The S&P 500 Index ($SPX), one of the most widely followed equity benchmarks globally, is gearing up for its quarterly rebalancing.

Every quarter, S&P Global (SPGI) adjusts its indexes, like the S&P 500, evaluating new contenders and considering businesses that may have become too small. Throughout the year, adjustments are made for spin-offs, acquisitions, and other corporate events affecting inclusion.

In the latest SPX update, a trio of top-rated stocks – CrowdStrike Holdings, Inc. (CRWD), KKR & Co. Inc. (KKR), and GoDaddy Inc. (GDDY) – are set to join the prestigious index effective June 24, elbowing out the Texas-based bank Comerica (CMA), human resources consulting firm Robert Half (RHI), and genetic analysis company Illumina (ILMN) in the process.

The S&P 500 addition should draw new volume and buying interest to these three stocks, as institutional investors pick up shares to make sure their portfolios track with the benchmark. However, analysts had CRWD, KKR, and GDDY named as stocks to buy already. Here’s a closer look at why.

Stock #1: CrowdStrike Holdings

Headquartered in Austin, Texas, CrowdStrike Holdings, Inc. (CRWD) is a leading global cybersecurity firm renowned for its cutting-edge cloud-native platform. The CrowdStrike Falcon platform, fortified with artificial intelligence (AI) and the CrowdStrike Security Cloud, leads the charge in real-time attack detection, automated protection, and swift deployment, streamlining operations and delivering instant results. CrowdStrike continues to innovate, setting benchmarks in the cybersecurity realm and expanding its footprint in safeguarding organizations against evolving cyber threats worldwide.

Against a backdrop of rising data breaches, CrowdStrike has been benefiting from the soaring demand for cybersecurity solutions. Its sustained focus on rolling out new products, acquisitions, and partnerships is expected to continue to boost sales.

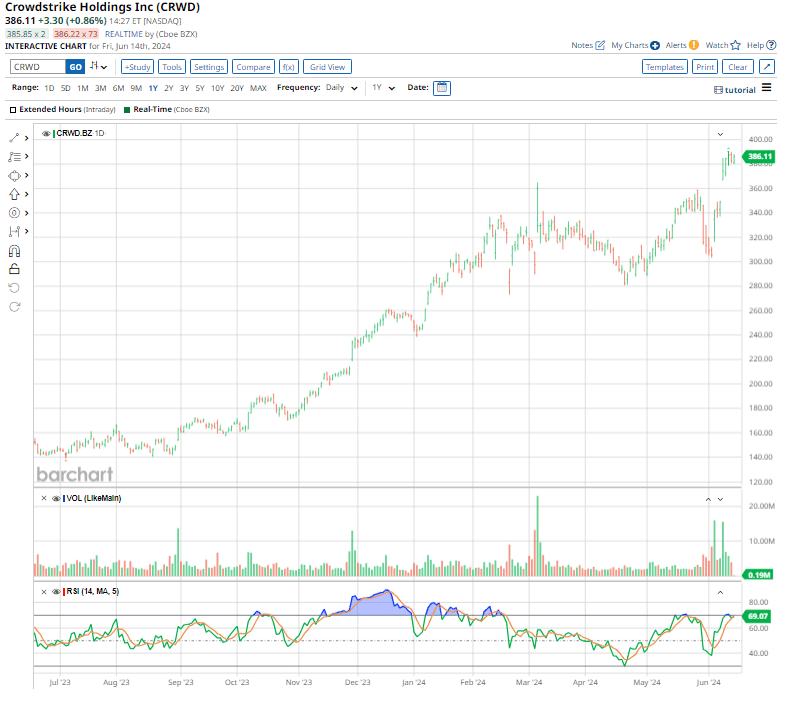

It’s no wonder that the cybersecurity leader, which has now reported five consecutive profitable quarters, with a market cap of $92.5 billion, is set to join the S&P 500 Index this June. Following the announcement by S&P Dow Jones Indices after the close last Friday, CrowdStrike stock surged more than 10% over the next two trading sessions.

Shares of CrowdStrike have soared by 150.6% over the past 52 weeks and 51.1% on a YTD basis, substantially outpacing the SPX, which gained 24% and 13.7%, respectively, over the same time frames. CRWD stock also outperformed the Nasdaq Cybersecurity ETF's (CIBR) returns of 21.1% over the past 52 weeks and 1.7% in 2024.

The stock is currently trading at 423 times forward earnings, significantly higher than its closest peers; however, on an adjusted basis, the forward P/E of 95.24 is a discount to peer Palo Alto Networks (PANW).

The stock’s impressive double-digit YTD gains are due in part to CrowdStrike’s positive earnings on June 4, which beat Wall Street’s estimates. CRWD stock popped nearly 12% in the subsequent trading session. Its Q1 total revenue increased 33% year over year to $921 million, beating the estimate of $904.8 million. Its subscription revenue amounted to $872.2 million, up 34% annually.

