As the renewable energy sector continues to grow, investors have been increasingly drawn to solar energy stocks, anticipating substantial returns from this promising industry. However, a recent analysis from JPMorgan Chase (JPM) prompted a word of caution against two solar energy stocks - Enphase Energy, Inc. (ENPH) and SolarEdge Technologies, Inc. (SEDG).

Following the Intersolar Europe Conference 2024, JPMorgan significantly slashed its year-end price target for these two names. The investment firm's decision stems from concerns over declining demand in the European residential solar market, coupled with persistently low power prices and political uncertainties. These factors collectively contribute to a more conservative outlook for these companies in the near term. Let’s take a closer look at these stocks.

Solar Energy Stock #1: Enphase

With a market cap of about $13.9 billion, California-based Enphase Energy, Inc. (ENPH) designs, develops, manufactures, and sells home energy solutions for the solar photovoltaic (PV) industry. Founded in 2006, Enphase revolutionized the solar industry with its microinverter technology, turning sunlight into a safe, reliable, and scalable energy source.

With approximately 68 million microinverters shipped and 3.5 million systems deployed in over 145 countries, Enphase is at the forefront of the clean energy future, helping millions access affordable, reliable energy while fostering job creation and a carbon-free world.

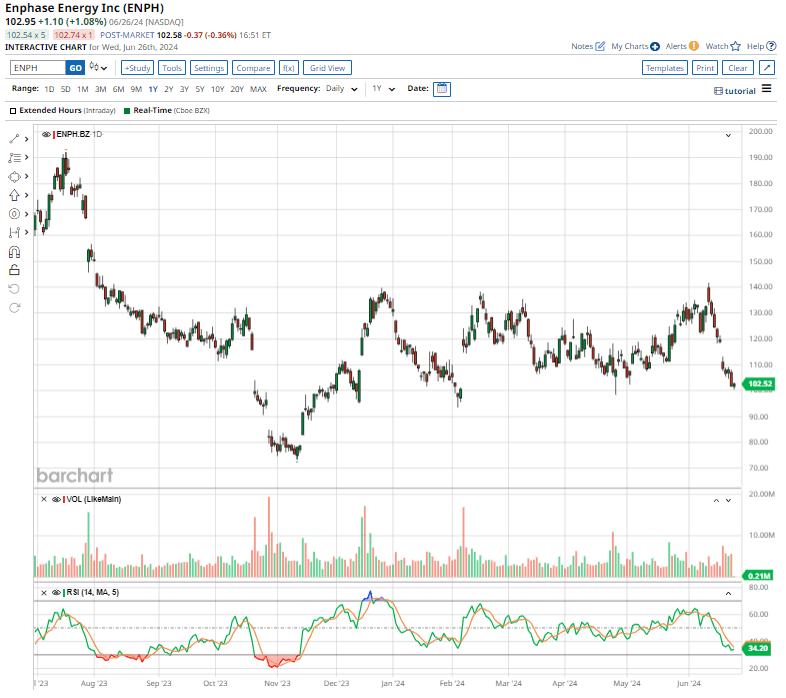

However, shares of this solar equipment company have lagged significantly behind the broader market. Over the past 52 weeks, the stock has plunged nearly 36.1%, compared to the S&P 500 Index’s ($SPX) gain of 26.3% over the same time frame. On a YTD basis, ENPH stock is down 23%, versus the SPX’s return of 14.6%.

From a valuation standpoint, the stock is priced at 70.99 times its forward earnings, trading much higher than its industry peers and its own five-year average.

On April 23, Enphase announced its Q1 earnings results, which failed to meet Wall Street’s forecasts on both the top and bottom lines, triggering a 5.6% drop in its shares in the next trading session. Total revenue for the quarter stood at $263.3 million, marking a 63.7% annual decline, driven by seasonal factors, softened U.S. demand, and strategic inventory management.

On an adjusted basis, the company earned $0.35 per share, down 74% year over year. The company concluded the quarter with approximately $1.6 billion in cash, cash equivalents, and marketable securities while achieving $49.2 million in operational cash flow. Plus, capital expenditures totaled $7.4 million for the quarter, down from $20.1 million in Q4 of fiscal 2023, reflecting reduced spending in U.S. manufacturing.

Looking forward to Q2, management anticipates revenue to range between $290 million and $330 million, while GAAP gross margin is expected to range from 42% to 45%. Additionally, non-GAAP operating expenses are projected to land somewhere between $78 million and $82 million.

