DocuSign Inc (DOCU), the eSignature software company, is a free cash flow (FCF) juggernaut. It has almost no capex requirements and produces nearly one-third of sales as FCF. That happened this past quarter with its June 6 release of quarterly earnings for its fiscal quarter ending April 30, 2024.

So, why is DOCU stock so far off its highs? It's trading for $51.35 per share in midday trading on Tuesday, June 11, down from $60.83 on May 15. After all, it's very cheap, trading at an FCF yield of 8.66%. This can be seen by dividing its trailing 12-month (TTM) FCF of $904.6 million by its market valuation today of $10.44 billion.

That FCF yield is way too high. The true value of the stock is at least $72 per share, or 40% more. Here's why.

Strong FCF Margins and Cheap Valuation

DocuSign produced a 32.7% FCF margin this past quarter (i.e., $232.1 million FCF/$709.6 million in sales). And its TTM FCF margin was 32.2% (i.e., $904.6 million/$2.81 billion in sales). Most tech or software stocks with this level of FCF margin have a 3% or lower FCF yield.

Moreover, going forward, analysts are projecting significantly higher revenue. That will serve to increase its FCF levels on an absolute basis and probably its FCF margins as well.

For example, revenue forecasts for the year ending Jan. 2025 are $3.24 billion, up 15.7% from the $2.8 billion last fiscal year. Moreover, for the following year ending Jan. 2026, analysts predict $3.50 billion in sales. That means that its run rate next 12-month (NTM) revenue averages $3.37 billion.

Therefore, if we apply a 32.7% FCF margin to this NTM sales forecast, we get an FCF estimate of $1.1 billion (i.e., $3.37b x .0327). That means that FCF could be 21.6% higher than the $904.6 million in TTM FCF.

Moreover, this implies the valuation of DOCU stock could be significantly higher.

FCF Yield Price Target for DOCU Stock

Once the market realizes that the company is a FCF juggernaut it's likely to lower the 8.66% FCF yield valuation. For example, even at a 7.5% FCF yield (which is nowhere near the 3% typical FCF yield of stocks with this kind of FCF margin), the valuation would be much higher

Here's how that works. Take the $1.1 billion in the NTM FCF forecast and divide it by 0.75. That produces a market cap estimate of $14.667 billion. This is 40.5% over its present $10.44 billion market cap.

In other words, the stock is worth over 40% more, or $72.14 per share. Other analysts tend to agree with me.

For example, Barchart's survey of 18 analysts shows that their average price target is $62.40 per share. In addition, Yahoo! Finance, which uses Refinitiv survey data, reports that 17 analysts have an average $63.23 price target. AnaChart, a new sell-side analyst tracking service, shows that 17 analysts have an average $67.77 price target, or 31.9% higher.

Moreover, AnaChart shows that one analyst, Patrick Walravens, of JMP Securities, has an $84 price target for DOCU stock. He has hit his price targets over 54% of the time, according to AnaChart's analysis.

And don't forget one more significant catalyst for the stock. DocuSign recently increased its share repurchase program to over $1 billion. That represents a buyback yield of almost 10% on its $10.44 billion market valuation.

One easy way to play this, especially for existing investors, is to short out-of-the-money (OTM) put options in nearby expiry periods.

Shorting OTM Puts

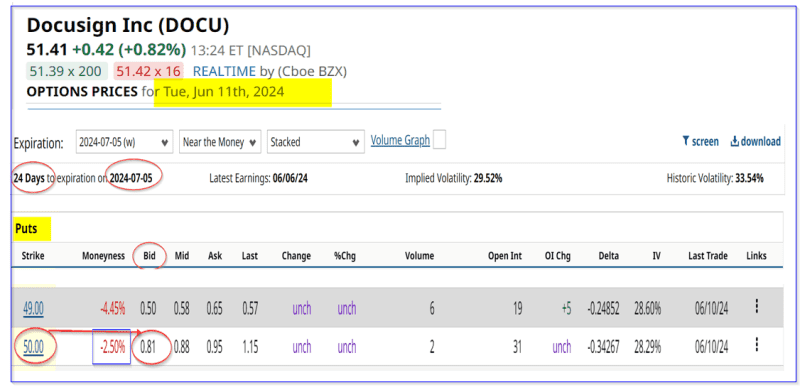

For example, look at the July 5, 2024, expiration period, which is slightly over 3 weeks from now. It shows that the $50 strike price put options trade for 88 cents per contract. That represents an immediate yield of 1.76% for the short seller of these puts.

This means that any investor who secures $5,000 in cash and/or margin with their brokerage firm can enter an order to “Sell to Open” one put option contract at this strike price and expiration date. The account will then immediately receive $88.00.

Note that this strike price is 2.5% below today's price, so there is room for the stock to fall before the investor is obligated to buy the shares at $50.00.

Moreover, for more conservative or risk-averse investors, securing $4,900 in cash and/or margin can make $50, and their out-of-the-money (OTM) risk is less since the stock is 4.45% over the strike price.

But, either way, this provides a good entry point for investors even if they have to use the secured cash to buy at these lower prices. Moreover, the expected return (ER) over the next quarter is high, if the investor can repeat these trades every 3 weeks. For example, the ER is $352 over the next 12 weeks, or 7.04% of the $5,000 invested four times.

This means that an existing investor in DOCU stock stands to make significant extra income, especially since DOCU still does not pay a dividend.

The bottom line is that DOCU stock looks cheap, given its high FCF margins, the excessively high FCF yield and its strong buyback program. One way to play this, especially for shareholders to make extra income, is to sell short out-of-the-money put options in nearby expiry periods.

More Stock Market News from Barchart

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.