- Pepsico pays a market-beating dividend and provides some safety from broad-market volatility.

- The company beat its Q3 consensus expectation and guided the market higher.

- Long-term trends suggest growth, capital returns, and dividend growth will continue in calendar 2023.

Pepsico (NASDAQ:PEP) has been lagging behind the broad market since the pandemic bottom but that may be about to change. The company’s performance may be tied to its high valuation, it trades near 24X earnings, but the valuation is well earned and the stock has many attractive qualities for investors.

Q3 2022 hedge fund letters, conferences and more

Find A Qualified Financial Advisor

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

If you're ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Not only does it pay a market-beating 2.80% dividend yield that comes with a highly-favorable outlook for dividend growth but the company is growing on an organic basis, outperforming its consensus expectations, and offers some safety in a time of market madness.

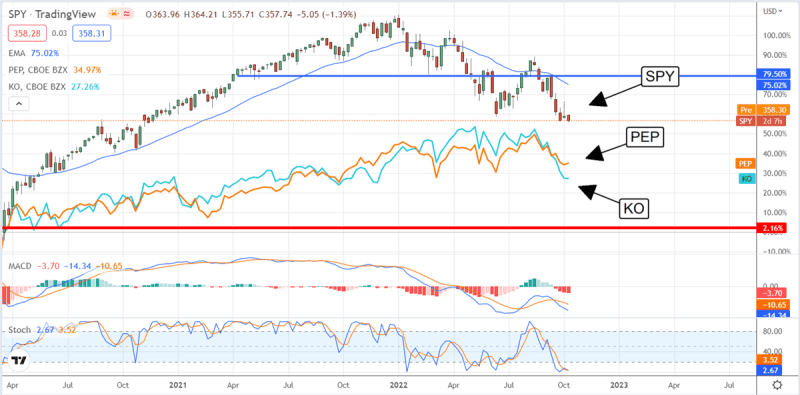

Pepsico is running with a beta of only 0.57 which makes it about half as volatile as the broad market and volatility in the broad market is on the rise.

Pepsico’s beta is also lower than the broader Consumer Staples sector (NYSEARCA: XLP) which makes it a better choice than an index-tracking ETF. The takeaway is that Pepsico is a winning dividend-growth stock in a winning sector with some insulation from the market downturn.

“Our strong results demonstrate that the investments we have made towards becoming an even Faster, even Stronger, and even Better company with pep+ at the center of everything we do are working. We are encouraged by the progress we are making on our strategic agenda, and remain committed to investing in our people, brands, supply chain, and go-to-market systems and winning in the marketplace.”

Pepsico Is Well-Supported By The Sell-Side Market

Pepsico appears to be well-supported by the market due to positive trends in both the analyst's sentiment and the institutional activity. There were a few price target reductions in the weeks ahead of the FQ3 earnings report but that should change now the report is in.

Until then, the Marketbeat.com consensus rating is a Moderate Buy with a price target of $184.50 and both are trending higher in the 12, 3, and 1-month comparisons.

As for the Q3 results, they are in line with the long-term investment thesis which is one of organic growth, capital appreciation, and capital returns. The company reported $21.97 billion in net revenue for a gain of 8.8% over last year that beat the consensus estimate by 550 basis points.

The strength was driven by growth in all segments led by Quaker, Frito Lay NA, and Latin America and this is despite a 300 basis point FX-related headwind. On an organic basis, sales are up 16% and accompanied by stronger margins as well.

In regard to the earnings and outlook, the company reported a 22% increase in GAAP earnings and a 14% increase in adjusted earnings that were driven by top-line strength, internal efficiency, and share repurchases which are expected to continue into the current quarter and next year.

The guidance reflects the Q3 strength, up 2% on the top line with core EPS of $6.73 versus $6.63 prior, and there is room for an upside surprise. Assuming the company’s momentum carries into the 4th quarter sales could easily outpace consensus and set it up fro strength in 2023 as well.

Pepsico On Track For Capital Returns

Pepsico reiterated its guidance for capital returns in F22 which has it on track to raise the dividend next summer. The company says it will pay $7.7 billion in dividends and repurchases and has $344 million or about 0.15% of the market cap left for the fiscal year.

The dividend is safe as well, the payout ratio is a bit high at 67% but it is still within acceptable limits for a Dividend King. Competitor The Coca-Cola Company (NYSE: KO) pays a higher yield but also has a higher payout ratio and lower distribution CAGR.

The Coca-Cola Company is also running with an identical 0.57 5-year monthly beta but is obviously more volatile than Pepsico in the post-pandemic world.

Should you invest $1,000 in PepsiCo right now?

Before you consider PepsiCo, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and PepsiCo wasn't on the list.

While PepsiCo currently has a "Moderate Buy" rating among analysts, top-rated analysts believe these five stocks are better buys.

Article by Thomas Hughes, MarketBeat