By Darren Parkin

Data from CryptoCompare shows that the price of Bitcoin dropped over the week to go from around $23,000 to a $21,600 low where it’s currently trading. The cryptocurrency industry has faced several negative headlines over the past few days.

Ethereum’s Ether – the second-largest cryptocurrency by market cap – moved similarly to BTC, starting the week with a move up to $1,650 before starting to drop, to now trade below the $1,500 mark.

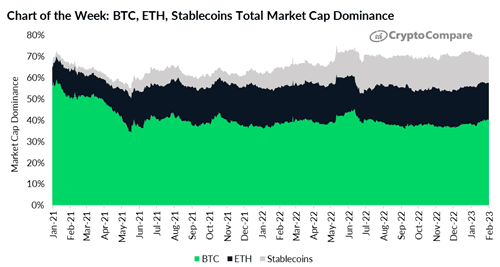

Notably, CryptoCompare data has shown that there was a 2.7% drop in the combined market cap dominance of BTC, ETH, and stablecoins, now making up 69.8% of the total cryptocurrency market cap.

The drop in dominance signals a change in market sentiment among market players, being the largest month-to-month decrease since August of 2021. The drop is mainly caused by a decrease in stablecoins’ market share, which has gone from 16.6% at the beginning of the year to 12.3% by the end of January.

Over the past week, various players in the cryptocurrency industry have offered assistance to Turkey following devastating earthquakes and aftershocks that have claimed over 30,000 lives and are projected to exceed 50,000, while destroying parts of some cities.

READ MORE: Binance to airdrop BNB tokens to users in Turkey earthquake region

In the wake of the earthquakes, several exchanges, including Binance, BitMEX, and Bybit, announced their plans to provide aid in the near future. Cryptocurrency exchange BitGet has already pledged one million Turkish Lira ($53,000) in aid, and Huobi Global has promised two million Lira.

The crypto community has a history of quickly responding to humanitarian crises, with millions of dollars being donated to Ukraine after Russia’s invasion last year, and to India during its deadly COVID-19 outbreak two years ago.

A group of more than 40 blockchain industry and research organisations in Turkey have signed a petition calling on the authorities to allow crypto-based donations. The petitioners want the creation of “official crypto asset wallets” and for them to be distributed through official channels, similar to what was done in Ukraine after the war started in February 2022, to prevent “malicious aid schemes”.

Binance stood out in the way it sent aid, as it moved to airdrop $100 in BNB to all of its users identified to be living in the regions affected by the earthquakes. The exchange estimated it would be donating around $5 million to affected users, worth around 94 million Turkish Lira. It noted that cryptocurrency transfers are “now increasingly being used to deliver financial aid to disaster victims”, as they provide fast and cheap borderless transactions.

Kraken to shut crypto staking service in $30 million SEC settlement

While the crypto industry rallied in support of Turkey, in the United States, crypto exchange Kraken agreed to pay a $30 million settlement to the Securities and Exchange Commission (SEC) for alleged violations of the agency’s rules regarding its staking products. As a result, the firm will shut down its staking service for US clients.

A representative from Kraken clarified that only US clients will be impacted, and their assets will be ‘un-staked’. Staked Ether will be un-staked after the Shanghai upgrade, which will allow for the process to occur on the blockchain.

In response to the settlement, Coinbase stated that its staking services do not fall under the definition of securities and added that it would “defend this in court if necessary”.

Meanwhile, the New York Department of Financial Services (NYDFS) started investigating stablecoin issuer Paxos, the company behind Pax dollar (USDP) and Binance USD (BUSD), a Binance-branded stablecoin that’s offered through a white-label service.

Over the week, leading stablecoin issuer Tether has published its latest quarterly financials, in which it revealed it made a $700 million “net profit” in the last quarter of 2022, marking the first time the firm generated a profit.

Bank of England weighs CBDC with £20,000 cap

The Bank of England and HM Treasury are exploring the possibility of introducing a digital pound, a central bank digital currency (CBDC), which would be issued by the central bank and could be used for daily transactions, but with a per person limit of £20,000.

In the event of its launch, the digital pound would be interchangeable with both cash and bank deposits, meaning that £10 in digital form would hold the same value as £10 in physical cash.

The Bank of England stated that neither the central bank nor the government would have access to personal information and users would enjoy the same level of privacy as they would with a traditional bank account.

Over the week, enterprise software firm MicroStrategy notably revealed it’s weighing adding BTC futures contracts to its cryptocurrency strategy through CME Group’s marketplace in a bid to generate yield.

MicroStrategy had previously disregarded the notion of lending out its Bitcoin through other organizations, some of which faced bankruptcy in the past year. The company initiated its investment in Bitcoin in August of 2020, and to date, has accumulated 132,500 BTC, with a value of approximately $3 billion.

Francisco Memoria is a content creator at CryptoCompare who’s in love with technology and focuses on helping people see the value digital currencies have. His work has been published in numerous reputable industry publications. Francisco holds various cryptocurrencies.

The post Crypto narratives: Industry comes to Turkey’s aid, and SEC moves against staking appeared first on CityAM.