the previous year period. While revenue rose slightly by 0.8% to $645.9 million, GMS fell 3.7% to $3 billion due to macroeconomic conditions affecting consumer spending. Net income fell by $11.5 million to $63 million in the quarter.

Etsy operates in a fiercely competitive e-commerce market against giants like Amazon (AMZN), eBay (EBAY), and Shopify (SHOP). Despite this, Etsy's one-of-a-kind business model of selling handcrafted, vintage, and custom-made goods has enabled it to maintain a loyal customer base of habitual buyers. The platform's emphasis on individuality and creativity distinguishes it from competitors, who typically sell mass-produced items, often with no regard for quality.

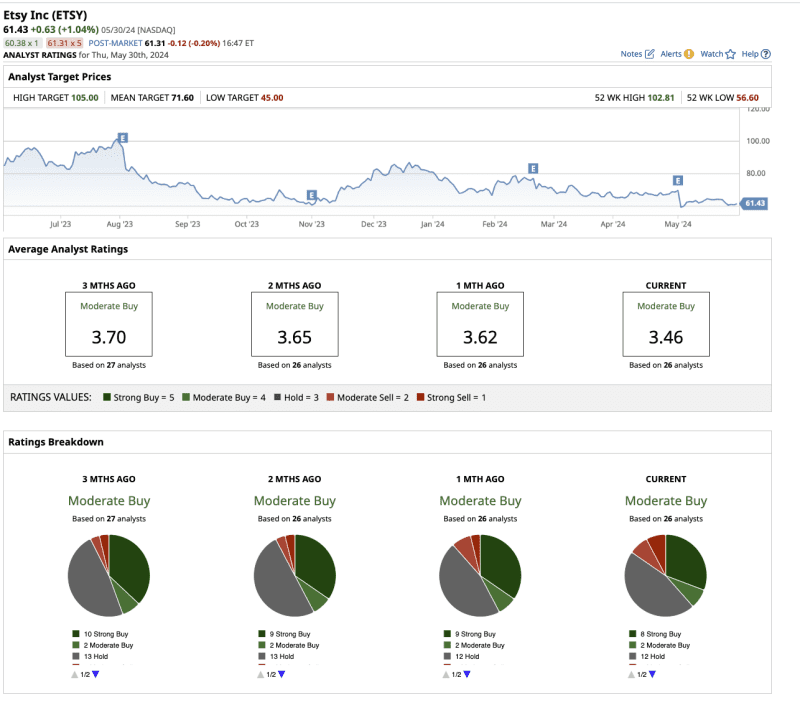

Analysts covering Etsy stock expect earnings to fall 6.8% in 2024 before recovering and increasing by 7.8% in 2025. Etsy, trading at 12 times forward 2025 earnings, is a reasonable long-term buy and hold.

Overall, Wall Street rates ETSY stock as a "moderate buy." Of the 26 analysts covering ETSY stock, 8 rate it a "strong buy," two rate it a "moderate buy," 12 recommend a "hold," two rate it a "moderate sell," and two rate it as a "strong sell."

The mean price target for ETSY stock is $71.6, implying a 15.7% upside potential. However, the stock's high target price of $105 suggests that it could rise by nearly 70% over the next year.

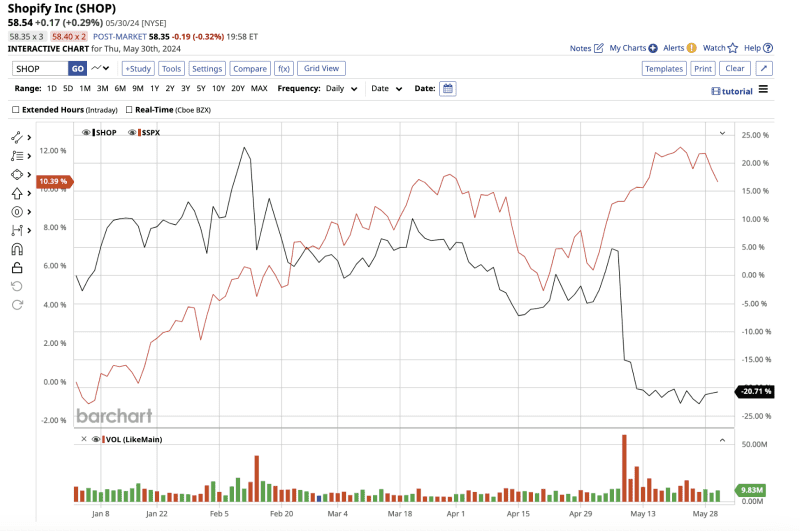

Shopify Stock

Shopify (SHOP), valued at $75 billion, is a much bigger player in the e-commerce space than Etsy. It offers a platform for businesses of all sizes to build and manage online stores.

