By Darren Parkin

Data from CryptoCompare shows that the price of Bitcoin endured a steep sell-off over the past week, dropping from around $19,600 to an $18,800 low before it started to recover.

Ethereum’s Ether, the second-largest cryptocurrency by market cap, traded in a way similar to BTC, dropping from $1,320 t a $1,260 low before recovering.

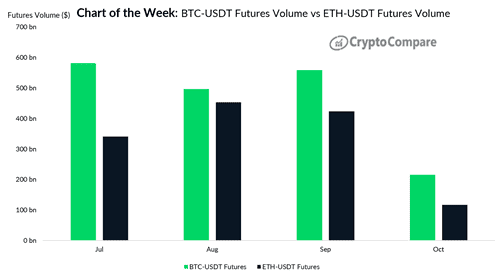

Data from CryptoCompare has found that leading up to the Ethereum Merge upgrade there was a rise in speculative activity on Ethereum, with the ratio of ETH-USDT and BTC-USDT futures volume reaching 0.91 in August.

However, liquidity returned to Bitcoin soon after the merge, with BTC futures seeing an 83.7% greater volume than ETH futures in October, as of the 16th.

Headlines in the cryptocurrency space this week were marked by an announcement from Mastercard, which detailed the firm was launching a new program enabling financial institutions to bring secure cryptocurrency trading capabilities and services to their customers, called Crypto Source. The company will act as a bridge between Paxos and banks through it.

Mastercard and Paxos will handle regulatory compliance and security as part of the program to allow financial institutions to “gain access to a comprehensive suite of buy, hold and sell services for select crypto assets, augmented with proven identity, cyber, security and advisory services.”

While Paxos is set to provide cryptocurrency trading and custody services on behalf of banks, Mastercard’s technology will “integrate those capabilities into banks’ interfaces” to improve user experience.

Mastercard’s move comes during the same week in which Fidelity Digital Assets, an independent subsidiary of financial services giant Fidelity Investments, announced it will start offering institutional clients the ability to trade Ether (ETH) on October 28.

Similarly, financial services giant Plaid has announced the launch of its first cryptocurrency-native product Wallet Onboard, which helps developers connect cryptocurrency wallets such as MetaMask to decentralised applications.

The product allows users to connect wallets such as MetaMask or Coinbase Wallet to apps, via a Plaid-branded interface as part of the onboarding process. Each onboarded wallet goes through Plaid’s compliance review, which to the firm means it can bolster security and trust in the ecosystem.

Moreover, this week Nubank, Brazil’s largest digital bank, revealed it’s set to launch its own cryptocurrency in the country next year as it moves deeper into the cryptocurrency space. The cryptocurrency, Nucoin, was deemed a “new way to recognise customer loyalty and encourage engagement with Nubank products.” The firm plans to offer discounts and other perks to token holders.

Leading stablecoin issuer Tether is also making moves in Brazil, as through a partnership with local payment solution startup SmartPay, its USDT stablecoin is set to become available at more than 24,000 ATMs in the country.

In Brazil, Tether’s USDT stablecoin will become available at local anco24Horas ATM machines, allowing users to convert USDT into Brazilian reais. Banco24Horas ATMs are common throughout the country and are located in high-traffic areas.

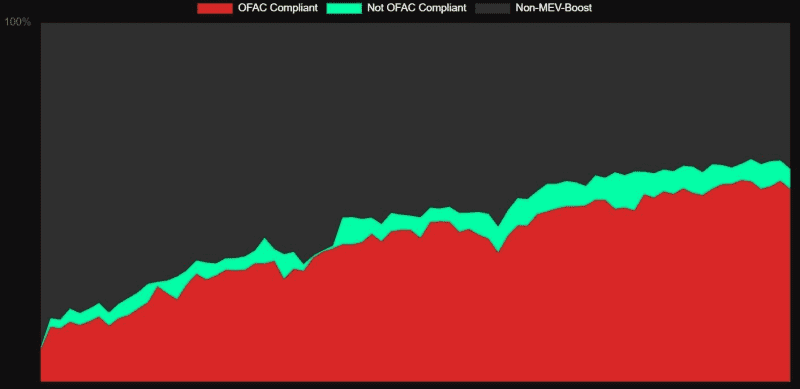

54% of Ethereum blocks are complying with US sanctions

Over the week, the percentage of newly found blocks on the Ethereum blockchain that are now following the US Treasury Department’s Office of Foreign Assets Control (OFAC) compliance recommendations rose to 54%. This means they are actively censoring transactions associated with the mixing service Tornado Cash.

These blocks are being delivered by relays that screen out transactions associated with the mixing service to comply with OFAC after it banned Americans from using Tornado Cash. Network validators use maximal extractable value (MEV) services to reorder transactions with a block to boost rewards.

Flashbots, an Ethereum-based research and development group, has been working on ways to curb the potential harms of MEV by building software that allows validators to request blocks from a network of builders via a middleman, called a relay. The most popular relay is one built by Flashbots.

Flashbots’ relay refuses to pass blocks containing transactions from sanctioned addresses, and out of five MEV-boosting relay providers, only two are offering non-censoring options.

This growing compliance comes as 2022 is on track to be crypto’s “biggest year for hacking on record,” as in October alone, more than $700 million were stolen from decentralised finance protocols.

According to Chainalysis, so far this year, hackers have “grossed more than $3 billion across 125 hacks”.

Despite these security breaches, developments in the cryptocurrency space keep growing. The XRP Ledger, the native network of the XRP token, has started testing a sidechain compatible with the Ethereum Virtual Machine (EVM) in a bid to bring smart contracts to its network. The sidechain has been developed by a firm called Peersyst and is in its first phase of development.

Ethereum itself has launched the “Shandong” testnet, where developers can start testing out their next upgrades to the protocol. The testnet is for the Shanghai upgrade, which is projected to happen next year.

Francisco Memoria is a content creator at CryptoCompare who’s in love with technology and focuses on helping people see the value digital currencies have. His work has been published in numerous reputable industry publications. Francisco holds various cryptocurrencies.

Featured image via Unsplash.

The post Mastercard to help banks offer crypto trading as Ethereum blocks compliance grows appeared first on CityAM.