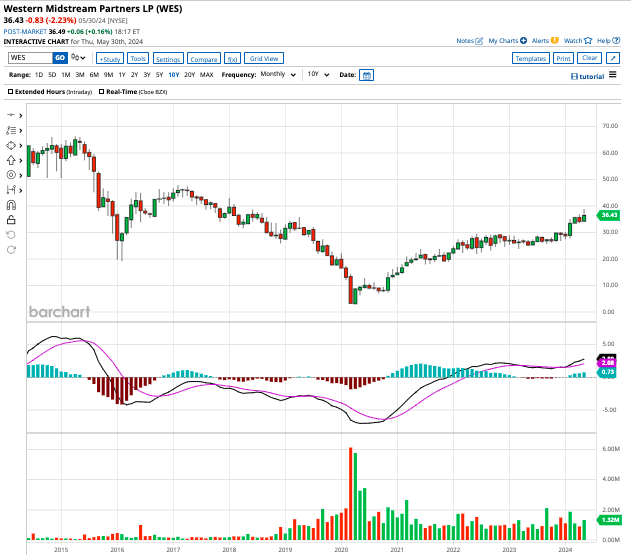

Due to the volatile nature of oil prices (CLN24), energy stocks are cyclical. That means oil and gas companies generally report outsized profits during periods of economic expansion, and experience a steep decline in cash flows when the economy enters a recession.

However, the global demand for oil and natural gas (NGN24) is expected to remain steady in the upcoming decade, despite the worldwide shift towards clean energy solutions - making midstream companies such as Western Midstream Partners (WES) a good investment choice right now. Let’s see why.

Is Western Midstream a Buy for its High Dividend Yield?

Valued at $13.86 billion by market cap, Western Midstream Partners owns, operates, acquires, and develops midstream energy assets. It is engaged in the business of gathering, processing, compressing, and transporting natural gas, condensate, natural gas liquids, and crude oil for Anadarko and other third-party producers or customers.

Despite an uncertain macro environment, Western Midstream reported a record natural gas throughput across its asset base in Q1 of 2024, as volumes rose by 2% sequentially. Its operated crude and natural gas liquid volumes also rose by 2%, while its operations in the Delaware Basin and New Mexico saw natural gas volume increase by 3% compared to Q4 of 2023.

These increases allowed the company to report an adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) of $609 million, an increase of 22% year over year. Comparatively, free cash flow rose by 60% to $225 million, allowing Western Midstream to raise its quarterly dividends by 52% year over year. The midstream company now pays shareholders a quarterly dividend of $0.875 per share, up from $0.575 per share last year, translating to a forward yield of 9.4%.

In Q1, Western Midstream paid out $223 million in cash distributions, indicating a payout ratio of almost 100%, which is quite high - but in line with other Master Limited Partnerships (MLPs). Given the 52% hike, Western Midstream’s quarterly dividend payout will rise to $340 million, which means it will pay close to $1 billion in dividends in the next three quarters.

Western Midstream expects operating cash flow to total $1.7 billion in the next three quarters and plans to spend less than $100 million in maintenance capital expenditures in this period, indicating a distributable cash flow of $1.6 billion. That suggests Western Midstream has the flexibility to spend on growth projects and lower its balance sheet debt, which should drive future cash flows higher.

What's Next for WES Stock?

Western Midstream sold five non-core assets for $790 million in Q1, the proceeds of which were used to lower $150 million in debt. So, the company is on track to end 2024 with a net-debt-to-adjusted EBITDA multiple of 3x, which is not too high.

Priced at 12 times forward cash flows, Western Midstream stock is quite cheap, given its high dividend yield and earnings forecast. In fact, Wall Street forecasts earnings for the company to expand from $2.60 per share in 2023 to $3.93 per share in 2024.

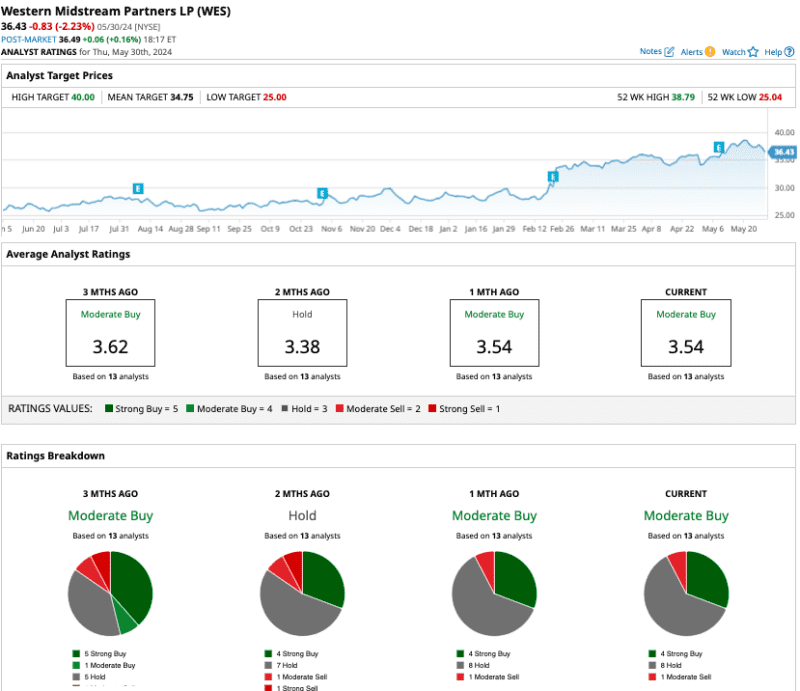

Out of the 13 analysts covering WES stock, four recommend “strong buy,” eight recommend “hold,” and one recommends “moderate sell.”

The average WES stock price target is $34.75, which is lower than the current trading price. However, the Street-high target price of $40 indicates expected upside potential of 7.2%.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.