Inflation data released earlier this week revealed a cooling consumer price index in May, with investors cheering data showing a 3.3% increase from last year. But despite the Fed's efforts to rein in inflation, it continues to linger above the central bank’s 2% target. With the Fed reducing its rate-cut forecast, the prolonged high rates aimed at curbing inflation could potentially hamper economic growth and even trigger a recession.

In this context, investors could consider buying three S&P 500 Value Index stocks: Zoetis Inc. (ZTS), Parker-Hannifin Corporation (PH), and Halliburton Company (HAL). With solid dividend payments backed by stable earnings and bullish analyst sentiment, these stocks could be ideal buy-and-hold investment candidates for investors seeking reliability and growth in this uncertain economic climate.

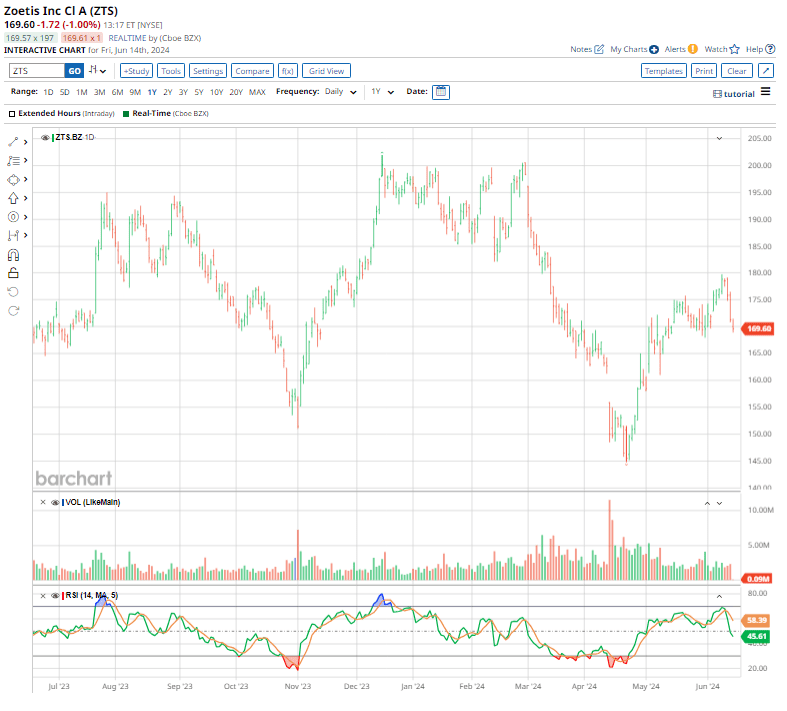

Value Stock #1: Zoetis

Commanding a market cap of about $78.2 billion, New Jersey-based Zoetis Inc. (ZTS) is a leading animal health company dedicated to animal care and supporting those who raise and care for animals, including veterinarians, pet owners, and livestock farmers. With over 70 years of innovation, Zoetis offers a top-tier portfolio and pipeline of medicines, vaccines, diagnostics, and technologies, impacting over 100 countries. The company is also enhancing its product range through strategic acquisitions and deals.

The company’s shares have pulled back 14% on a YTD basis.

On May 22, the company announced a quarterly dividend of $0.432 per share, payable to its shareholders on Sept. 4. Its annualized dividend of $1.73 translates to a 1.02% dividend yield. Additionally, it maintains a conservative payout ratio of 28.77%, providing ample room for future dividend increases.

Priced at 31 times forward earnings and 9.39 times sales, the stock trades lower than its own five-year averages of 36.24x and 10.65x, respectively.

The animal healthcare company soared 5.5% on May 2 after it revealed Q1 earnings results that sailed past Wall Street’s predictions on both the top and bottom lines. Revenue surged 9.5% year over year to $2.2 billion, while adjusted EPS of $1.38 topped estimates by almost 3%.

During the quarter, the company demonstrated strong performance across its key segments. Revenue in the U.S. segment surged to $1.2 billion, marking a significant 16% annual improvement. The international segment reported revenue of $1 billion, representing a 3% year-over-year jump.

Commenting on the company’s Q1 performance, CEO Kristin Peck stated, “our companion animal portfolio grew an impressive 20% operationally, fueled by our innovative franchises in pet parasiticides, osteoarthritis pain and dermatology."

For fiscal 2024, management anticipates revenue to range between $9.1 billion and $9.2 billion. Adjusted net income is expected to be between $2.6 billion and $2.7 billion, while adjusted EPS is forecast to land between $5.71 and $5.81.

Analysts tracking Zoetis project the company’s profit to climb 8.3% year over year to $5.76 in fiscal 2024 and rise another 9.9% to $6.33 per share in fiscal 2025.

