S&P 500 was indeed building a bull flag, which “must” now continue with a fresh upleg so that the formation is validated. Odds are that in spite of the tech-led upswing, the rally would continue. All that‘s required for today, is a not too disappointing non-farm payrolls figure, which would (in the market‘s mind) give the Fed some leevay in taking on inflation while not choking off economic growth (however decelerating). Optimal outcome would be a figure somewhat below expectations as that would enable speculation as to how far the Fed would move towards focus on growth (the Brainard view of things) and away from Powell‘s resolute (verbally resolute, to be precise – big difference) inflation fighter pose. Yesterday‘s Yellen admission on getting it wrong, is a preview of more hawkish monetary policies still ahead.

Q1 2022 hedge fund letters, conferences and more

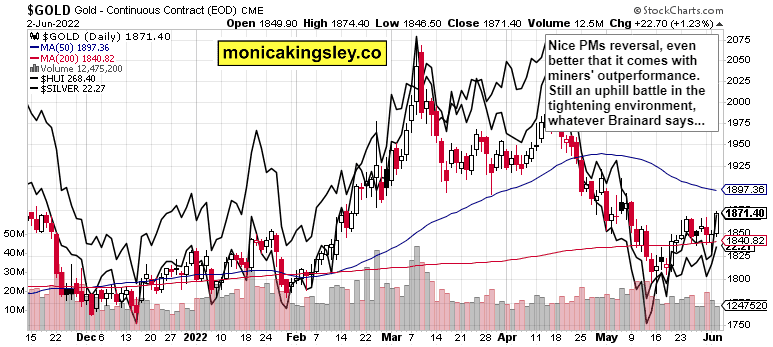

That‘s why I‘ve said that this rally wasn‘t sustainable, but it still has further to go. Treasuries aren‘t relenting in the pressure on the Fed to act, and the central bank would have to catch up. It‘s a question of time when this risk-on reprieve runs its course. Yesterday‘s turn in precious metals and copper is a preview of what such a Fed turn would imemdiately cause – helping the open positions mightily. And I‘m not even talking the sizable open profits in crude oil...

S&P 500 and Nasdaq Outlook

Not too much dillydallying now is key for stocks. We can go higher still – value hasn‘t yet kicked in properly, there is still time for this rotation. How soon would that come? The bulls don‘t have the luxury of time.

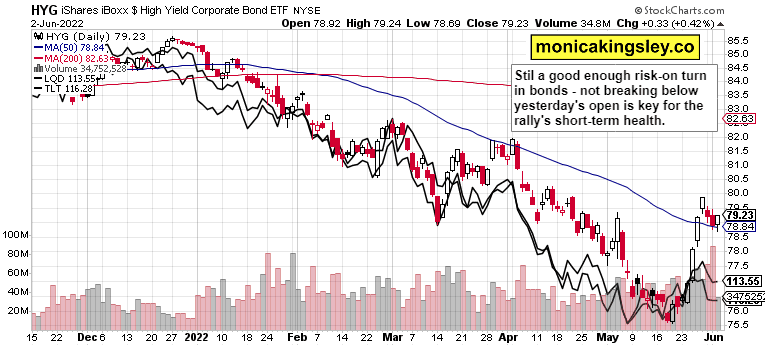

Credit Markets

HYG reversal would look better if it happened on higher volume. Still, that can (and probably would) be overcome. What‘s key here is that Wednesday‘s downswing was heavily bought, and the bears couldn‘t push prices lower yesterday.

Gold, Silver and Miners

Precious metals are turning up, and one dovish remark appropriately interpreted, does that trick. It‘s encouraging that the Yellen appearance was ignored by real assets – let‘s not get into overly celebrating mood as the weeks ahead aren‘t about to bring stellar gains in the least, not yet.

