Oil prices (CLN24) took a hit earlier this week, triggered by OPEC's decision to ramp up production. However, prices swiftly bounced back from their four-month lows, as optimism surrounding anticipated interest rate cuts in the months ahead countered the negative sentiment.

Apart from the optimism surrounding interest rate cuts this year, oil prices are finding support due in part to concerns stemming from the conflict between Hamas and Israel. According to the U.S. Energy Information Administration (EIA), ongoing geopolitical risks are expected to support the Brent crude oil spot price around $90 per barrel for the remainder of 2024.

As oil prices move higher off their recent lows, three affordable dividend-paying energy stocks - Matador Resources Company (MTDR), Civitas Resources, Inc. (CIVI), and Crescent Energy Company (CRGY) \- could be ideal investment candidates now.

Dividend Stock #1: Matador Resources

Valued at $7.2 billion by market cap, Texas-based Matador Resources Company (MTDR) is an independent U.S. energy company specializing in the exploration, development, production, and acquisition of oil and natural gas (NGN24), with a focus on shale and unconventional plays. Matador also offers midstream services like natural gas processing, oil transportation, and water management.

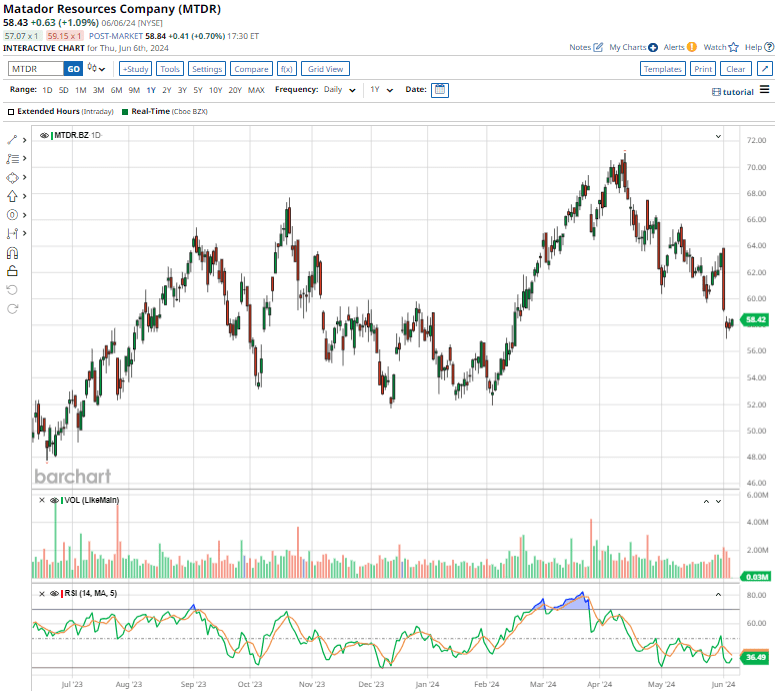

Over the past 52 weeks, the company’s shares have surged nearly 20%.

On April 17, the oil and gas exploration company declared a quarterly dividend of $0.20 per share, payable to its shareholders on June 7. Its annualized dividend of $0.80 translates to a 1.36% dividend yield. With a conservative payout ratio of 10.09%, the company has substantial room for further dividend increases.

Moreover, priced at 7.71 times forward earnings, the stock trades at a discount to its industry median and its own five-year average.

Matador reported its Q1 earnings results on April 23, blowing past Wall Street’s forecasts. The company’s total revenue of $787.7 million jumped a notable 40.6% annually, outshining estimates by nearly 7.3%. Its adjusted EPS of $1.71 registered a 14% annual growth, also surpassing projections by 15.5%.

During the quarter, Matador achieved an average daily production of 149,760 barrels of oil and natural gas equivalent (BOE), surpassing the previously announced guidance of 145,750 BOE per day. Notably, average oil production hit 84,777 barrels per day, marking a remarkable 44% year over year increase and exceeding the upper limit of its earlier guidance.

Encouraged by these better-than-expected production results, management now expects oil production for fiscal 2024 to reach the higher end of its previously announced average production guidance, ranging between 91,000 barrels per day and 95,000 barrels per day. Similarly, the total average production for fiscal 2024 is also projected to be at the upper end of its earlier guidance of 153,000 BOE per day to 159,000 BOE per day.

Analysts tracking Matador project the company’s profit to climb 13.4% year over year to $7.68 per share in fiscal 2024, and grow another 8.3% to $8.32 per share in fiscal 2025.