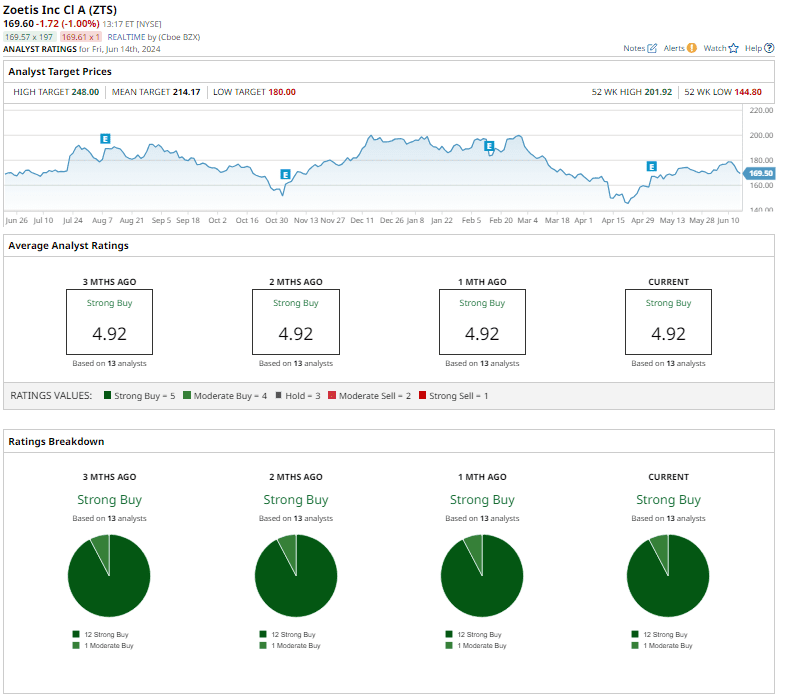

Zoetis stock has a consensus “Strong Buy” rating overall. Of the 13 analysts covering the stock, 12 suggest a “Strong Buy,” and the remaining one gives a “Moderate Buy” rating.

The average analyst price target of $214.17 indicates potential upside of 26.3% from the current price levels. The Street-high price target of $248 suggests that the stock could rally as much as 46.3%.

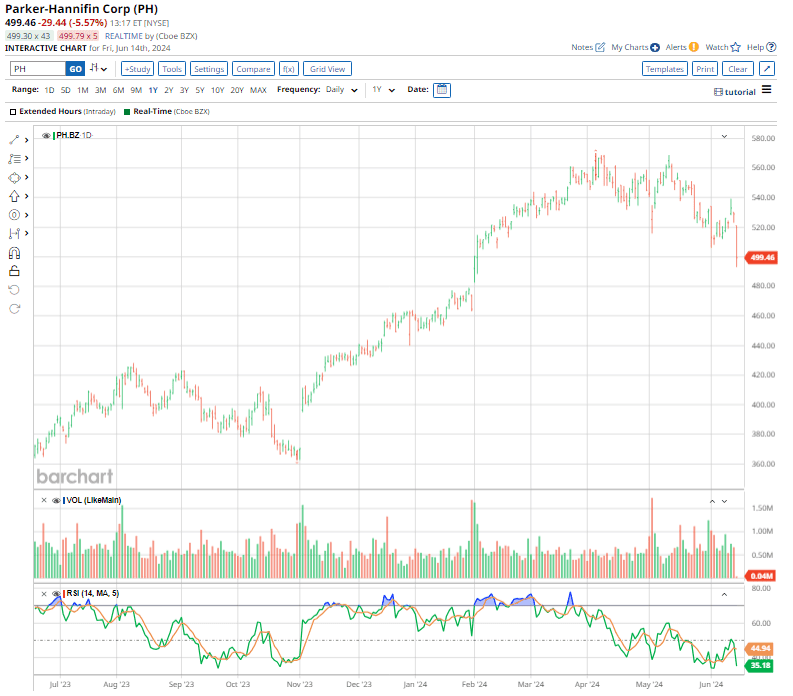

Value Stock #2: Parker-Hannifin

Founded in 1917, Ohio-based Parker-Hannifin Corporation (PH) designs, manufactures, and sells motion and control technologies and systems for diverse markets, including the mobile, industrial, and aerospace sectors, worldwide. With a market cap of $67.9 billion, the company operates through two segments: Diversified Industrial and Aerospace Systems.

Shares of Parker-Hannifin have surged 34.8% over the past 52 weeks, outpacing the broader S&P 500 Index’s ($SPX) gain of 23.8% over the same time frame.

With a remarkable 68-year streak of consecutive dividend increases, Parker-Hannifin is among the top five companies holding the record of the longest-running dividend increase in the SPX, supported by its strong cash flow and strategic investments.

