Biotech stocks can be volatile, because earnings typically don't stabilize until a few successful drugs have hit the market. However, AbbVie (ABBV), a global biotech company, has demonstrated its worth here. The company's status has been upgraded from "Dividend Aristocrat" to "Dividend King" after consistently paying and increasing dividends for the past 52 years. Dividend Kings are an elite group of companies that have consistently hiked their dividends for the past 50 years.

Since the patent expiration of its blockbuster immunology drug Humira, the company has suffered a setback. However, AbbVie has been wise in diversifying its revenue streams through many other successful drugs and strategic acquisitions, expanding its product portfolio.

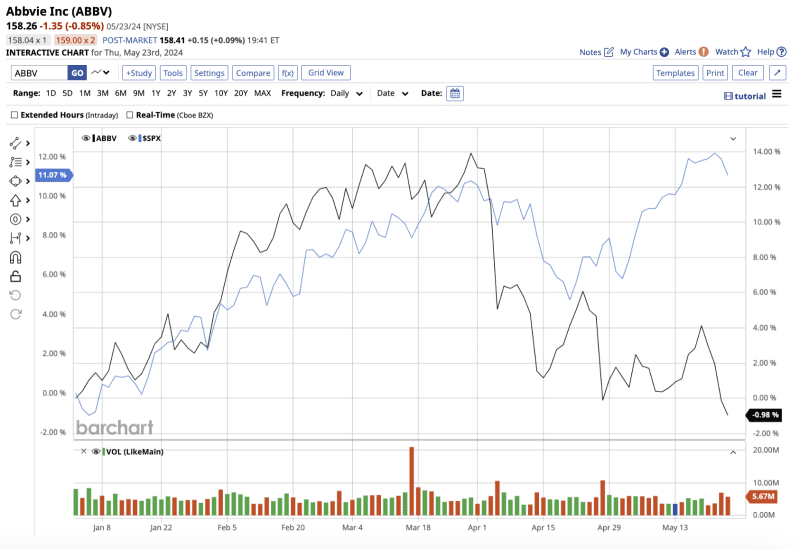

The stock has gained 1.4% year-to-date, compared to the S&P 500 Index’s ($SPX) gain of 11.2%. ABBV is also down 14% from its all-time high, making it an excellent time to buy this dividend stock on the dip.

AbbVie’s Financial Health Has Been Steady

AbbVie has grown significantly, thanks to a strong product portfolio and strategic acquisitions. Its portfolio includes many successful drugs. However, the success of its immunology drugs, and particularly Humira, drew investors' and analysts' attention in the last couple of years.

Humira (which treats autoimmune conditions) has been a significant revenue generator for the company. But Humira's US patent protection expired in 2023, leaving investors skeptical of AbbVie's future. In its recentfirst quarter of 2024, Humira generated $2.27 billion globally, a dip of 35.9% year-over-year.

However, AbbVie has strategically expanded its portfolio to reduce the impact of biosimilar competition. Newer drugs, such as Skyrizi and Rinvoq, which target autoimmune conditions, are showing promising results, helping to diversify revenue streams.

Notably, in Q1, global Skyrizi net revenues increased 47.6%, while global Rinvoq net revenues increased 59.3%. Furthermore, cancer treatments Imbruvica and Venclexta are expanding the company's oncology offerings. In Q1, the oncology segment contributed 13% of total revenue. Total revenue for the quarter fell 0.7% year on year to $12.3 billion, while adjusted diluted earnings fell 6.1% to $2.31 per share.

Strategic Acquisitions Could Boost Fundamentals

Towards the end of 2023, AbbVie also announced plans to acquire Cerevel Therapeutics. According to AbbVie, the company has a solid pipeline of "multiple clinical-stage and preclinical candidates with potential across several diseases, including schizophrenia, Parkinson's disease (PD), and mood disorders." The deal is worth approximately $8.7 billion in total equity and is expected to close in mid-2024.

This agreement aims to strengthen AbbVie's neuroscience pipeline, which currently accounts for just 15% of total revenue. I believe it will also help the company reduce its reliance on immunology drugs, which accounted for approximately 44% of total revenue in the first quarter.

