Amid concerns over OPEC+ production levels, some high-quality energy stocks have pulled back recently, potentially presenting attractive entry points for investors. One such name is Sunoco LP (SUN), a fuel distributor that has seen its stock price drop 17.3% since its early March highs, despite delivering robust Q1 results.

SUN is currently down more than 10% year-to-date, significantly underperforming the Alerian MLP ETF's (AMLP) 10.5% gain, as investors weigh concerns around the company's $5.7 billion acquisition of NuStar Energy. However, some analysts see the pullback in SUN as overdone. JPMorgan, Mizuho, and Stifel have all upgraded SUN recently, suggesting the stock's dip could be a prime buying opportunity.

With the NuStar deal expected to generate at least $150 million in synergies, the stock offering a 6.52% yield, and trading at a discount to peers, Sunoco could offer compelling value for income-oriented investors. Let's take a closer look at the bull case.

Sunoco's Recent Pullback and Valuation

Valued at $5.4 billion by market cap, Sunoco LP (SUN) is one of the largest independent fuel distributors in the U.S., supplying motor fuel to convenience stores, independent dealers, commercial customers, and distributors. They also run retail fuel sites and convenience stores.

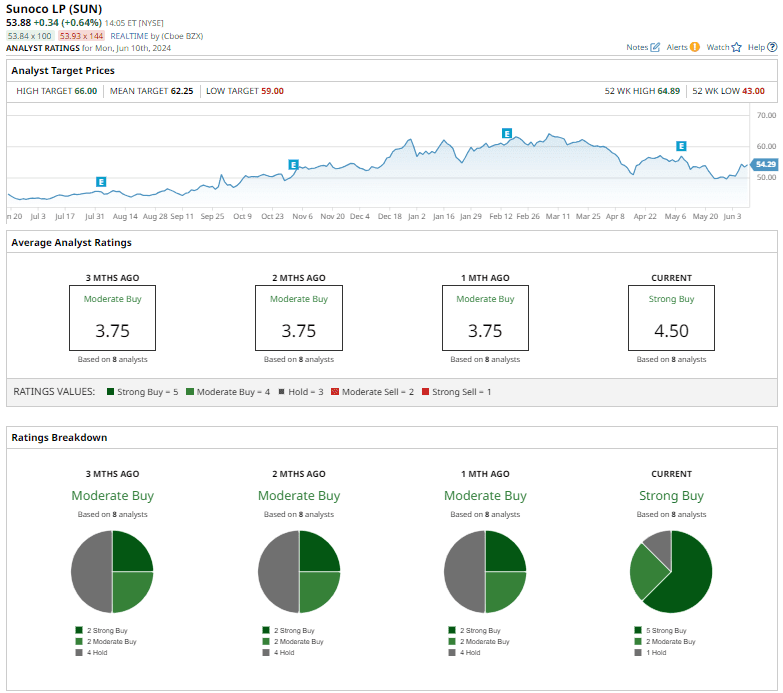

SUN stock is up 21.3% over the past 52 weeks, though the shares have pulled back double digits from the 52-week high near $65 set in March.

The recent dip has the stock changing hands at a discount to its industry peers. SUN is trading at a forward P/E of around 9.04x, a discount to the energy sector average of 11x and SUN's 5-year historical average of roughly 12x. The stock's price-to-sales ratio of 0.20 also looks cheap compared to a sector median of 1.41x.

Sunoco's Q1 2024 financial performance was strong, with record net income of $230 million, up from $141 million the previous year. Adjusted EBITDA also increased to $242 million from $221 million year-over-year.

The company's total quarterly revenues hit $5.49 billion, up from $5.36 billion last year, driven by strong performance in the Fuel Distribution and Marketing segment, which alone generated $5.31 billion in revenue. Sunoco reported GAAP EPS of $2.26 for Q1 2024, while adjusted earnings of $1.06 were in line with estimates.

For the full year 2024, Sunoco has revised its adjusted EBITDA outlook to range between $1.46 billion and $1.52 billion, boosted by contributions from the recent NuStar acquisition, which is expected to add $480 million to $520 million in adjusted EBITDA for the year.

The Key Drivers Behind Sunoco's Strong Fundamentals

Sunoco LP has been making big strategic moves to boost its growth prospects and financial stability. The $7.3 billion acquisition of NuStar Energy L.P., approved by NuStar unitholders in May, is a game-changer. This merger is expected to bring at least $150 million in expense and commercial synergies, plus an additional $50 million per year in cash flow from refinancing activities. This acquisition enhances Sunoco's credit profile and promises an immediate boost to distributable cash flow per LP unit, with growth expected to exceed 10% by the third year after the deal closes.

On top of the NuStar acquisition, Sunoco has also completed the purchase of European liquid fuel terminals from Zenith Energy and divested 204 convenience stores to 7-Eleven, Inc.

These growth drivers are complemented by Sunoco's robust dividend history. The company has consistently paid dividends for over 20 years, reflecting its commitment to returning value to shareholders. The most recent dividend payment was $0.876 per unit, translating to an annual rate of $3.50 per unit and a yield of 6.52%.

Like most MLPs, Sunoco maintains a high payout ratio, but its stable financial performance supports this generous distribution. The company recently announced a 4% increase in its quarterly distribution, following its 2% increase last year.

Analyst Upgrades and Future Prospects: A Bullish Outlook for Sunoco

Analysts are bullish on Sunoco's prospects. The stock currently has a consensus rating of "Strong Buy" based on recommendations from eight analysts, up from “Moderate Buy” one month ago. This includes five “Strong Buy” ratings, two “Moderate Buy” ratings, and one “Hold” rating.

The average price target for Sunoco is $62.25, suggesting 16% upside potential.

JPMorgan recently upgraded Sunoco from “Neutral” to “Overweight”, setting a price target of $61. This upgrade was largely influenced by Sunoco's acquisition of NuStar Energy, which JPMorgan analyst Jeremy Tonet described as "transformational" due to its potential to diversify Sunoco's business and enhance stability and growth opportunities.

Similarly, Mizuho Securities upgraded Sunoco from “Neutral” to “Buy”, although they adjusted their price target slightly down to $59. Mizuho's analyst highlighted that Sunoco's current market valuation doesn't fully reflect the company's strong outlook, including anticipated EBITDA growth and synergies from the NuStar acquisition.

And on June 5, Stifel also upgraded Sunoco from “Hold” to “Buy”, and maintained a price target of $62, citing the significant decline in Sunoco's unit price as an attractive entry point for investors.

Conclusion

So is it time to fill up the tank on SUN? The valuation looks pretty reasonable, and you're getting paid a hefty 6%+ dividend to wait for the next positive catalyst. The analyst upgrades and fundamental momentum are encouraging - but, as always, energy stocks can be a wild ride, and you've gotta watch that macro picture. My 2 cents are that SUN could be an interesting name for income-focused investors who don't mind a little volatility.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.