By Darren Parkin

Volatility was rife in the cryptocurrency markets last week as Bitcoin and other popular digital assets continued to decline. Data from CryptoCompare shows that Bitcoin opened the week just above the $24,000 mark, however, by the time the week concluded, it had settled below $21,000 – roughly a 12.5% decline.

The native token of the Ethereum network, Ether, the second largest cryptocurrency by market capitalisation, experienced a similar fate, declining from $1,900 to end the week just above the $1,550 level.

Despite the recent price action, August has been an exciting month for those who follow the developments of the Ethereum network. Earlier this month, Ether saw its price soar above $2,000 as market participants speculated on the narratives surrounding the approaching Merge upgrade, which is now predicted to take place on September 15. This is an event that many consider pivotal within the space, for not only does this reduce Ethereum’s energy consumption by over 99%, but it also lays the foundations for future scalability upgrades such as sharding.

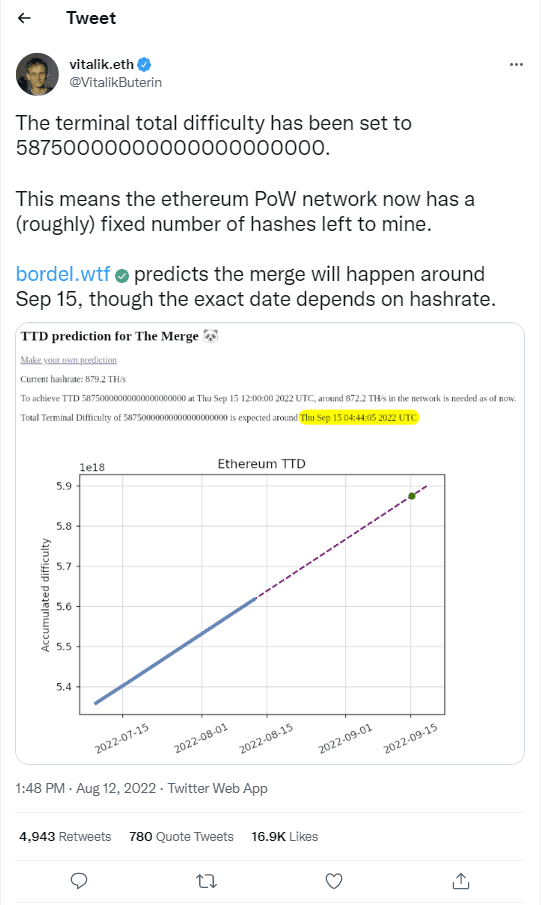

Historically, the Ethereum foundation has received criticism for the setbacks surrounding the Merge date, which has been delayed numerous times. However, this time, things look to be different. The Ethereum network successfully merged on its Goerli testnet, and Ethereum creator Vitalik Buterin announced via Twitter that the terminal total difficulty (TTD) has been set to 58750000000000000000000.

TTD refers to the total difficulty required for the final block of the Proof of Work Ethereum network to be mined; essentially this helps to predict when the Merge will take place based on the network hash rate.

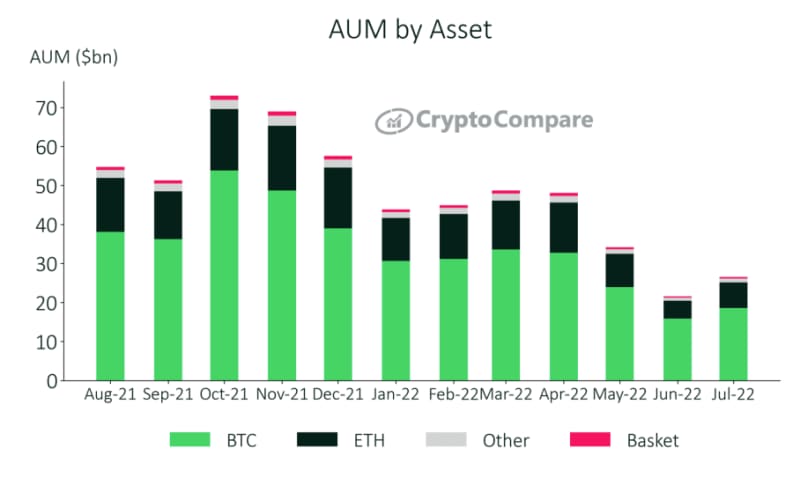

The promising developments surrounding the Merge have also been reflected in market activity. Ethereum Open Interest outpaced Bitcoin’s for the first time ever at the start of August, and Ethereum-based cryptocurrency investment products also saw a resurgence, with their AUM rising 44.6% to $6.57 billion, according to CryptoCompare’s latest Digital Asset Management Review.