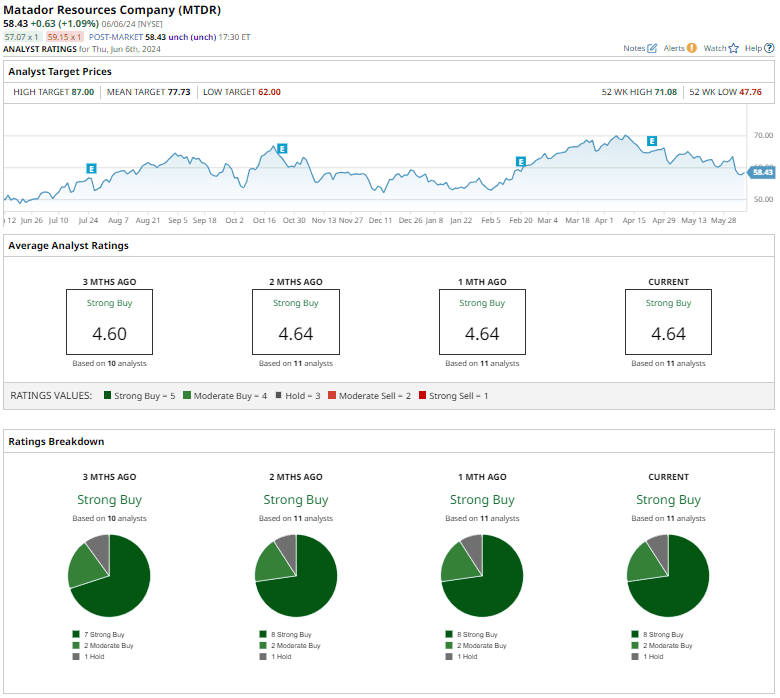

Matador Resources stock has a consensus “Strong Buy” rating overall. Out of the 11 analysts covering the stock, eight suggest a “Strong Buy,” two advise a “Moderate Buy,” and the remaining one gives a “Hold” rating.

The average analyst price target of $77.73 indicates a potential upside of 33% from the current price levels. However, the Street-high price target of $87 suggests that the stock could rally as much as 48.9%.

Dividend Stock #2: Civitas Resources

Established in 1999, Colorado-based Civitas Resources, Inc. (CIVI) is a leading independent U.S. oil and gas producer, concentrating on its top-tier assets in the Denver-Julesburg (DJ) and Permian Basins. As Colorado’s first carbon-neutral oil and gas producer, Civitas leads in environmental, social, and governance (ESG) practices. The company’s market cap currently stands at $6.8 billion.

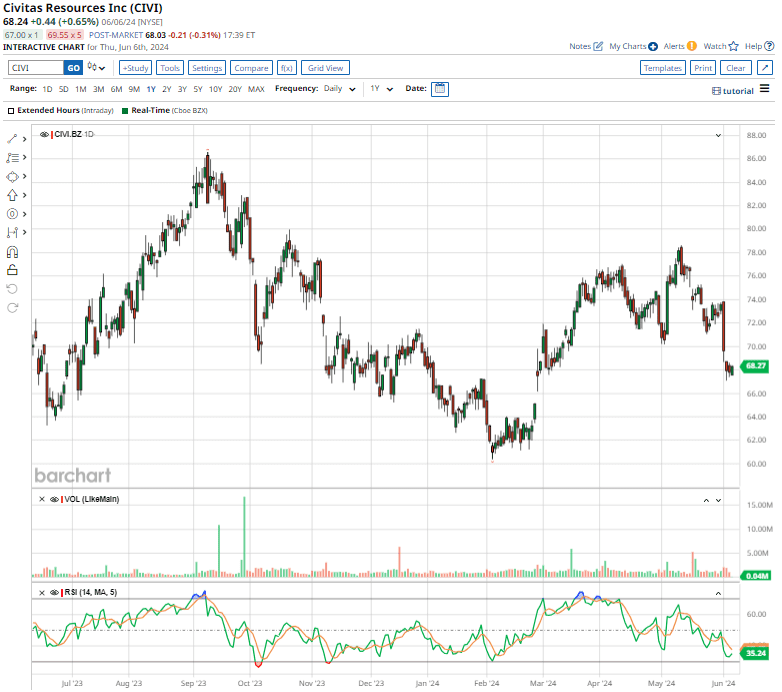

The stock has tumbled 3.3% over the past 52 weeks.

On May 2, the company announced a base quarterly dividend of $0.50 per share, along with a variable payout of $1.00 per share. Its annualized dividend of $2.00 translates to a 2.93% forward yield, while investors have realized a trailing yield north of 10% in the last 12 months.

In terms of valuation, the stock is trading at 5.81 times forward earnings, which is much lower than its industry median.

