Penny stocks are often overlooked by investors due to their volatility. However, some penny stocks have the potential to become very profitable. Notably, with the global cancer drug market estimated to cross $289 billion by 2030, Elevation Oncology (ELEV) is one high-potential penny stock that's gaining attention for its unique approach to addressing unmet medical needs in oncology.

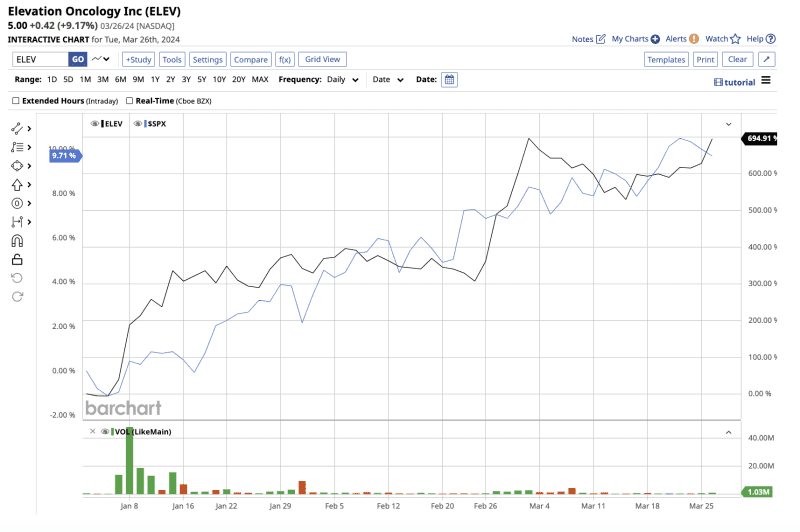

As investors consider the potential of this burgeoning field, Elevation Oncology stock has emerged as an intriguing opportunity with promising developments in its pipeline. This explains the stock's impressive gains so far; ELEV is up an eye-catching 825% year-to-date, far outperforming the S&P 500 Index's ($SPX) 9.7% gain.

Despite these enormous gains, Wall Street still expects more than 55% upside yet to come from Elevation stock this year. Let’s find out why.

Elevation Oncology’s Pipeline Progress Is Impressive

Elevation Oncology currently has no approved products on the market. Nonetheless, its pipeline includes several promising candidates for rare cancers with high unmet needs.

In February, the company extended its Phase 1 clinical trial of EO-3021 to Japan, dosing the first patient. EO-3021 is an antibody-drug conjugate (ADC) that is expected to be a potential treatment for "advanced, unresectable, or metastatic solid tumors likely to express Claudin 18.2, including gastric, gastroesophageal junction, pancreatic, or esophageal cancers."

Management stated that testing outside the U.S. will enable them to evaluate the "safety and efficacy profile of our anti-Claudin 18.2 agent in a diverse patient population." The company expects to provide an early update on the trial in mid-2024, with more updates expected in the first half of 2025.

The company's other flagship program is the HER3-ADC program. Elevation intends to present on HER3-ADC's potential for treating HER3-expressing cancers at the American Association for Cancer Research (AACR) Annual Meeting 2024,+Annual+Meeting+2024%2C) to be held in April.

Strong Cash Position

The company's net loss in the fourth quarter came in at $7.9 million, significantly lower than $19 million in the year-ago quarter. The company's cash, cash equivalents, and marketable securities totaled $83.1 million at the end of the year, down from $90.3 million in 2022. Elevation's debt-to-equity ratio is 0.55, which is not particularly high. However, being unprofitable while burning cash may burden the company.

Management believes that the cash balance, combined with the net proceeds of $17.0 million raised through its at-the-market (ATM) facility in 2023, will suffice until the fourth quarter of 2025.

It is not unusual for biotech companies to be unprofitable and lose money during their growth phase. However, biotech companies developing treatments for life-threatening diseases, such as cancer, have enormous growth potential once an approved and successful drug is on the market.

While the long-term prospects are appealing, investors should note that it may take years for the company to develop a successful drug that generates profits. This is probably why clinical-stage biotech companies work best for investors with a high-risk appetite.

What Is The Stock Price Prediction For ELEV?

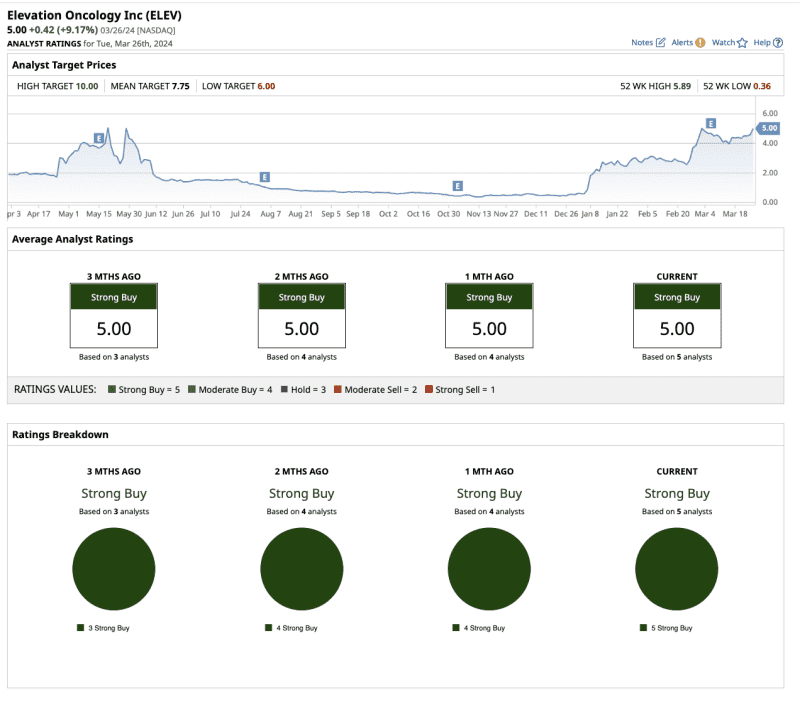

In March, H.C. Wainwright analyst Swayampakula Ramakanth reiterated his bullish stance on ELEV stock, maintaining a "buy" rating and a $6 price target. The analyst is impressed by the company's declining net losses, strong cash position, and progress in its clinical pipeline.

Furthermore, JMP Securities initiated coverage of the stock with a "buy" rating and a $7 price target. Additionally, Wedbush analyst Robert Driscoll raised the target price to $8 with a "strong buy" rating.

Overall, Wall Street rates Elevation stock a "strong buy,” with all five analysts in coverage giving the stock their highest rating.

The average target price for ELEV is $7.75, which implies an upside potential of 55% in the next 12 months. Plus, its high target price of $10 implies the stock could rise as high as 100% from current levels.

The Bottom Line on Elevation Oncology

While at the clinical stage, Elevation Oncology is in a good position with positive updates from its pipeline. Plus, its strong cash position and efficient use of capital should help the company going forward. As Elevation Oncology advances its pipeline and expands its reach, the future looks bright for patients with rare cancers.

Furthermore, as the world moves toward a cancer-free future, the company will have plenty of room for growth.

While choosing the right penny stock at the right time can result in substantial profits, there is also the risk of losing money. Given that, careful due diligence is required before investing in penny stocks, such as Elevation Oncology.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.