Mega-cap stocks frequently attract the most attention from investors, due to the stability of their business models and their proven market value. However, small-cap companies have more room to expand than large-cap companies. They may be in the early stages of their growth cycle, which presents significant upside potential.

However, small-cap stocks can also be highly volatile. As a result, they are better suited for aggressive investors with a longer investment horizon who are willing to accept greater risk for the opportunity to earn higher returns.

Here are two cheap stocks trading under $30 with 43% to 76% upside potential over the next 12 months.

1. Digi International

Founded in 1985, Digi International (DGII) has been a provider of Internet of Things (IoT) connectivity products and services. It provides a variety of hardware and software solutions, such as embedded systems, routers, gateways, and network management tools. Digi's products are used in various industries, including industrial automation, energy, transportation, and healthcare.

Over the years, Digi’s revenue and profits have increased steadily, owing to the widespread adoption of IoT technologies. Revenue has increased from $254 million in fiscal 2019 to $444.8 million in fiscal 2023, while profits have risen from $0.35 to $0.67 per share during the same period.

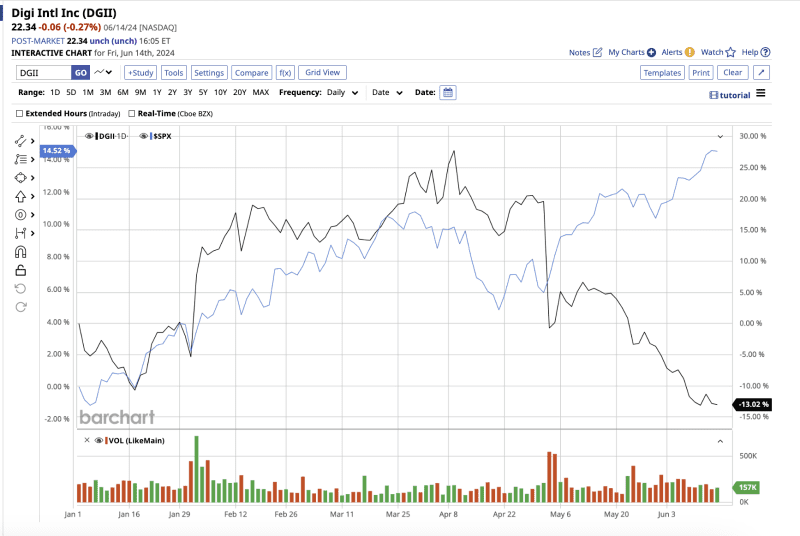

Valued at $812.6 million, Digi stock has fallen 14.6% year-to-date, underperforming the S&P 500 Index’s ($SPX) gain of 14.5%, due to lukewarm second-quarter fiscal 2024 results.

In the second quarter, net revenue fell 3% to $108 million, while adjusted net income was flat year on year at $0.49 per share. However, Digi's annual recurring revenue (ARR) increased by 11% to $110 million. The rising ARR of subscription-based business models like Digi's reflects consumer confidence in its products and services.

Management stated that they anticipate challenging macroeconomic conditions for the remainder of fiscal 2024, leaving them uncertain about when sales cycles will return to normal. As a result, management expects revenue to fall 5% year on year, despite a 5% increase in ARR.

Similarly, analysts predict that fiscal 2024 will be a difficult year for Digi, with a 4.8% drop in sales and a 0.7% decline in earnings. However, revenue and earnings are expected to rise by 4.5% and 7.6% in fiscal 2025, respectively.

Longer term, Digi International has a bright future ahead of it, as the IoT market is expected to grow exponentially. Over the next five years, the company expects to double its ARR and achieve $200 million in adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization).

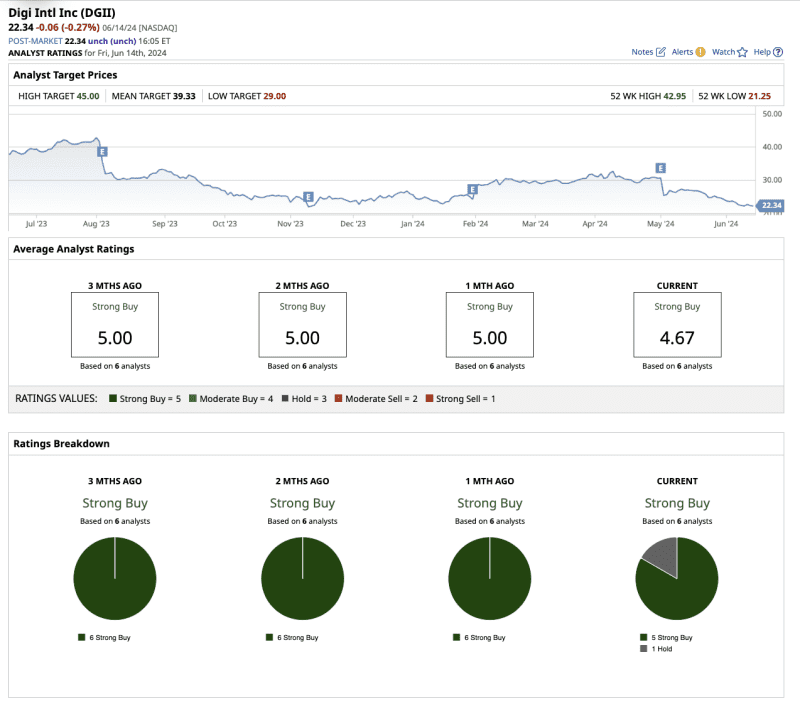

Analysts remain optimistic about the long-term potential of DGII stock, citing strong market fundamentals and Digi's proactive approach to innovation and market expansion. Overall, Wall Street rates DGII as a “strong buy.” Of the six analysts that cover the stock, five rate it a “strong buy,” and one rates it a “hold.”