CrowdStrike’s net new annual recurring revenue (ARR) grew 22% to $212 million, and the company delivered a record operating cash flow of $383 million and a record free cash flow of $322 million, or 35% of revenue. The company’s non-GAAP net income rose 63% to $0.93 per share, compared to the Wall Street estimate of $0.89 per share.

Investors were thrilled not only by CrowdStrike's Q1 growth but also by its optimistic guidance. Management's forecast for fiscal 2025 calls for revenue to soar between $3.98 billion and $4.01 billion, marking a robust 31% surge. Non-GAAP EPS is projected to be between $3.93 and $4.03, further fueling excitement about the company's trajectory.

Analysts tracking CrowdStrike expect GAAP EPS to grow 82% in fiscal 2025 and 55% in fiscal 2026.

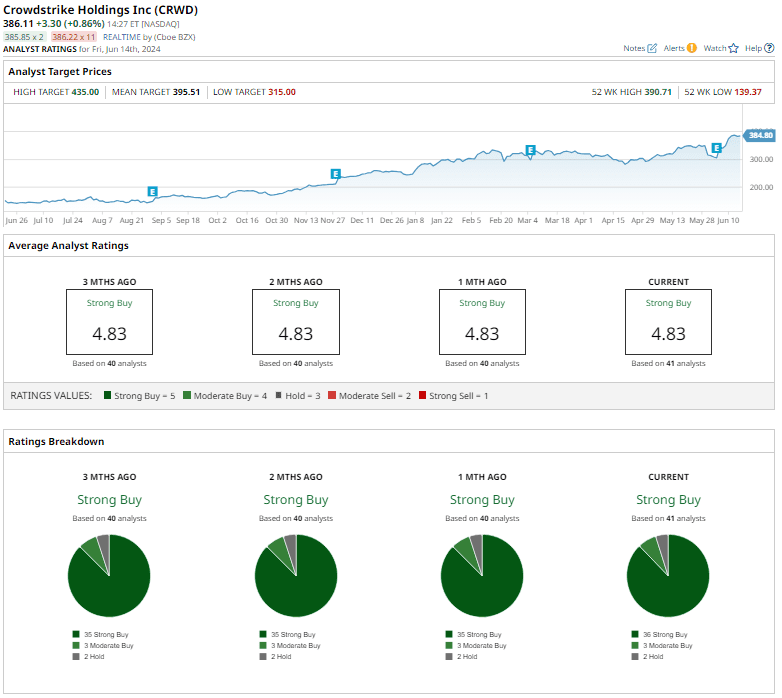

CRWD has a consensus “Strong Buy” rating overall. Of the 41 analysts covering it, 36 recommend “Strong Buy,” three suggest “Moderate Buy,” and two say “Hold.”

The average analyst price target for CrowdStrike is $395.98, indicating a potential upside of just 2.5%. The Street-high target price of $435 implies a 12.6% upside potential.

Stock #2: KKR & Co.

Founded in 1976, New York-based KKR & Co. Inc. (KKR) is a powerhouse in private equity and real estate investments, known for strategic acquisitions and leveraged buyouts across diverse sectors, including software, cybersecurity, energy, and infrastructure. With a global footprint spanning North America, Europe, Asia, and beyond, KKR targets businesses with significant growth potential and social impact. It operates through a network of offices worldwide, driving innovation and growth in its extensive portfolio of companies and real estate investments.

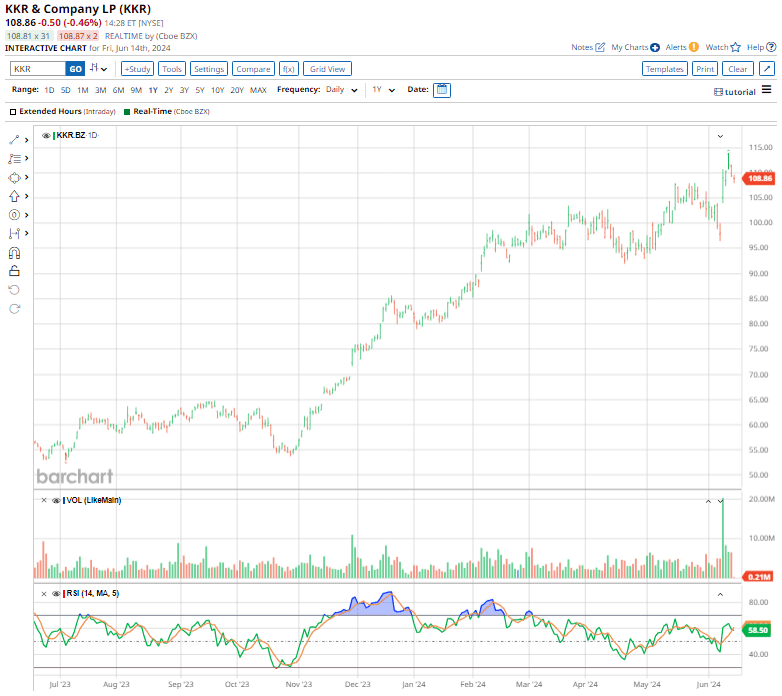

KKR's inclusion in the S&P 500 index underscores its robust growth in the private investment sector, and follows the addition of Blackstone (BX) to the benchmark last year. With ambitions to manage $1 trillion in assets within five years, the S&P nod helps KKR to solidify its role as a major industry player.