Despite reporting a strong first quarter, Shopify's stock is down 25.7% year to date, underperforming the overall market.

Shopify's financial performance in recent years has been strong, led by its rapid growth and expanding market presence. Between 2019 and 2023, the company's revenue grew from $1.5 billion to $7.1 billion.

The company reported revenues of $7.1 billion in 2023, a 26% increase over the previous year. This impressive growth was fueled by new merchants' continued adoption of its platform and increased sales from existing customers.

The company's net income per share stood at $0.10, compared to a loss of $2.73 per share in 2022, showcasing improved profitability. Shopify's strong performance is further highlighted by its gross merchandise volume (GMV), which reached $235.9 billion in 2023, an increase of 20%. GMV reflects the extensive use of Shopify's platform by merchants worldwide.

In the most recent first quarter, revenue increased 23% to $1.9 billion, driven by a 23% increase in GMV. Shopify's monthly recurring revenue increased by 32% as its subscription plans continued to grow.

Management stated that the company generated $232 million in free cash flow (FCF), representing a FCF margin of 12%. Management anticipates a high-teens percentage increase in revenue in the second quarter compared to the second quarter of 2023. The free cash flow margin target remains the same as in Q1 2024.

Shopify's strategic initiatives are geared towards sustaining growth and increasing shareholder value. Furthermore, the company is also using artificial intelligence (AI) and machine learning to improve the platform's capabilities.

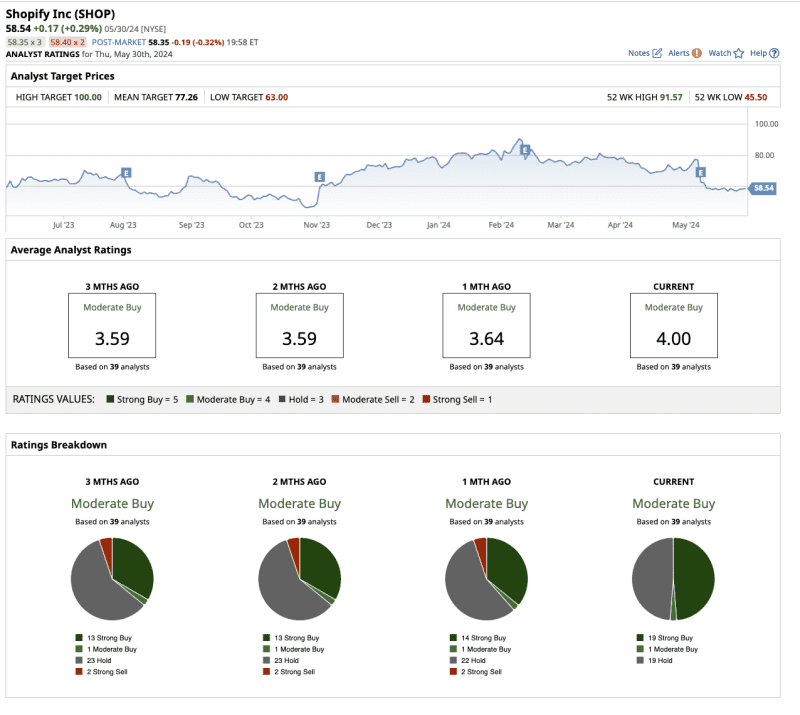

Analysts covering Shopify stock expect revenue and earnings to increase by 21.0% and 35.4% in 2024. Revenue and earnings could further increase by 20% and 28% in 2025.

Following the recent stock decline, Shopify is now valued at eight times forward 2024 estimated sales. Shopify is currently a reasonable buy, compared to its five-year historical average of 27 times sales.

Recently, Wells Fargo analyst Andrew Bauch reiterated his "buy" rating on the stock, citing the company's focus on long-term growth over immediate profitability. The analyst's price target for the stock is $70. In addition, Goldman Sachs upgraded SHOP to "buy" from "hold" with a target price of $74.

Overall, Wall Street rates SHOP stock a “moderate buy.” Of the 39 analysts covering SHOP, 19 have rated it a “strong buy,” one has a “moderate buy” recommendation, and 19 suggest a "hold.”

Based on its mean price target of $76.87, the stock has an upside potential of 32.2% from current levels. Plus, its high target price of $100 suggests the stock could rise as high as 72% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.