Praetorian Capital commentary for the fourth quarter ended December 31, 2021.

Q4 2021 hedge fund letters, conferences and more

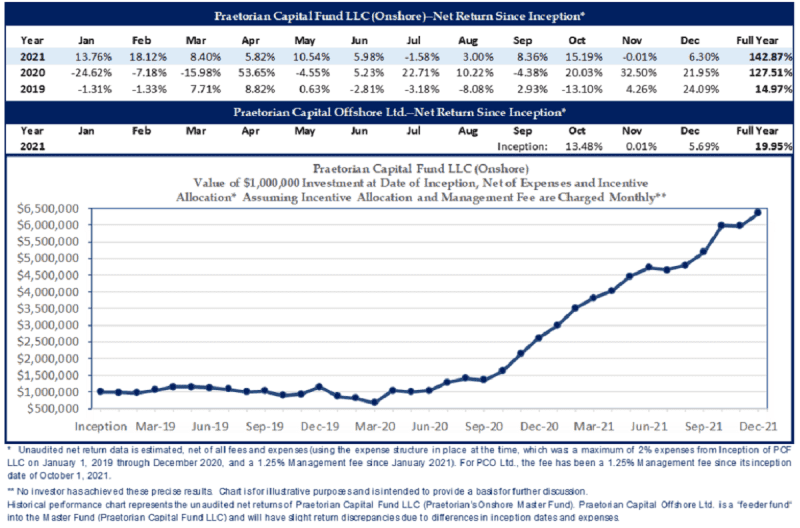

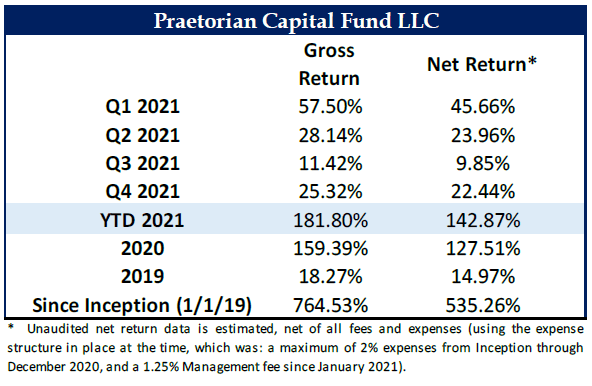

During the fourth quarter of 2021, the fund appreciated by 22.44% net of fees. For 2021, the fund appreciated by 142.87% net of fees. Given the fund’s concentrated portfolio structure and focus on asymmetric opportunities, I anticipate that the fund will be rather volatile from quarter to quarter. During the fourth quarter, our core portfolio appreciated moderately. Meanwhile, our Event-Driven Book produced a moderately positive return excluding one opportunity that added approximately 900 basis points during October. This subpar return from the Event-Driven book is mostly a reflection of a slow fourth quarter in terms of events and reduced overall market volatility. I am hopeful that recent increases in market volatility during early January of 2022 will lead to a recovery in our Event-Driven performance in future periods.

The fourth quarter of 2021 marks a notable milestone for our fund as the fund is now three years old. I have always believed that rolling three-year periods are the shortest duration necessary to judge the performance of an investing strategy. I’m proud to say that during the first three years in existence, this fund has produced a return of 535.26% net of fees. This works out to a compound annual return of 85.20% net of fees. While past returns are clearly not indicative of future performance, I believe that our three-year performance is indicative that the strategy is compounding capital at an attractive rate for investors.

I would like to caution you that our portfolio has become somewhat lopsided in terms of being exposed to inflation assets, particularly with a focus on energy assets. Partly, this is due to disproportionate appreciation of those assets as a percentage of the portfolio and partly this is a result of what I see as the most attractive opportunity set in the current market. As commodities tend to be more volatile than the overall market, it bears mentioning that this increased exposure is likely to increase the overall volatility of our fund.

Market View

Looking out into 2022, I see an economy with accelerating rates of inflation, mostly driven by commodity and labor inflation. While the Federal Reserve will continue to talk tough, it will fail to rein in this inflation. Instead, the Fed will likely remain behind the curve in terms of taming this inflation but will succeed in detonating the bubbles in the Ponzi Sector along with high multiple tech. Additionally, I believe that many of the set-it-and-forget-it “compounder” companies will see margin and ultimately multiple compression as the Fed engages in Quantitative Tightening along with interest rate increases. Consequently, the capital in this sector will likely gravitate to the “Old Economy” value names that I have spent much of my career analyzing.