Following the announcement, KKR stock gained 13.8% over the first three trading sessions of this week. This momentum adds to its impressive gains, with shares of KKR up 91.8% over the past 52 weeks and 32% on a YTD basis. That exceeds not just the SPX’s returns, but also the gains of the iShares US Financials ETF (IYF).

On May 1, KKR treated its shareholders to a quarterly dividend bump, paying a dividend of $0.175 per share on May 28, up 6%. This marks the fifth consecutive year of dividend hikes since KKR restructured, boosting its annual payout from $0.50 to $0.70 per share. This annualized dividend now translates to a 0.64% yield. With a conservative payout ratio of 21.77%, KKR has ample room for future increases, reinforcing its commitment to rewarding investors.

Priced at 27.15 times forward earnings and 6.75 times sales, the stock trades at a discount to its industry peer, Ares Management Corporation (ARES).

Shares of KKR rose 2.2% on May 1 following a stellar Q1 earnings report. Its total asset management segment revenues improved 9.5% annually to $1.4 billion, while its adjusted EPS of $0.97 surged 19.8%, fueled by strong management and transaction fees.

Fee-related earnings (FRE) rose 22% to $668.7 million, thanks to income from managing $578 billion in total assets and transaction fees from financing its own deals. KKR also completed a $2.7 billion acquisition of the remaining 37% stake in Global Atlantic.

Looking ahead to Q2, KKR is optimistic about a strong pipeline of new deployments driven by broad firm-wide activities. Over the next 12 to 18 months, it anticipates raising over $300 billion in capital for over 30 strategies by 2026. Management projects over $4.50 per share of FRE, more than $7 total operating earnings per share, and adjusted EPS between $7 and $8.

Longer term, KKR foresees over $15 in adjusted EPS within 10 years, with about 70% being recurring. Over the next five years, it projects over $25 billion in cash generation, earmarked for core private equity, share buybacks, strategic M&A, and insurance.

Analysts tracking KKR expect the company’s profit to surge 45.5% to $4.06 per share in fiscal 2024 and rise another 31.3% to $5.33 per share in fiscal 2025.

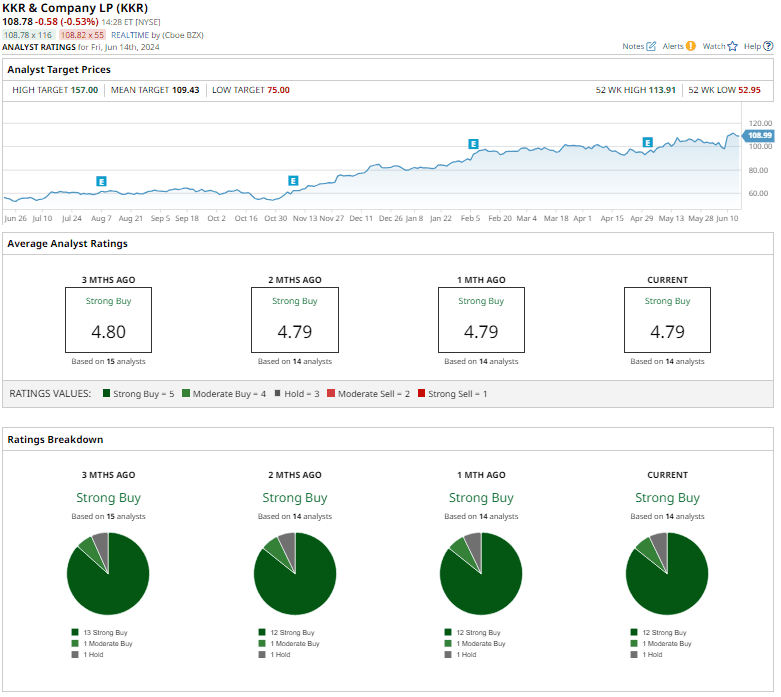

KKR stock has a consensus “Strong Buy” rating overall. Out of the 14 analysts offering recommendations for the stock, 12 suggest a “Strong Buy,” one advises a “Moderate Buy,” and the remaining one gives a “Hold” rating.