Stablecoins, depegs, regulation, and legislation

Moving away from the Merge, more news has surfaced surrounding another leading narrative within the crypto markets: stablecoins. A proposed bill, which is scheduled to be debated in Parliament in September, could bring stablecoins into the scope of local payment regulation within the UK.

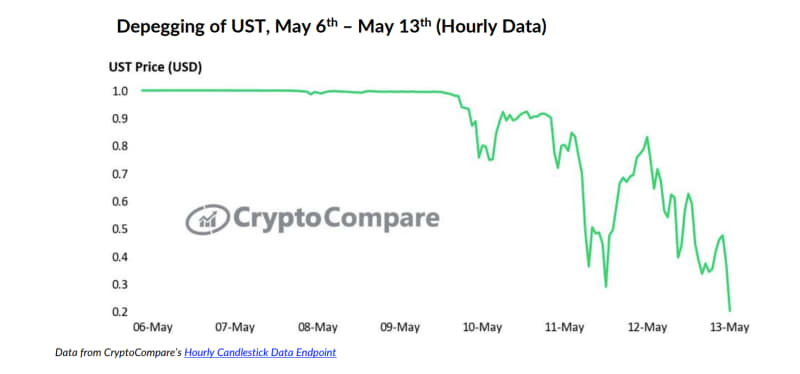

It is no surprise that a bill of this type is being introduced following the downfall of the terraUSD (UST) algorithmic stablecoin, which lost its peg against the dollar and proceeded to collapse, wiping out a $40bn ecosystem in the process. Many governments have started to put together new legislation surrounding stablecoins in the wake of the collapse; this includes the UK, the U.S., and Singapore to name a few.

The bill has seen a largely positive reaction from many U.K.-based crypto advocates, however, it is unclear what the new rules will ascertain if the bill were to pass. Regardless, increased legislation and regulation surrounding stablecoins seems almost certain at this point, as the depeg of UST has not been an isolated incident.

HuobiUSD (HUSD) and Acala Dollar are the latest stablecoins to fall from their peg. Last Thursday, HUSD began to decline from its $1 value, falling to as low as $0.82 as a result of liquidity issues. In response, Huobi announced they had been in contact with the HUSD stablecoin issuer Stable Universal Limited. The peg of HUSD was restored to $1 by the following day.

Elsewhere, however, users were not so fortunate. Acala Dollar (aUSD) fell victim to an exploit that saw a user mint 1 billion aUSD, which caused the stablecoin to depeg by 99%. In response, the Acala team froze the hacker’s wallet and were eventually able to cover a large portion of the tokens. The team’s actions, however, raised numerous questions over the platform’s claims of decentralisation.

Coinbase insider trading may spread wider than US

In other news, it has surfaced that the US charge against a former Coinbase employee may not have been the only instance of insider trading happening at the popular cryptocurrency exchange, according to a new study by researchers from the University of Technology Sydney (UTS).

Ishan Wahi, 32, who is a former Coinbase product manager, was arrested on charges that he had shared confidential information with his brother about the new assets that were being listed on Coinbase.

Researchers from UTS examined how tokens traded on decentralised exchanges (such as Uniswap) prior to Coinbase’s listing announcement. The research showed that some traders appeared to take advantage of the popular DEX to buy tokens of 10-25% of all Coinbase listings since 2018.

Furthermore, they uncovered that on average the price of the newly-added token jumped 40% compared to a market benchmark during the 300 hours preceding the Coinbase listing announcement. Following the announcement, the price would rise another 2% over the subsequent 100 hours, the study found.

Jamie Sly is a content creator at CryptoCompare who holds various cryptocurrencies.

The post Merge approaches amid more stablecoin woes appeared first on CityAM.