This sector rotation began during the summer of 2021 and has been accelerating ever since. While it has led to some volatility, I think the real fireworks are just beginning. Fortunately, we have taken down our overall exposure and I believe that our portfolio is well-positioned for inflows into undervalued securities that are tied to increasing rates of inflation.

Activism

During the fourth quarter, this fund engaged in shareholder activism. While I’d prefer to avoid the distractions of activism, I refuse to let us be a victim. The case in question involved our filing a 13D in relation to an unsolicited take-over proposal for Lee Enterprises, Incorporated (NASDAQ:LEE) at $24. I believed that the offer was woefully inadequate and made my point known to LEE’s Board of Directors. Fortunately, the Board proceeded to reject the offer the following day. In the five trading days after we filed our 13D, the shares appreciated as high as $41, showing that other market participants agreed with me that $24 was inadequate. Once again, I don’t intend for this fund to go looking for fights, but I don’t intend to get abused either. As the fund gets larger, we will inevitably give up some of our edge in terms of liquidity; hopefully we’ll more than offset that by our ability to have our voice heard when necessary.

Position Review (top 5 position weightings at quarter end from largest to smallest)

Uranium Basket (Entities holding physical uranium along with production and exploration companies)

It may take some time still, but I believe that society will eventually settle on nuclear power as a compromise solution for baseload power generation. In my opinion, this will come at a time when there is a deficit of uranium production, compared with growing demand. As aboveground stocks are consumed, uranium prices should appreciate towards the marginal cost of production. Additionally, there is currently an entity named Sprott Physical Uranium Trust (U-U – Canada) that is aggressively issuing shares through an At-The-Market offering or ATM to purchase uranium (we are long this entity). I believe that these uranium purchases will accelerate the price realization function by sequestering much of the available above-ground stockpile at a time when utilities have run down their inventories and need substantial purchases to re-stock. The combination of these factors ought to lead to a dramatic increase in the price of uranium as it will take roughly two years for any incremental supply to come online—even if the re-start decision were made today.

While most of our exposure is to physical uranium within the Sprott trust, as it allows us to express this view with reduced risk, we also own shares of Kazatomprom (KAP – UK) along with a few select junior miners. I am well aware that mining is one of the riskiest businesses out there, but Kazatomprom is the lowest-cost producer globally, with incredible scale in what is a highly consolidated industry. At the same time, I recognize that we take on certain risks when owning a company engaged in mineral extraction, especially in a country like Kazakhstan that can be politically unstable at times. That said, I believe that the recent change in government will do little to impact the operating environment in Kazakhstan, though the tax rate may expand moderately.

Newspaper Securities Basket (LEE Along with Other Positions Not Currently Disclosed)

Most global print newspapers have seen their readership decline for decades as subscribers seek out alternative digital sources of information. In response to this, newspapers have tried to build up their digital presence. Historically, this digital revenue stream was always rather negligible as it was coming from a small base, especially when compared to steep declines from the print side.

Over the past few years, digital revenue growth has accelerated to the point where I expect that the newspaper companies in our basket are within a few years of their digital revenue overtaking their print revenue—assuming recent trends hold. Digital revenue represents a higher margin and higher return on capital business when compared to the capital and manpower intensity of printing and distributing physical newspapers. My belief is that, as these digital businesses come to dominate the revenue stream, newspaper company valuations will re-rate—particularly as many of them trade as if they are dying businesses, when in reality, the digital side of their businesses is growing quite rapidly.

While many well-known global newspapers have successfully made this digital transition and seen earnings growth for a number of years, many smaller papers have continued to see earnings decline. I believe that these smaller papers are now on the cusp of an inflection to earnings growth as digital growth overtakes print declines. Should this happen, I anticipate it will dramatically change the narratives for these companies, along with their valuations, much like what occurred at more well-known papers. The fund owns a global basket of these smaller newspaper companies.

Looking at Lee Enterprises, Incorporated (NASDAQ:LEE), which is our largest position in this basket; during the most recent reported quarter, LEE saw 65% annual growth in digital subscribers. Additionally digital revenue now represents approximately 34% of total revenue. Both of these metrics are rapidly growing. I have every reason to believe that this growth will continue in future periods.

St. Joe (JOE – USA)

St Joe Co (NYSE:JOE) owns approximately 175,000 acres in the Florida Panhandle. It has been widely known that JOE traded for a tiny fraction of its liquidation value for years, but without a catalyst, it was always perceived to be “dead money.”

Over the past few years, the population of the Panhandle has hit a critical mass where the Panhandle now has a center of gravity that is attracting people who want to live in one of the prettiest places in the country, with zero state income taxes and few of the problems of large cities.

