Blue Bird Corporation (BLBD), established in 1927, manufactures school buses. The company boasts a diverse portfolio that includes both traditional and electric school buses. There are over 20,000 propane, natural gas, and electric buses on the road today.

Blue Bird stock has returned a staggering 469% in the last decade. Its improving fundamentals and positive long-term outlook for providing sustainable transportation solutions have made Wall Street optimistic about the stock, with most analysts rating it a “strong buy.”

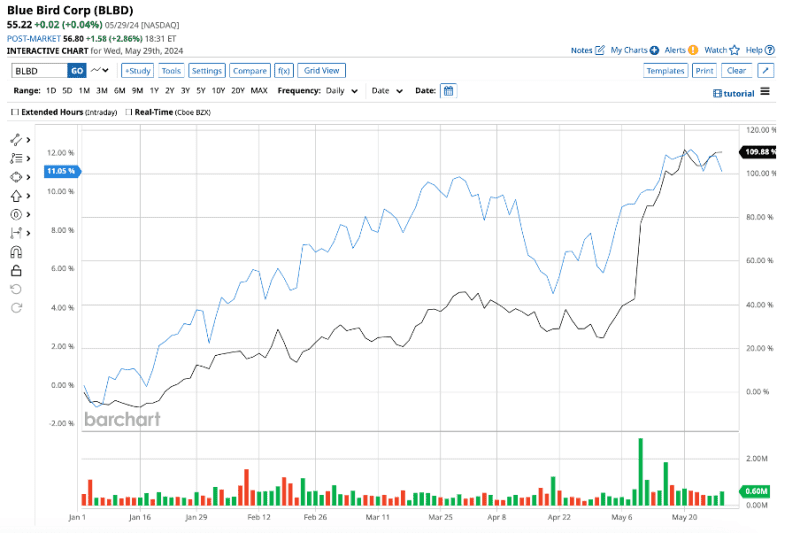

Recently, the company reported another strong quarter that exceeded Wall Street's expectations. The stock is up 110.5% year to date, massively outperforming the S&P 500 Index's ($SPX) gain of 10.2%.

Nonetheless, analysts believe there is still room for it to rise further this year. Let's find out why.

Is Blue Bird A Buy After Strong Q1 Earnings?

Blue Bird has consistently reported steady revenue growth, due to increased demand for school buses and successful expansion into the electric vehicle (EV) market.

In the fiscal second quarter, total revenue increased by 15% year on year to $345.9 million. Management stated that market demand for its school buses remains strong, with 5,900 units in backlog.

Adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) remained at a record high of $46 million in the quarter, up $25 million from the year before. Adjusted net income of $0.89 per share increased by a whopping 229% from the same quarter last year. Both revenue and earnings exceeded consensus estimates.

How’s the Future Looking For Blue Bird?

The demand for school buses is unlikely to subside any time soon. Furthermore, the global shift toward sustainable transportation is a significant tailwind for Bluebird. The company's early entry into the electric school bus market gives it an advantage as school districts across the country work to reduce carbon emissions.

Increased government funding and subsidies for green transportation solutions are expected to boost demand for Blue Bird's electric buses. Last year, the company received $1 billion in funding through Phase 1 of the EPA's $5 billion Clean School Bus program. Blue Bird had 500 electric school bus orders on the backlog at the end of the second quarter.

Furthermore, the company expects to receive new EV orders during Phase 2 (A and B) of the five-year program.

At the end of the second quarter, Blue Bird had $93 million in cash and cash equivalents. Its debt-to-equity ratio of 0.92 seems to be on the higher side. However, with steady earnings and free cash flow (FCF) growth, the company should be able to manage its debt effectively.

Management expects to generate an adjusted FCF of around $70 million to $80 million in 2024. With adequate liquidity, Blue Bird is well-positioned to invest in future growth opportunities, particularly in the EV segment.

