FactSet Research Systems (FDS), which supplies many Wall Street firms with data and research, produced a massive free cash flow (FCF) result in its latest quarter. If this keeps up, FDS stock could be deeply undervalued.

FDS closed at $423.73 on Friday. I estimate the stock is worth at least 68% more at $712 per share. This article will show why.

The company's results for its fiscal Q3, released on Friday, June 21, show that it had a massive gain in free cash flow and FCF margins. This augurs well for the company's valuation from now on.

Free Cash Flow Surging

The company's revenue rose 4.3% from the prior year and its adjusted operating margin hit 39.4%, up 340 basis points Y/Y. This fed straight into its free cash flow and FCF margins.

For example, FactSet generated almost $217 million during the quarter, on $552.7 million in revenue. That means that its FCF margin was an astounding 39.3%.

Here is how to look at this. For every dollar in revenue the company makes, it can save over 39 cents and keep it in the checking account, with no obligations or expenses left to pay. In effect, it's free to pay this amount out to shareholders.

As a result, the stock's valuation is worth a good deal more. Here is how that works out.

Estimating FactSet's Value

Analysts estimate that the company will generate between $2.2 billion and $2.32 billion in revenue between this fiscal year and next. That means its run rate revenue for the next 12 months (NTM) is $2.26 billion.

So, if we apply a 39% FCF margin against this we can estimate the company will generate $881 million in NTM FCF. But just to be conservative, let's use a 36% FCF margin. It follows that FactSet could at least make $814 million in FCF going forward.

That is useful in setting a valuation for the stock.

Target Price for FDS Stock

For example, what if the company paid this out in dividends? Right now, the company pays out $112 million each quarter, or about 52% of its $216 million in quarterly FCF. It has a 1% dividend yield at today's payout ratio.

So, theoretically, if the company paid out 100% of the FCF, the stock might have a 2% or 2.2% yield. Just to be conservative let's use a 2.5% FCF yield metric. In other words, if we divide the $814 million in FCF by 2.5% we get a market cap estimate of $32.56 billion.

That is 100% higher than its present $16.15 billion market cap. To be even more conservative, let's use a 3.0% FCF yield metric. That implies FDS stock is worth at least $27.13 billion (i.e., $814 million/0.03 = $27.133 billion).

This is still 68% higher than its existing $16.15 billion market cap. In other words, FDS stock is worth 68% more than $423.73 per share, i.e., a $712 price target.

Shorting OTM Puts

One way to play this is to sell short out-of-the-money (OTM) put options. This allows an investor to buy in at a lower price if the stock falls, as well as gain some extra income.

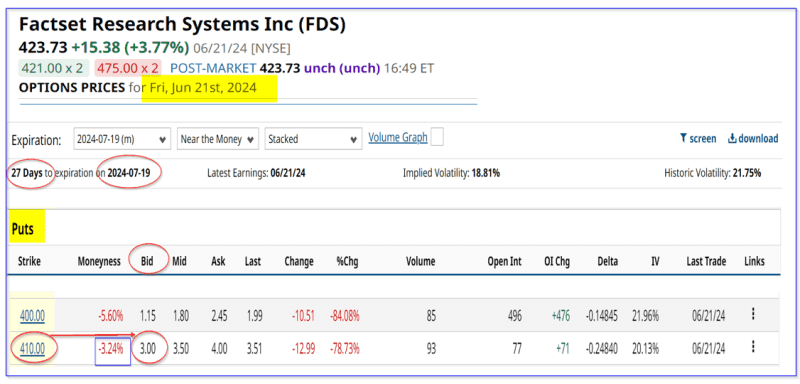

For example, look at the July 19 expiration period, 27 days from now. It shows that the $410 strike price puts trade for $3.00 on the bid side.

That represents an immediate yield of 0.73% for the short seller of these puts (i.e., $3.00/$410.00 = 0.0073). Here is how that works.

The investor first secures $41,000 in cash and/or margin with their brokerage firm. Then they enter an order to “Sell to Open” 1 put contract at $410 for expiry on July 19. The account will then immediately receive $300.00. This is because each contract represents 100 shares.

Then, as long as the stock stays above $410 on or before July 19, the account will not have an obligation to purchase 100 shares at $410.00. And no matter what happens the account keeps the $300.

That means that the effective breakeven buy-in price if the stock falls to $410, is $410-$3.00, or $408.00 per share. This means that the breakeven price is 3.7% below today's price. That provides good downside protection.

The point is that existing investors who already own FDS shares can make almost a 1% yield over the next month. Plus they have all the potential upside in the stock. But for other investors, it provides a disciplined way to buy, in case the stock falls.

The bottom line is that FDS stock is worth a good deal more than its present price, given its huge FCF margins. One way to play this is to buy the stock and also short OTM puts.

More Stock Market News from Barchart

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.