While the broader market has hit record highs in 2024 and the Nasdaq Composite ($NASX) is sitting on double-digit YTD returns, some sections of the market trade considerably below their all-time highs. Electric vehicles (EVs) – once a sunshine sector that attracted quite a bit of interest from investors – is one such industry.

While analysts have toned down their expectations for the group, Li Auto (LI) is one name in the space that experts expect to nearly double over the next year. Is LI a growth stock worth buying, despite the continued turmoil in the EV industry? We’ll discuss in this article.

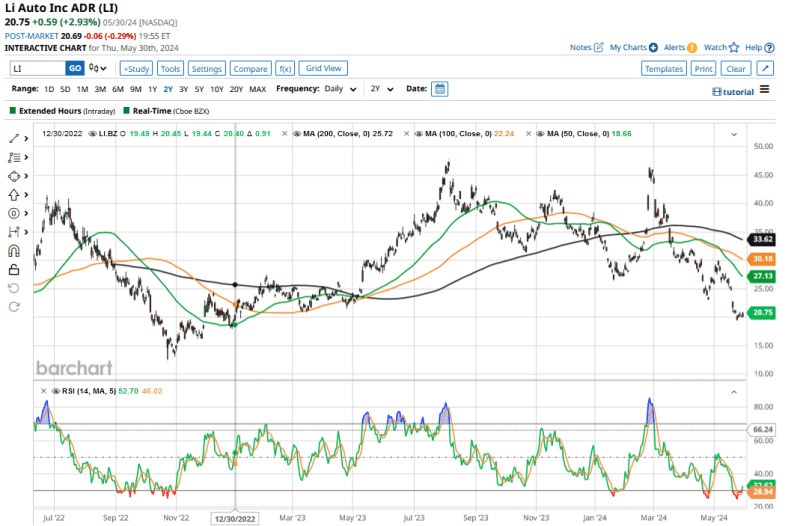

EV Stocks Have Crashed in 2024

With a YTD loss of almost 46%, LI is among the worst-performing EV stocks this year. Things haven’t been much better for its China-based peers; both NIO (NIO) and Xpeng Motors (XPEV) have lost around 40% each YTD.

Otherwise, Li Auto stands out among its peers for multiple reasons. While emerging Chinese EV companies have been struggling with delivery growth and burgeoning losses, Li Auto hit the milestone of becoming the first emerging Chinese EV company to surpass 600,000 cumulative deliveries and 50,000 monthly deliveries last year.

It has been a cash flow powerhouse, and generated free cash flows of $6.22 billion last year. This is unlike other competitors, who have been burning cash.

The EV Industry Slowdown Caught Up with Li Auto

Until about last year, Li Auto seemed immune from the slowing growth in the Chinese new energy vehicle (NEV) market. Notably, unlike NIO and XPEV - which sell only battery electric vehicles (BEVs) - Li was focusing on hybrid cars, and created a niche for itself in the premium market.

This year, the company launched its first BEV, the Li MEGA MPV, which did not receive the expected response from buyers. Li Auto admitted that MEGA's operating strategy was “mis-paced.”

The company has now delayed the launch of other BEV models, and plans to move forward only in 2025. After a tepid response to MEGA and the continued slowdown in the Chinese EV market, Li Auto also trimmed its 2024 delivery guidance to between 560,000 and 640,000 units, down from the previous guidance of 650,000-800,000 units.

Management expects to deliver between 105,000-110,000 vehicles in Q2. To hit its new delivery guidance for the year, Li Auto would need to deliver over 60,000 vehicles on an average every month in the back half of the year. That seems like a tall order, especially as the company has delayed the launch of new BEVs to 2025.