Furthermore, in Q1, AbbVie completed the acquisition of ImmunoGen and its flagship cancer therapy, ELAHERE. This $10.1 billion deal is expected to help the company break into the commercial market for ovarian cancer. Despite these strategic deals, the company maintained a sturdy balance sheet, with $18 billion in cash and cash equivalents at the end of Q1.

Currently, AbbVie’s forward dividend yield of 3.9% is higher than the healthcare sector average of 1.58%. Its reasonable forward payout ratio of 51.5% implies the company’s earnings can sustain the current dividend payments, with chances for growth if earnings continue to increase.

Analysts tracking AbbVie stock predict a 1.5% increase in full-year revenue, with earnings rising 1.13% to $11.24, in line with management's expectations. Furthermore, revenue and earnings are expected to rise 5.2% and 7.4%, respectively, by 2025.

Currently, AbbVie stock trades at 14 times forward 2024 earnings, compared to its five-year historical average of 29x.

Is AbbVie a Buy Now, According to Wall Street?

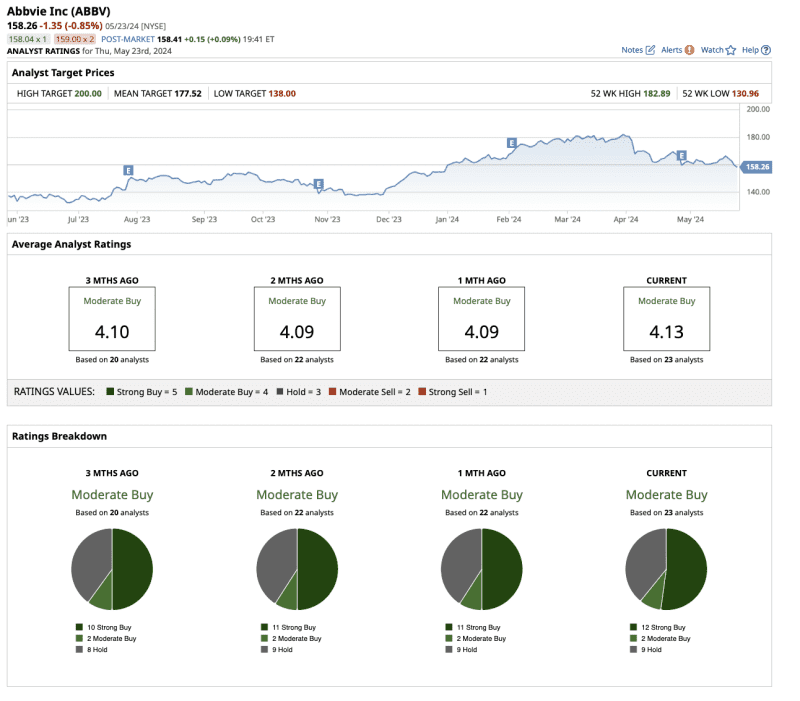

Following its Q1 results, Goldman Sachs analyst Chris Shibutani reiterated his "buy" rating and set a $190 price target for the stock.

Shibutani believes that despite the stock's recent underperformance, its future prospects are bright due to the company's "emerging products and anticipated pipeline assets." Barclays maintained the same bullish stance, setting a target price of $187.

More recently, TD Cowen analyst Steve Scala reiterated the "buy" rating and set a $180 price target. Scala believes AbbVie has strong long-term potential, and revised its sales and EPS estimates for 2024-25 upward. According to Scala, AbbVie's current valuation is an excellent entry point for investors looking to capitalize on the company's increasing returns in the coming years.

Likewise, Cantor Fitzgerald initiated coverage of the stock with a “strong buy” rating.

Overall, Wall Street has assigned a “moderate buy” rating to AbbVie stock. Out of 23 analysts covering the stock, 12 have a “strong buy” rating, two suggest a “moderate buy” rating, and nine recommend a “hold” rating. The mean target price for ABBV is $177.52, which is 13% above current levels. Its high price estimate of $200 implies a potential upside of 27.3% over the next 12 months.

Is This Dividend King A Buy Now?

AbbVie's attempts to strengthen its fundamentals through strategic acquisitions demonstrate its commitment to increasing earnings and returning value to shareholders.

The company has demonstrated its value as a Dividend King, and is an excellent addition to an income-oriented investor's portfolio. However, it also makes a compelling case for a growth stock, with a strong product portfolio of successful drugs and many more in the works.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.