Following the Q1 earnings results revealed on May 2, the company’s shares soared 7% in the subsequent trading session, triggered by the better-than-expected top- and bottom-line figures. Its total operating net revenue of $1.3 billion climbed a whopping 102.6% annually, sailing past estimates by 3.5%. Also, adjusted EPS of $2.74 increased 24.5% sequentially, topping predictions by 8.3%.

The remarkable revenue growth during the quarter primarily stemmed from a 19% increase in sales volumes, accompanied by slightly reduced realized commodity prices. Notably, crude oil contributed 81% to the total revenue for Q1.

CEO Chris Doyle said, “In the Permian, our execution is already unlocking value through improved cycle times and cost reductions, and in the DJ, performance continues to exceed expectations. We surpassed our goal to sell $300 million in non-core assets, and we will use the proceeds to strengthen our balance sheet and support our shareholder return program."

For fiscal 2024, management reiterated its oil and total equivalent production volume to range between 325 MBoe/d and 345 MBoe/d. Furthermore, capital expenditure is estimated to be between $1.8 billion and $2.1 billion.

Analysts tracking Civitas expect the company’s profit to reach $12 per share in fiscal 2024, up 33% year over year, and rise another 16.7% to $14 per share in fiscal 2025.

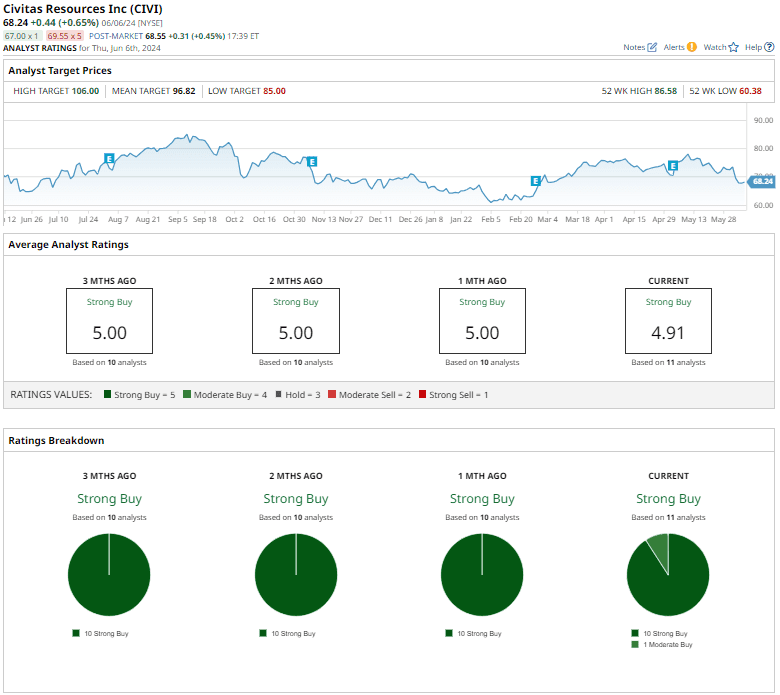

Civitas stock has a consensus “Strong Buy” rating overall. Out of the 11 analysts offering recommendations for the stock, 10 suggest a “Strong Buy,” and the remaining one gives a “Moderate Buy” rating.

The average analyst price target of $96.82 indicates a potential upside of 41.9% from the current price levels, while the Street-high price target of $106 suggests a potential upside of 55.3%.