Analysts tracking Enphase predict the company’s profit to drop 54.6% year over year to $1.50 per share in fiscal 2024 but rise 136.2% to $3.53 per share in fiscal 2025.

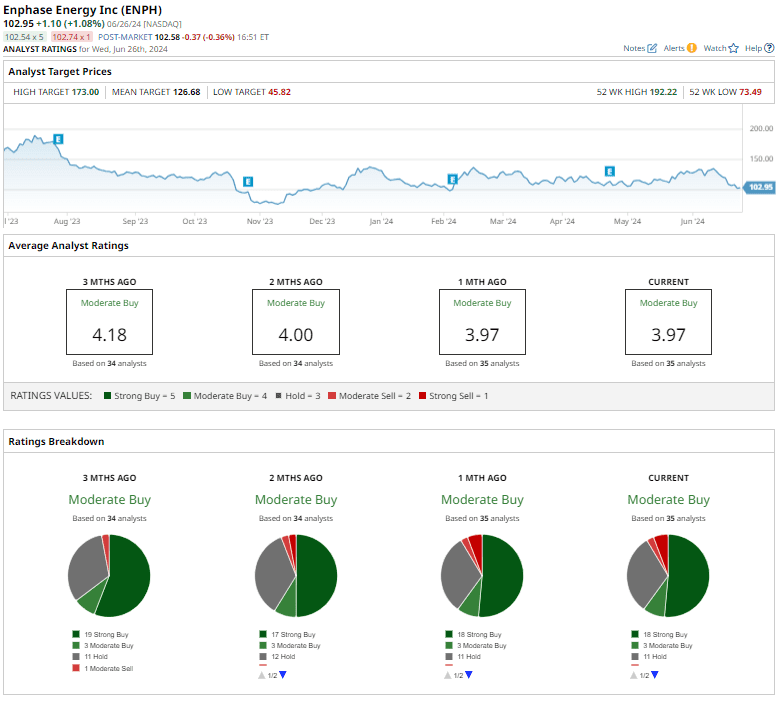

Fueled by the pessimism surrounding European residential solar demand, JPMorgan has lowered Enphase’s price target to $124 from $128. This new target suggests a 21.8% potential upside from current levels.

ENPH stock has a consensus “Moderate Buy” rating overall. Out of the 35 analysts offering recommendations for the stock, 18 recommend a “Strong Buy,” three advise a “Moderate Buy,” 11 suggest a “Hold,” one gives a “Moderate Sell,” and the remaining two give a “Strong Sell” rating.

The average analyst price target of $126.68 indicates a potential upside of 24.2% from the current price levels. The Street-high price target of $173 suggests that the stock could rally as much as 69.6%.

Solar Energy Stock #2: SolarEdge

Founded in 2006, Israel-based SolarEdge Technologies, Inc. (SEDG) revolutionized power harvesting and management in PV systems with its DC-optimized inverter solution, which maximizes power generation and reduces energy costs, enhancing the return on investment for PV systems.

Valued at $1.5 billion by market cap, the company continues to advance smart energy solutions across various market segments with a diversified product offering that includes residential, commercial, and large-scale PV systems, energy storage and backup solutions, electric vehicle (EV) charging, and more.

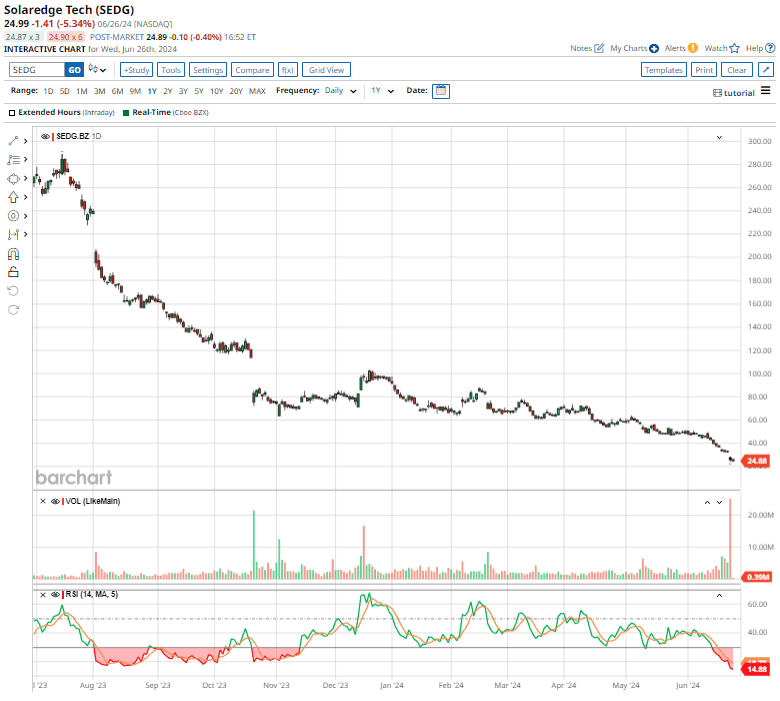

Like Enphase, shares of SolarEdge have nosedived, plummeting nearly 90% over the past 52 weeks and 73.2% on a YTD basis, massively underperforming the broader SPX’s double-digit returns during both these periods.