On June 7, the company paid its shareholders a quarterly dividend of $1.63 per share, representing a 10% jump from the previous quarterly dividend. Its annualized dividend of $6.52 translates to a 1.30% dividend yield.

In terms of valuation, the stock trades at 21.05 times forward earnings and 3.59 times sales, lower than its industry peer, Illinois Tool Works Inc. (ITW), which trades at 23.32x and 4.44x, respectively.

On May 2, Parker-Hannifin revealed its Q3 earnings results, which topped Wall Street’s estimates. Its net sales reached $5.1 billion, up marginally year over year. Adjusted EPS of $6.51 jumped 9.8% annually, exceeding projections by 6.7%. As of March 31, cash and cash equivalents stood at $405.5 million.

During the quarter, sales from the Aerospace Systems Segment showed a strong annual improvement of 18%, reaching $1.4 billion.

Chairman and CEO Jenny Parmentier noted, “We delivered significant adjusted segment operating margin improvement with our Aerospace Systems Segment delivering another standout quarter. Our strong performance also led to record year-to-date operating cash flow.”

For fiscal 2024, management expects total sales growth of approximately 4% and a total segment operating margin of around 21.2%. Also, adjusted EPS is anticipated to range between $24.65 and $24.85.

Analysts tracking Parker-Hannifin project the company’s profit to reach $24.84 per share in fiscal 2024, up 15.3% year over year, and grow another 6.3% to $26.40 per share in fiscal 2025.

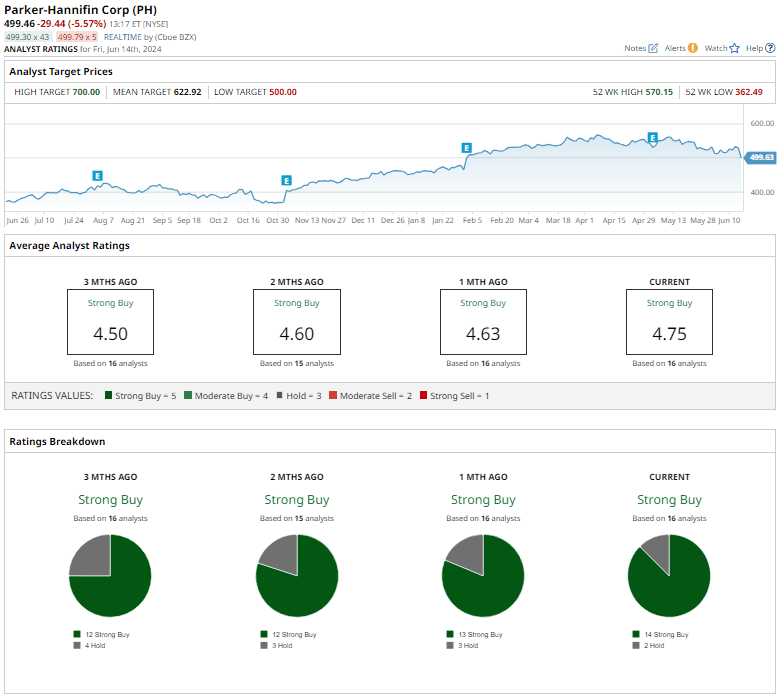

Parker-Hannifin stock has a consensus “Strong Buy” rating overall. Of the 16 analysts covering the stock, 14 suggest a “Strong Buy,” and the remaining two give a “Hold” rating.

The average analyst price target of $622.92 indicates a potential upside of 24.6% from the current price levels, while the Street-high price target of $700 suggests potential upside of about 40%.