Dividend Stock #3: Crescent Energy

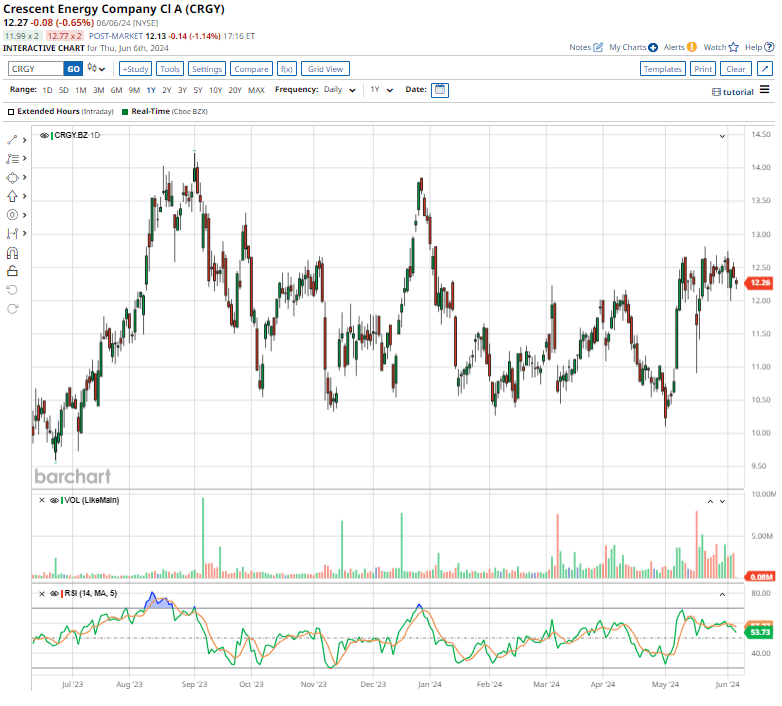

Headquartered in Houston, Texas, Crescent Energy Company (CRGY) is a U.S. energy company focused on acquiring, developing, and producing crude oil, natural gas, and natural gas liquids (NGLs) reserves. With a market cap of about $2.2 billion, the company’s portfolio includes low-decline, cash-flow-oriented unconventional and conventional assets in the Eagle Ford and Uinta basins, featuring long reserve lives and high-return development locations.

Shares of Crescent Energy have soared 24.9% over the past 52 weeks and 13.8% over the past month.

The company is committed to returning value to its shareholders. On May 6, management approved a $150 million share buyback initiative until March 2026, and announced a quarterly dividend of $0.12 per share, payable to its shareholders on June 7. Its annualized dividend of $0.48 offers an attractive 3.89% dividend yield. Moreover, Crescent maintains a healthy dividend payout ratio of 38.31%.

Priced at 7.51 times forward earnings, the stock trades at a discount to its industry median.

Alongside its dividend announcement, Crescent unveiled its Q1 earnings results on May 6, sparking a remarkable 10.1% surge in its shares during the subsequent trading session.

The company’s total revenue increased 11.4% year over year to $657.5 million, and topped Wall Street’s estimates by 12.4%. Its adjusted net income of $83 million showed a strong 54.8% annual improvement. Moreover, during Q1, production hit a record high, averaging 166 MBoe/d, with 42% oil and 59% liquids.

Crescent CEO David Rockecharlie said, “We entered 2024 with strong momentum and again exceeded market expectations in the first quarter, achieving record quarterly production, generating robust operating cash flows and demonstrating the merits of our proven and differentiated business model to create long-term value for shareholders.”

For fiscal 2024, management revised its production guidance upward, forecasting it to range between 157 MBoe/d and 162 MBoe/d. Analysts tracking Crescent Energy project the company’s profit to come in at $1.65 per share in fiscal 2024 and grow 82.4% to $3.01 per share in fiscal 2025.

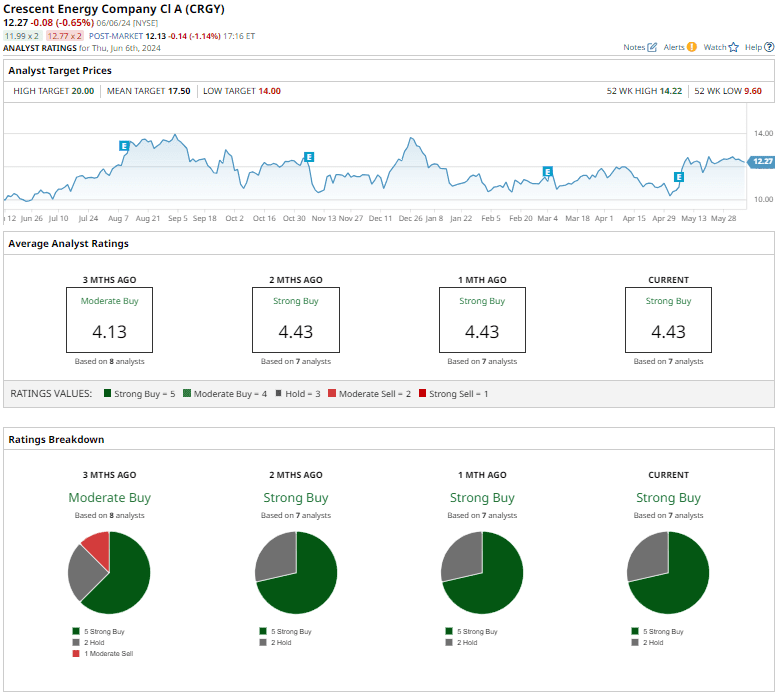

Crescent Energy stock has a consensus “Strong Buy” rating overall. Out of the seven analysts covering the stock, five suggest a “Strong Buy,” and the remaining two give a “Hold” rating.

The average analyst price target of $17.38 indicates a notable potential upside of 42.6% from the current price levels. However, the Street-high price target of $20 suggests that the stock could rally nearly 63%.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.