The average analyst price target of $109.43 suggests that the stock has only marginal upside potential to the current price levels, but the Street-high price target of $157 suggests that KKR could rally as much as 44.1%.

Stock #3: GoDaddy

Tempe, Arizona-based GoDaddy Inc. (GDDY) is a heavyweight in domain registration, web hosting, and website-building services. With a market cap of $19.7 billion, GoDaddy’s user-friendly platform and strong brand recognition empower small and medium-sized businesses to thrive online. Its robust business model, fueled by recurring revenue from domain registrations and hosting, ensures steady growth. Strategic acquisitions and innovations, like AI-driven customer support and advanced security features, further sharpen GoDaddy's competitive edge, solidifying its place as a leader in the digital space.

Shares of the e-commerce software company have gained 84.4% over the past 52 weeks and 29.3% on a YTD basis. This impressive performance not only outpaces the SPX’s gains, but also eclipses the GX E-Commerce ETF’s (EBIZ) 28.8% returns over the past year and 10.9% YTD gains.

In terms of valuation, GDDY stock is trading at 28.66 times forward earnings, much lower than its own five-year average of 60.06x.

On May 2, the domain registrar and web services company reported better-than-expected Q1 earnings results. Revenue rose 7% year over year to $1.1 billion, slightly above estimates, driven by A&C revenue growth of 13%.

The 9.5% rise in total bookings was fueled by growing customer adoption of productivity solutions and add-ons, price hikes, strength in domains and aftermarkets, and strong demand for website-building products. EPS of $2.76 surged a whopping 820% annually, also impressively exceeding projections.

GoDaddy’s normalized EBITDA (NEBITDA) of $313.0 million rose 25% annually, representing a 28% margin and exceeding the Q1 guidance of 27%. The company’s free cash flow rose 26% to $327.4 million, and as of March 31, total cash and cash equivalents amounted to $664 million.

GoDaddy is expecting Q2 revenue between $1.10 billion and $1.12 billion, which would mark 6% annual growth at the midpoint. A&C revenue growth is projected to be in the low- to mid-teens, with core revenue in the low single digits and a NEBITDA margin of around 28%.

For the current fiscal year, GoDaddy raised its revenue forecast, and is now projecting between $4.50 billion and $4.56 billion, representing 6.5% growth at the midpoint. NEBITDA margin is set at 29%, with Q4 hitting 31%. Free cash flow is projected to be at least $1.2 billion, an 11% annual increase.

Analysts tracking GoDaddy expect the company’s profit to reach $4.82 per share in fiscal 2024, up 71.5% year over year, and rise another 27.8% to $6.16 per share in fiscal 2025.

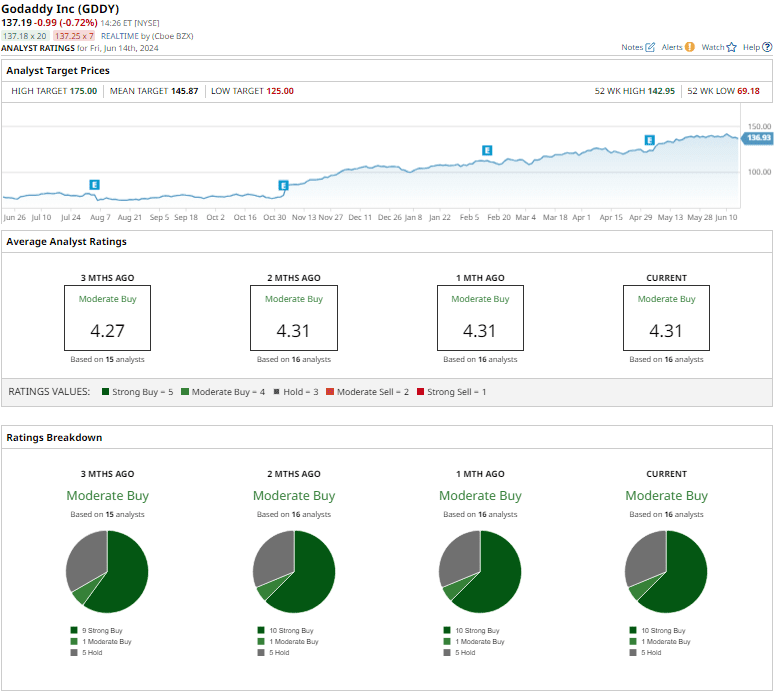

GoDaddy stock has a consensus “Moderate Buy” rating overall. Out of the 16 analysts covering the stock, 10 suggest a “Strong Buy,” one advises a “Moderate Buy” rating, and the remaining five recommend a “Hold.”

The average analyst price target of $145.87 indicates a potential upside of 6.4% from the current price levels. However, the Street-high price target of $175 suggests that GDDY stock could rally as much as 27.6%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.