The mean target price of $39.33 implies the stock has an upside potential of 76.4% over current levels. The high target price of $45 suggests the stock can rally 101.8% over the next 12 months.

2. Fiverr International

Fiverr International (FVRR) is a global online marketplace that connects freelancers with businesses that require various services. Fiverr revolutionized the gig economy by providing a platform for freelancers to list and sell their services, known as "gigs."

The gig economy is a new trend that is expected to continue. People are increasingly opting to freelance over working in an office because it allows them to travel the world while earning money. And Fiverr's financial performance reflects the growing trend of remote work and the gig economy.

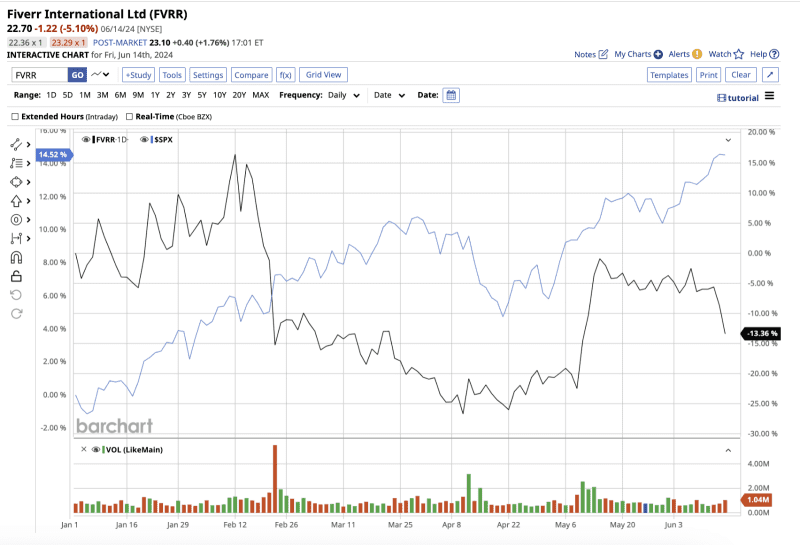

Valued at $877.4 million, Fiverr’s stock has fallen 18.2% so far in 2024, compared to the broader market's gain, providing an entry point for growth-oriented investors.

Without a doubt, Fiverr's revenue has soared, rising from $107 million in 2019 to $361 million by 2023. While prioritizing growth, the company has struggled to maintain consistent profitability. However, in the most recent first quarter, adjusted net income rose 44% to $0.52 per share, while revenue increased 6.3% to $93.5 million.

To drive long-term growth, Fiverr has expanded its offerings, allowing freelancers to charge higher prices and provide more complex services through artificial intelligence (AI) in a variety of categories, such as digital marketing, graphic design, writing, programming, and more.

For fiscal 2024, Fiverr expects 5% to 7% growth in revenue, in line with consensus estimates. Analysts covering the stock expect earnings to grow by 17% in 2024 and 10% in 2025.

The future of Fiverr International is bright, with the gig economy expected to expand as more businesses and individuals embrace remote and freelance work. Fiverr's strategic initiatives, which include platform enhancements, global expansion, and marketing efforts, position the company for long-term growth.

Analysts remain bullish on the long-term potential of FVRR stock because of its strong market fundamentals and its innovative approach to the freelance marketplace.

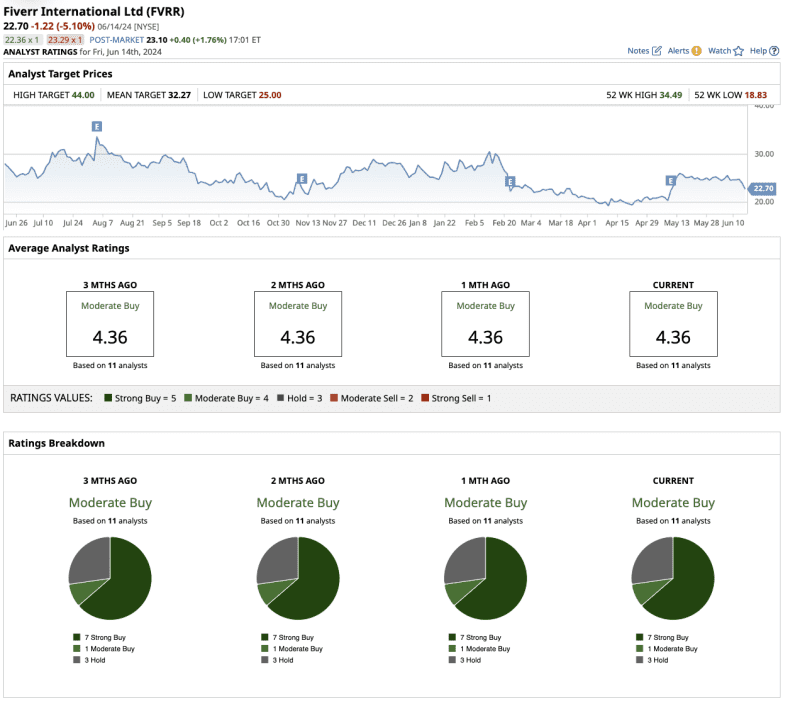

Overall, Wall Street rates Fiverr stock a “moderate buy.” Of the 11 analysts that cover FVRR, seven rate it a “strong buy,” one rates it a “moderate buy,” and three rate it a “hold.”

The mean target price of $32.27 implies the stock has an upside potential of 43.7% over current levels. The high target price of $44 suggests the stock can rally 95.9% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.