In terms of valuation, the stock is trading at 0.64 times sales, much lower than its industry peers and its own five-year average.

Following the company’s less-than-stellar Q1 earnings results announced on May 8, the company’s shares tumbled nearly 8.5% in the subsequent trading session. SolarEdge’s revenue of $204.4 million declined a notable 78.4% year over year, but managed to surpass estimates by 4.8%. Its solar segment pulled in $190.1 million in revenue, a staggering 79% plunge from the $908.5 million recorded a year ago.

The company’s non-GAAP loss of $1.90 per share widened by 166.7% from the same period last year, and was steeper than Wall Street estimates. Moreover, as of March 31, SolarEdge’s liquid assets totaled $316.3 million, compared to $634.7 million recorded at the end of fiscal 2023.

Commenting on the Q1 performance, CEO Zvi Lando said, “As we enter spring when installations historically tend to rise, we expect channel inventory to continue to decline and revenues to improve. In parallel, we are focused on a suite of new products that we plan to release in the next several quarters to position ourselves for the next growth cycle in our industry.”

For Q2, management anticipates revenue to range between $250 million and $280 million, while revenue from the solar segment is projected to fall within the range of $225 million and $255 million. Also, non-GAAP operating expenses are forecasted to arrive somewhere between $116 million and $120 million.

Analysts tracking SolarEdge predict the company’s loss to widen sharply to $6.12 per share in fiscal 2024 before swinging to a profit of $0.43 per share in fiscal 2025.

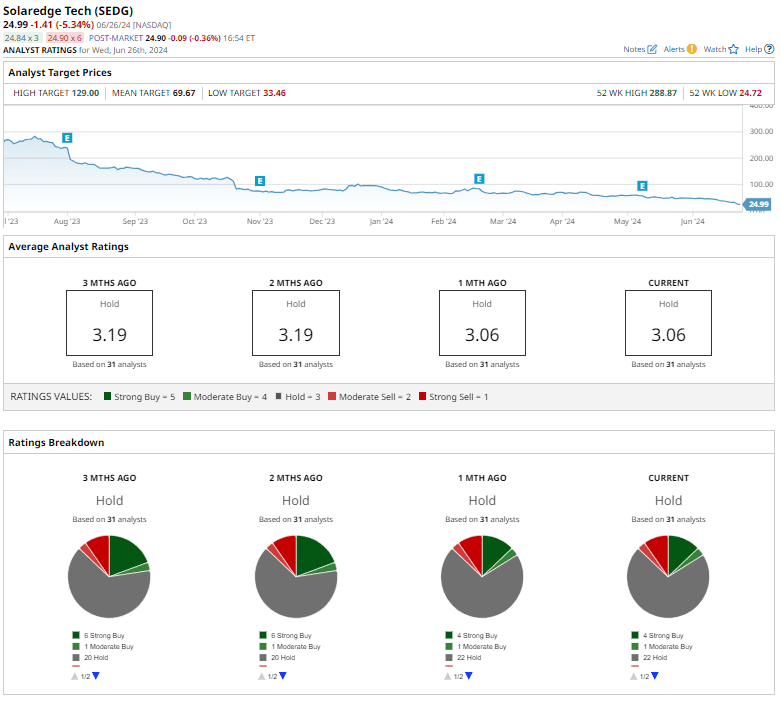

JPMorgan has lowered SolarEdge’s price target to $59 from $73, which still implies an ambitious 134% potential upside from its current levels.

SEDG stock has a consensus “Hold” rating overall. Out of the 31 analysts covering the stock, four recommend a “Strong Buy,” one suggests a “Moderate Buy,” 22 recommend “Hold,” one advises a “Moderate Sell,” and the remaining three give a “Strong Sell” rating.

The average analyst price target of $69.67 indicates a potential upside of 177.3% from the current price levels, while the Street-high target of $129 implies an impressive 413% upside potential.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.