Analysts Expect Li Auto to Almost Double, Despite the Challenges

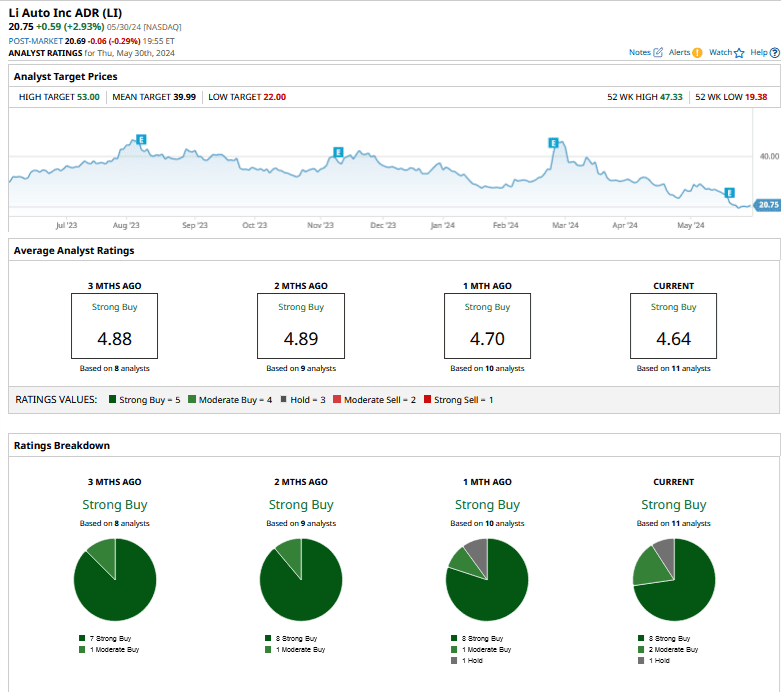

Despite the obvious challenges for Li Auto, Wall Street analysts are quite bullish on the growth stock. LI has a consensus rating of “Strong Buy” from the 11 analysts covering the stock. Only 1 analyst has rated it as a “Hold” or some equivalent, while 2 rate it as a “Moderate Buy.” The remaining 8 rate the stock as a “Strong Buy.”

Li Auto’s mean target price is $39.99, which is almost twice the current price level.

Chinese EV Companies Could Face Tariffs in the E.U.

Along with intensifying competition and a worsening price war at home, Chinese EV companies also face challenges in the overseas market. The U.S. market is practically shut for Chinese EV companies after President Joe Biden quadrupled the tariffs on EV imports from China to 100%.

The E.U. is also contemplating imposing tariffs on EV imports from China, which could be announced in June. Any European tariff would particularly hurt Chinese EV companies, as names like NIO and Xpeng Motors sell cars across the E.U.

Li Auto has so far been focused on the China market, and any European tariff wouldn’t hurt it specifically for now - even as it could dampen market sentiments more broadly towards Chinese EV companies.

Is Li Auto Stock a Good Buy?

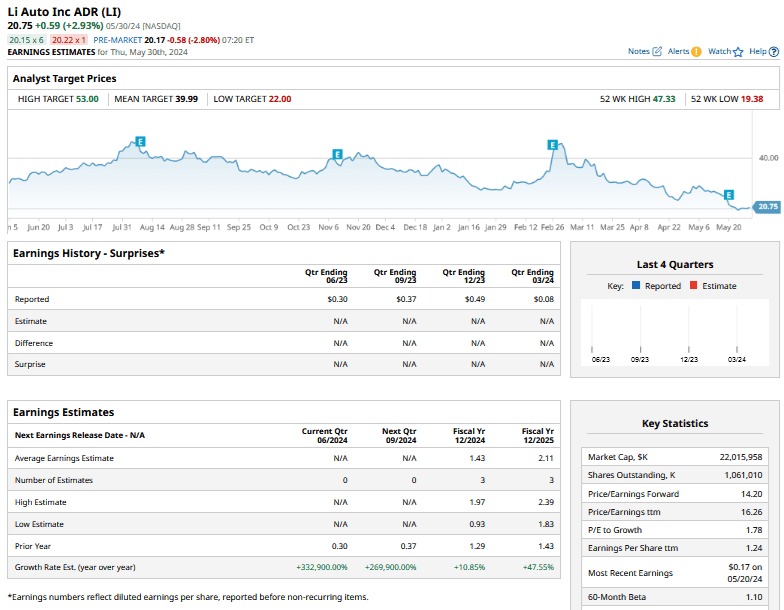

Analysts expect Li Auto’s earnings per share (EPS) to rise 10.8% YoY to $1.43. The automaker posted a net loss and negative free cash flows in Q1, as it has had to lower vehicle prices amid the intensifying price war in China. Also, its expenses have risen amid higher staff costs, as well as the expansion of its sales and service network.

Li's expenses could rise further as it builds its charging infrastructure, which it sees as a key to growing its EV business. According to China Merchants Bank International analyst Shi Ji, “The company has lowered its priority for 2024 profitability but has been focusing on laying a more solid foundation for BEV's success after the wrong expectation on the Mega.”

Profitability has indeed taken a backseat in the short term for Li Auto, which otherwise has the rare distinction of being profitable in an industry known for its perennial losses and cash burn.

In terms of valuation, Li Auto trades at a next 12-month price-to-earnings multiple of around 16x, which is not unreasonable for a company whose revenues are expected to rise nearly 24% in 2024. Also, while Li Auto’s profit growth is expected to be tepid in 2024, analysts expect it to rise 48% in 2025.

Li has a strong balance sheet and held $13.7 billion worth of cash and equivalents at the end of May. For context, the company’s market cap is just about $22.3 billion.

As an asset class, Chinese stocks are risky, considering the policy uncertainty under President Xi Jinping and the near-Cold War between the U.S. and China. However, tepid valuations and a strong growth outlook make Li Auto a name worth betting on.

However, for the stock to double from here, as its mean target price from Wall Street suggests, a lot has to go right for LI - both on the macro as well as the company-specific level. The company especially needs to prove that MEGA MPV was a mere blip, and it can come up with impressive BEV models.

On the date of publication, Mohit Oberoi had a position in: LI , NIO , XPEV . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.