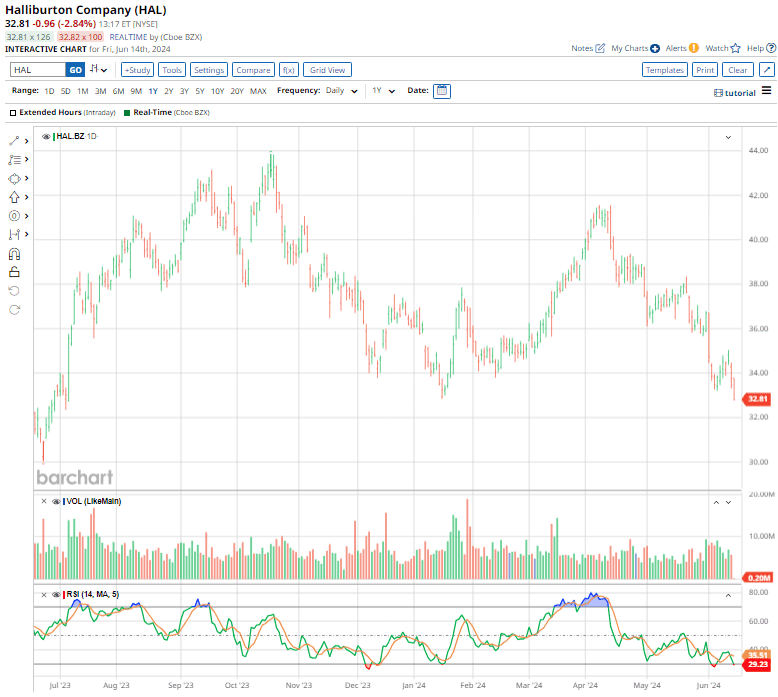

Value Stock #3: Halliburton

Founded in 1919 and headquartered in Texas, Halliburton Company (HAL) is one of the world’s largest oilfield service providers. Valued at a market cap of $29.9 billion, the company offers a wide range of equipment, maintenance, and engineering and construction services to the energy, industrial, and government sectors.

Over the past 52 weeks, shares of Halliburton have climbed about 2.5%.

On May 16, Halliburton declared a quarterly dividend of $0.17 per share, payable to its shareholders on June 26. Its annualized dividend of $0.68 translates to a 2.01% dividend yield. With a conservative payout ratio of 20.31%, the company has ample room for future dividend increases.

In terms of valuation, the stock is trading at 10.19 times forward earnings and 1.33 times sales, lower than its industry peers. And with above-average earnings growth projected over the next three to five years, the stock’s 0.88x price/earnings-to-growth (PEG) ratio is quite reasonable.

Halliburton revealed its Q1 earnings results on April 23, which exceeded Wall Street’s forecasts. Total revenue grew by 2.2% year over year to $5.8 billion, outperforming estimates by 2.1%. Additionally, adjusted EPS of $0.76 rose 5.6% annually, beating projections by 2.7%. As of March 31, the company generated $487 million in operating cash flow and $206 million in free cash flow.

During the quarter, Halliburton's completion and production segment generated $3.4 billion in revenue, marking a slight decrease compared to the previous year. However, operating income from the segment increased by 3% annually to $688 million. Meanwhile, the Drilling and Evaluation segment achieved 7% annual revenue growth, reaching $2.4 billion, while operating income rose by 8% year over year to $398 million.

"Activity in North America recovered from fourth-quarter lows, and our international business delivered its 11th consecutive quarter of year-on-year growth," commented Jeff Miller, Chairman, President, and CEO.

While the company didn’t offer any guidance, analysts tracking Halliburton expect the company’s profit to reach $3.39 per share in fiscal 2024, up 8.3% year over year, and rise another 18% to $4.00 per share in fiscal 2025.

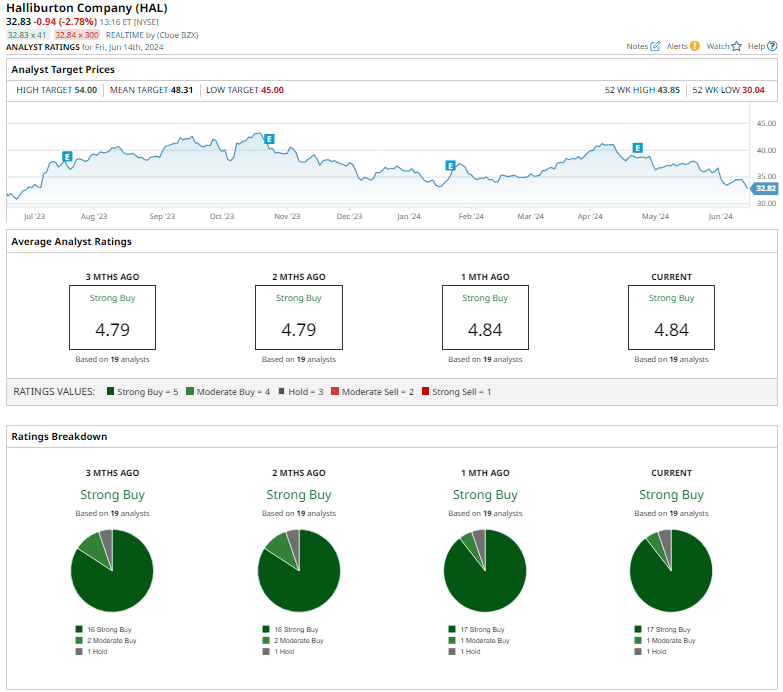

Halliburton stock has a consensus “Strong Buy” rating overall. Of the 19 analysts offering recommendations for the stock, 17 suggest a “Strong Buy,” one recommends a “Moderate Buy,” and the remaining one gives a “Hold” rating.

The average analyst price target of $48.31 indicates a notable potential upside of 47% from the current price levels. The Street-high price target of $54 suggests that HAL stock could rally as much as 64.4%.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.