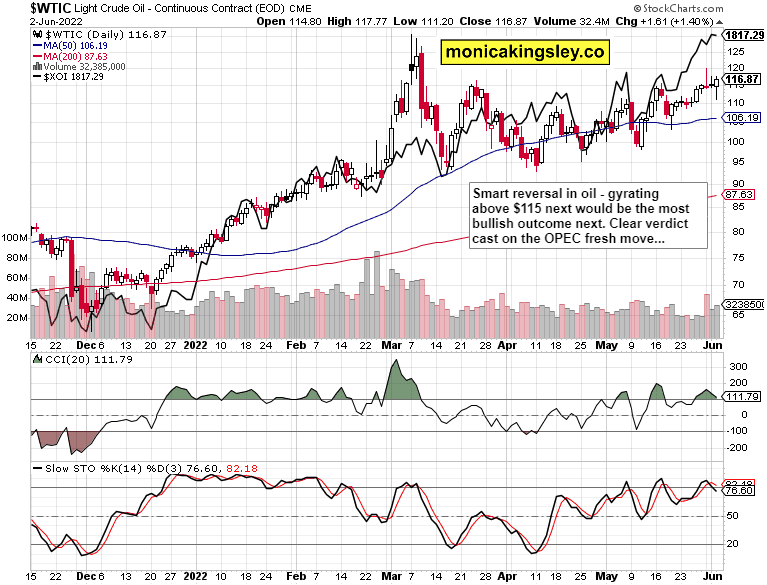

Crude Oil

Crude oil bulls have stepped in, and the fact it happened on OPEC production increase news, is encouraging. Sideways, running correction in a tight range – that would be an optimal outcome for the bulls. Still time to keep holding crude.

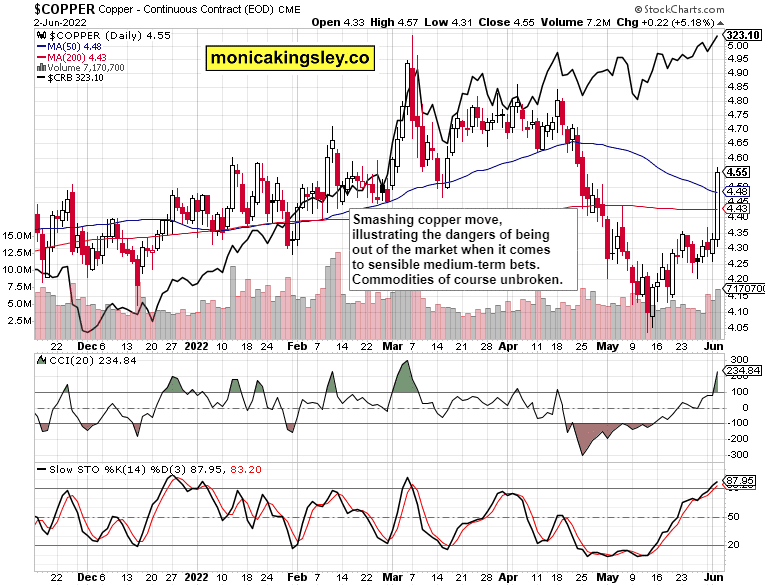

Copper

Copper surprised in a good way – keeping above $4.50 roughly so that the daily momentum can continue for a little longer, would be great. Foot off the tightening pedal reflected in bond yields and the dollar (both down), would facilitate that in an instant.

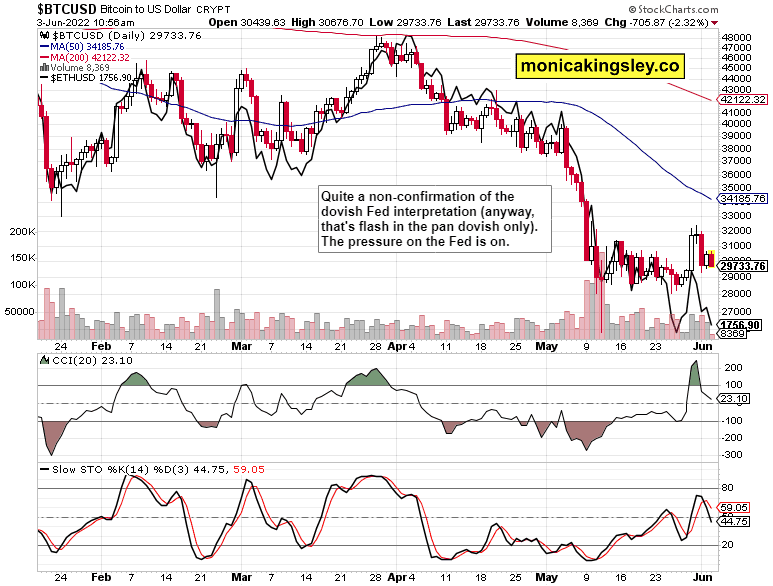

Bitcoin and Ethereum

Warning message from the cryptos after all – even when the dollar declines. Daily shows of remarkable strength look best to be sold.

Summary

S&P 500 can still continue its upswing but the 4,115 area better hold in the non-farm payrolls aftermath. Odds are good that any panic selling in the wake of a number coming in below expectations, would be reversed. And that could help real assets as well to extend gains – even if in a more modest way than was the case yesterday. What magic can bringing up the growth focus card by Brainard do… Treasuries though aren‘t buying the dovish turn, so get ready for rough trading in the weeks and short months ahead – all we got yesterday, was a preview of what the reaction to the Fed pivot, would be.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the five publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals, Copper Trading Signals and Bitcoin Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

Oil Trading Signals

Copper Trading Signals

Bitcoin Trading Signals

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.

Updated on