Thanks to the strong second quarter, Blue Bird raised its full-year revenue guidance to a range between $1.275 billion and $1.325 billion, indicating growth of 12.5% to 16.9%. Adjusted EBITDA could land between $145 million and $165 million, an increase of 65% to 87%.

Analysts covering Blue Bird expect fiscal 2024 revenue and earnings to increase by 16.6% and 152.8%, respectively. Revenue and earnings could further rise by 11% and 15%, respectively, in 2025.

Trading at 20 times forward 2024 earnings, Blue Bird appears to be a reasonable buy right now, given the earnings growth expected in 2024 and future growth opportunities.

What Does Wall Street Say About Blue Bird Stock?

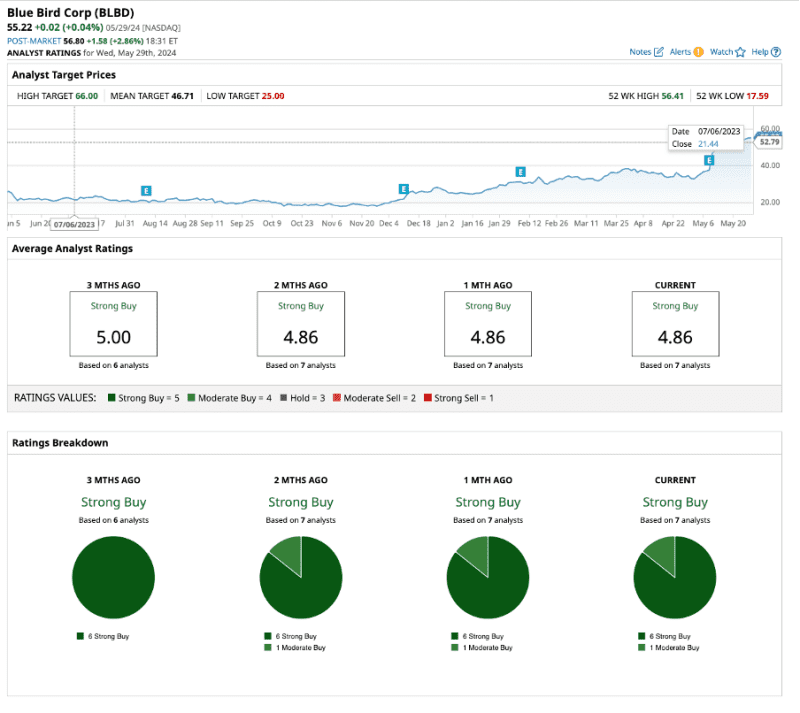

Wall Street remains highly optimistic about Blue Bird stock, rating it a “strong buy” overall.

Recently, Barclays analyst Adam Seiden reiterated his "buy" rating for Blue Bird stock, with a $43 price target. Seiden is pleased with the company's entry into the commercial vehicle market with its step-van offering, which he believes has the "potential to double its Total Addressable Market (TAM)."

For context, Blue Bird debuted its electric-powered step van at the Advanced Clean Transportation (ACT) Expo on May 20.

Seiden further added, “The company’s move into the step-van market is not only a strategic growth initiative but also enhances its electric vehicle narrative, an increasingly important factor in the industry.”

He believes that the company's core business of manufacturing school buses represents a stable foundation, with the transition to step-vans catalyzing growth in the years ahead.

Six of the seven analysts who cover the stock have given it a "strong buy," while one has a "moderate buy" rating. Blue Bird is trading well above its mean target price of $46.71. However, the high target price of $66 suggests that the stock could rise 16.2% over the next 12 months.

The Bottom Line on Blue Bird Stock

Blue Bird, like many other manufacturers, is vulnerable to supply chain disruptions, which can affect production schedules and raise costs. However, management expects global supply chain recovery to continue, leading to "sustained profitable growth in the coming years."

Overall, Blue Bird offers a balance of stability and growth potential. The company's strong market position, combined with its strategic focus on electric vehicles, lays the groundwork for future growth, making it an ideal buy-and-hold stock for the long term.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.