The oddity of the current disdain for so-called “value investments” is that many of them are growing quite fast. I believe that JOE will grow revenue at 30% to 50% each year for the foreseeable future, with earnings growing at a much faster clip. Meanwhile, I believe the shares trade at a single-digit multiple on Adjusted Funds from Operations (AFFO) looking out to 2024, while substantial asset value is tossed in for free.

Besides the valuation, growth, and high Return on Invested Capital (ROIC) of the business, why else do I like JOE? For starters, land tends to appreciate rapidly during periods of high inflation—particularly an inflationary period where interest rates are suppressed by the Federal Reserve. More importantly, I believe we are about to witness a massive population migration as people with means choose to flee big cities for somewhere peaceful.

I suspect that every convulsion of urban chaos and/or tax-the-rich scheming will launch JOE shares higher, and it will ultimately be seen as the way to “play” the stream of very wealthy refugees fleeing for somewhere better.

Energy Services Basket (Positions Not Currently Disclosed)

In 2020 when oil traded below zero, drilling activity ground to a halt and many energy service providers declared bankruptcy. Many of these businesses had teetered on the verge of bankruptcy for years due to reduced demand and over-leveraged balance sheets. The bankruptcies led to consolidation and reduced future industry capacity, removing future competition in the recovery.

With oil prices now at multi-year highs, I believe that demand for drilling and other services will recover. We purchased many of these positions at fractions of the equipment’s replacement cost, despite restored balance sheets and positive operating cash flow. As the sector recovers, I believe that this cash flow will become more apparent, and this equipment will trade up to valuations closer to replacement cost.

Long-Dated Oil Futures and Futures Options (Various Strikes and Maturities)

I believe that many years of reduced capital expenditures in the oil sector, combined with continued increases in global consumption, ought to lead to higher oil prices. We are expressing part of this bullish oil view by directly owning December 2025 oil futures, which trade at a substantial discount to front-month pricing. I believe that these futures will eventually reflect anticipated inflationary cost pressures and trade higher. Additionally, we own a sizable position in various longer-dated oil futures options as they give us additional upside leverage to this thesis, but with a defined risk profile should I be incorrect in my analysis. Given the long-dated nature of these futures options, the premiums should only decline gradually, giving us plenty of flexibility to re-evaluate this position over time, with minimal price risk.

In summary, during the fourth quarter of 2021, the fund experienced a positive net return on our capital, despite a rather subdued return from our Event-Driven book. Our exposure is a bit more concentrated in inflation, particularly in energy, than I’d normally expect it to be, but those are also my favorite themes. I also believe we’ve expressed this view through instruments like physical uranium, long dated oil futures and futures options, energy equipment services companies and land plays, which should have a reduced risk of permanent impairment.

Given our moderate overall leverage, I’m actively looking for additional themes to add to our stable of positions while cognizant that accelerating inflation may create additional volatility.

Operational Updates

As this fund matures, we have been active on the operational side. During the third quarter, I was remiss in not mentioning some of these changes. In January of 2021, I legally moved to Puerto Rico and my homebase is now in Rincon, on the west coast of the island. I moved there with good friends Nick and Lauren Cousyn, who will take over roles in client relations and operations, respectively. If you haven’t yet spoken with Nick, please reach out and introduce yourself (Nick@Pracap.com). Lauren will be your contact if you want to add funds in the future (Lauren@pracap.com). Continuing on the staffing side, I’m looking to add two analysts during the first half of 2022 as I look to beef up our research capabilities. If you know of anyone who would like to apply for the two research analyst roles based in Rincon, Puerto Rico, please have them apply to: Jr. Research Analyst - Open positions. I will not consider remote employees.

In early January of 2022, the fund’s assets surpassed $100 million. I’m highly cognizant of the fact that as our assets grow, our ability to be nimble will slowly recede. As a result, I intend to closely monitor the fund’s asset level and will likely close the fund to new investors sometime in 2022 (assuming that inflows remain at the current pace). Additionally, for the onshore fund, we are increasing our investment minimum to $5 million as we are only allowed to have 99 investors and have less than 10 “slots” remaining. The offshore fund’s minimum investment will remain at $250,000 for now, but will likely increase in the next few months. Existing investors can still add to their capital accounts and these changes will not impact existing investors. I want you to know that my focus remains on producing strong performance results—not on asset aggregation. I hope that you see these changes as evidence of that.

I want to finish by thanking all of you for entrusting your capital with me. It’s a great honor and responsibility. I’m proud of the results that I have been able to produce in this fund’s first three years and am hopeful that results in future years will continue to be strong.

Sincerely,

Harris Kupperman

Praetorian Capital Management LLC

Updated on